Loop Capital analyst Dominick Gabriele initiated coverage of Mastercard (NYSE:MA | MA Price Prediction) with a Buy rating and a $631 price target, stepping into a stock that has pulled back sharply from its highs. With shares trading around $494 as of March 30, the initiation implies meaningful upside from current levels and arrives as the broader payments sector faces a reset in valuation.

| Ticker | Company | Firm | Rating | Price Target | Current Price |

|---|---|---|---|---|---|

| MA | Mastercard | Loop Capital | Buy (Initiation) | $631 | $494 |

The Analyst’s Case

Gabriele’s Buy initiation lands at a moment when Mastercard stock is down 13.34% year-to-date, well off its 52-week high of $600.08. The $631 target sits below the broader analyst consensus of $661.12, suggesting Loop Capital is taking a measured rather than aggressive stance. Still, the initiation adds to a coverage universe where 27 analysts carry Buy ratings and zero carry Sell ratings across 38 total analysts.

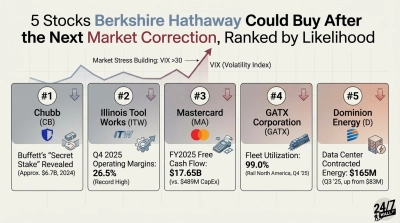

The fundamental case rests on Mastercard’s consistent ability to beat expectations and accelerate revenue beyond its core network. In Q4 2025, adjusted diluted EPS came in at $4.76 against a $4.24 consensus estimate, a beat of 12.26%. Full-year 2025 revenue reached $32.791 billion, up 16.42% year-over-year, with operating income expanding 21.27% to $18.897 billion.

Why the Move Matters Now

The growth story increasingly runs through value-added services, which expanded 26% in Q4 2025 and 23% for the full year. This segment, spanning digital authentication, security products, and consumer engagement, has accelerated every quarter in 2025, moving from 16% growth in Q1 to 26% in Q4. Cross-border volume, a high-margin revenue driver, grew 14% on a local currency basis in Q4, consistent with the 15% full-year pace.

At a forward P/E of 25x and a PEG ratio of 1.587, the valuation looks more reasonable today than it has in some time. The company’s operating margin of 57.7% and profit margin of 45.7% reflect the structural advantages of a two-sided network with limited marginal cost. CEO Michael Miebach captured the setup plainly: “Focused, agile, and diversified, we’re well positioned for the opportunities ahead in 2026.”

What to Watch Next

Mastercard’s $16.7 billion remaining buyback authorization and $17.648 billion in full-year operating cash flow provide a durable capital return floor. Regulatory risk on interchange rates and the Pillar 2 global minimum tax remain real headwinds, and the stock has pulled back sharply year-to-date. Loop Capital’s initiation at current levels reflects a well-regarded firm’s view that the risk/reward has shifted favorably following the pullback. Long-term investors focused on secular digital payment adoption should watch whether the value-added services growth trajectory holds into the first half of 2026.