I’m coming out of Microsoft’s (NASDAQ:MSFT | MSFT Price Prediction) Q3 FY2026 earnings report with a clear stance: the setup looks compelling at current levels.

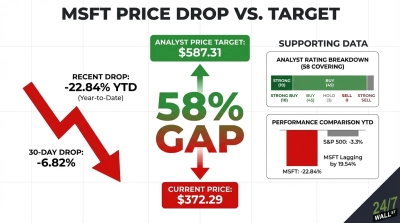

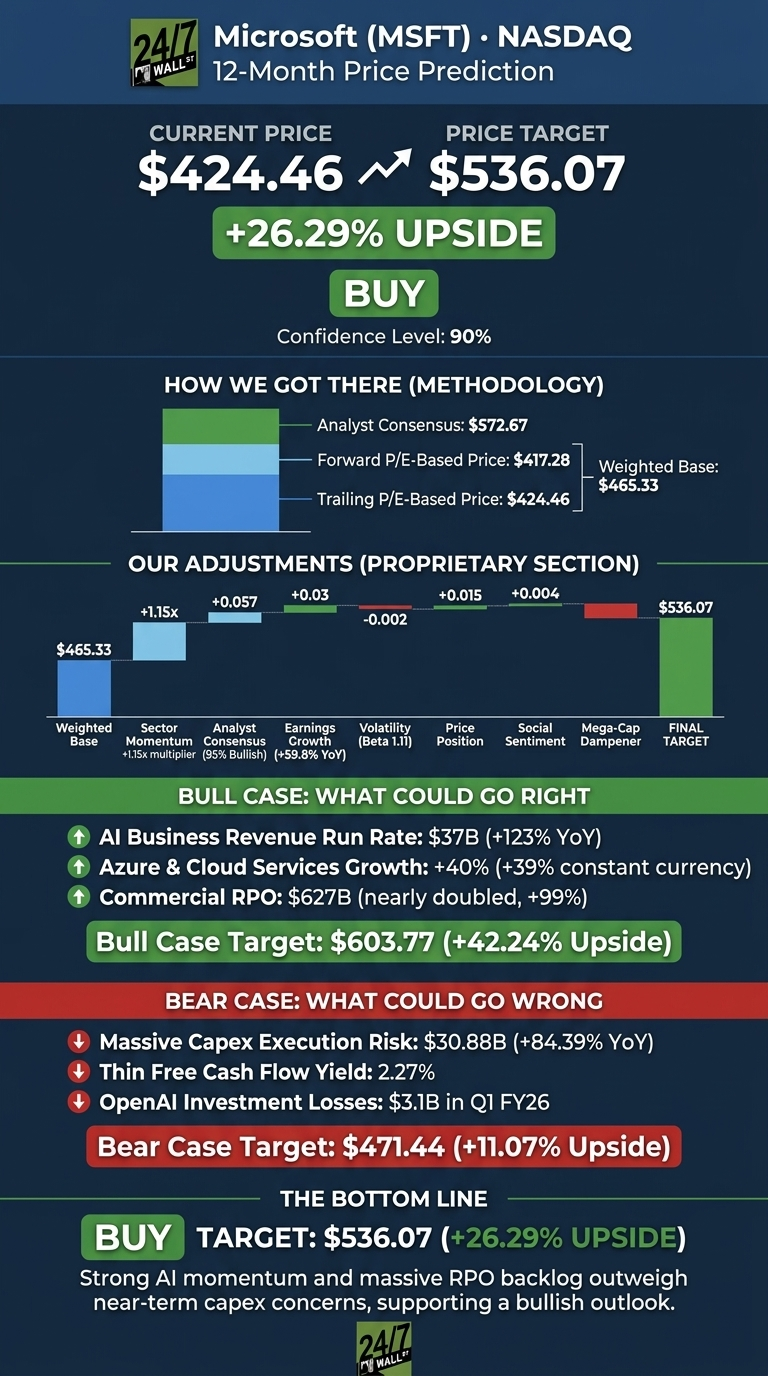

Microsoft just posted $82.88 billion in revenue, beat EPS at $4.27 versus $4.07 expected, and revealed an AI run rate that doubled. Yet the stock trades at $424.46, well below its 52-week high. Our 24/7 Wall St. price target for Microsoft is $536.07 over the next 12 months, with high conviction.

24/7 Wall St. Price Target Summary

| Metric | Value |

|---|---|

| Current Price | $424.46 |

| 24/7 Wall St. Price Target | $536.07 |

| Upside | 26.29% |

| Recommendation | BUY |

| Confidence Level | 90% |

A Choppy Stock Hiding a Strong Quarter

Microsoft is down 12.03% year to date and slipped 1.95% over the past week, even after rallying 18.25% off the March low of $358.96. Shares sit roughly 4% below the 52-week high of $552.24.

The Q3 FY2026 release on April 29, 2026 was the fourth straight EPS beat. Intelligent Cloud grew 30% to $34.681 billion, Azure climbed 40%, and commercial RPO ballooned to $627 billion, up 99%.

CEO Satya Nadella highlighted that “Our AI business surpassed an annual revenue run rate of $37 billion, up 123% year-over-year.” The market shrugged, with shares closing flat on the day.

The Case for $600+

The bull setup is straightforward. Of 58 covering analysts, 55 carry Buy or Strong Buy ratings with zero sells, and the consensus target of $572.67 sits well above our model.

Azure at 40% growth is reaccelerating, the $627 billion RPO backlog de-risks the next several quarters, and the AI segment’s $37 billion run rate (+123%) validates the capex spend. Operating margins held at 45.62% with ROE at 33.28%.

Our bull case projects $603.77 within 12 months, a 42.24% total return.

The Risks Worth Watching

Capex jumped 84.39% year over year to $30.876 billion in a single quarter, and free cash flow yield is a thin 2.27%. OpenAI investment losses hit $3.1 billion in Q1 FY26.

The Q2 FY2026 reaction was telling: a 7.57% beat met a 9.99% same-day decline, suggesting the market is wary of digestion risk on AI spend. Bulls would counter that this capex underwrites the $627 billion RPO and is already converting to revenue. Our bear case lands at $471.44, still positive at 11.07%.

The Bottom Line

The 24/7 Wall St. price target of $536.07 with a buy rating reflects 90% confidence. The factor that tips the scale is the RPO backlog: $627 billion in contracted future revenue removes most of the AI demand uncertainty.

The bullish thesis holds if Azure growth stays above 35% next quarter. The thesis weakens if capex outpaces operating cash flow growth by another quarter, since that signals returns are slipping.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $536.07 |

| 2027 | $622.49 |

| 2028 | $714.24 |

| 2029 | $783.83 |

| 2030 | $840.12 |

These projections assume Azure compounds at a mid-20s rate and AI infrastructure investments earn their cost of capital. Significant upside or downside could result from accelerated agentic AI adoption or a sharp drop in enterprise IT budgets.