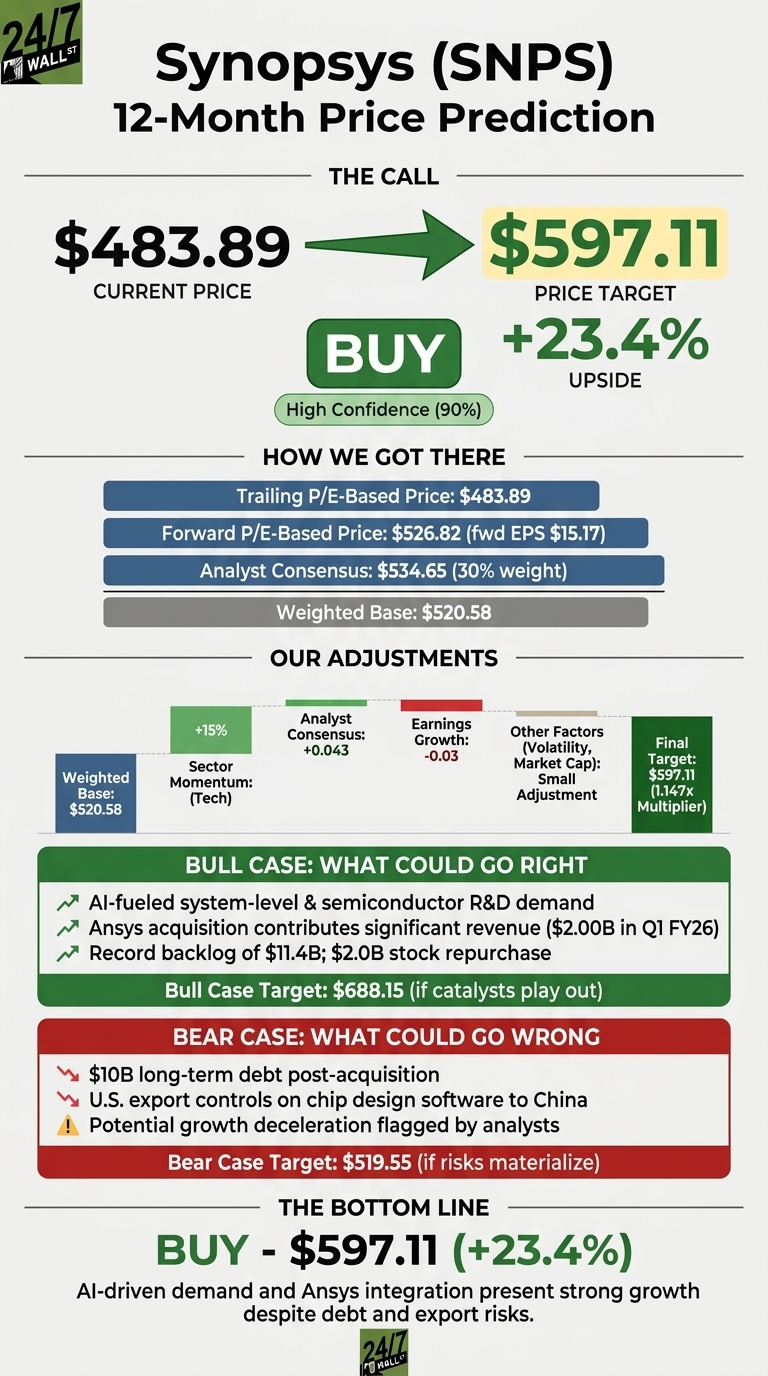

I’m leading with the headline because the math here is too important to bury. Synopsys (NASDAQ:SNPS | SNPS Price Prediction) trades at $483.89, and our 24/7 Wall St. price target points to $597.11 over the next 12 months. That implies 23.4% upside, and the model carries 90% confidence. The setup looks constructive from here.

| Metric | Value |

|---|---|

| Current Price | $483.89 |

| 24/7 Wall St. Price Target | $597.11 |

| Upside | 23.4% |

| Setup | Constructive |

| Confidence Level | 90% |

A Volatile Year Sets Up the Setup

SNPS has been one of the more volatile large-cap software names in recent memory. The stock is up 27.18% over the past month and 3.49% over the past week, yet it sits 18% below its 52-week high of $651.73. The October 2025 selloff, when SNPS dropped 35.84% in a single session on a 9.48% EPS miss, still anchors the chart.

Q1 FY2026, reported February 25, 2026, was the rebuttal. Revenue hit $2.41 billion, rising 65.4% YoY on the Ansys integration, and non-GAAP EPS of $3.77 beat consensus by 5.98%. Operating cash flow swung to $856.83 million, and Synopsys retired roughly $3.45 billion of long-term debt during the quarter.

The Case for $688 and Beyond

Bulls have a clean story. CEO Sassine Ghazi told investors “AI continues to fuel robust system-level and semiconductor R&D, and the increasing AI capabilities throughout our portfolio strengthen our strategic advantage and accelerate our customers’ innovation.”

Backlog ended FY2025 at $11.4 billion, FY2026 revenue guidance sits at $9.56 billion to $9.66 billion, and the board replenished a $2 billion buyback.

Analyst consensus target of $534.65 includes 17 Buy and 2 Strong Buy ratings. Our bull-case scenario lands at $688.15, a 42.21% total return, if Ansys synergies pull through and silicon-to-systems TAM expansion accelerates.

What Could Go Wrong

The bear case is real. SNPS carries $10 billion in long-term debt, GAAP net income fell 78.03% YoY in Q1 (depressed by $404 million in acquired intangible amortization), and management has flagged restructuring charges for FY26.

Morgan Stanley (NYSE:MS) downgraded the stock on growth deceleration concerns, and U.S. export controls on chip design software continue to threaten China revenue.

Bulls would counter that the GAAP weakness is a non-cash artifact of Ansys purchase accounting, with operating cash flow of $856.83 million telling the truer story. Our bear-case scenario settles at $519.55, still a 7.37% return.

The Setup From Here

The 24/7 Wall St. price target of $597.11 reflects a stock with credible 20%+ upside, 90% model confidence, and a recovering momentum profile (MACD turned bullish on April 20-21). The tipping factor for me is the AI-driven backlog.

The thesis holds if Ansys synergies continue tracking and Q2 prints near the $2.22 billion to $2.27 billion guide. The thesis breaks down if export controls escalate or if FY26 EPS guidance gets cut below $14.38.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $597 |

| 2030 | $905 |

These projections assume Synopsys executes on Ansys integration and AI chip design demand persists. Significant upside or downside could result from export-control changes or accelerated silicon-to-systems platform adoption.