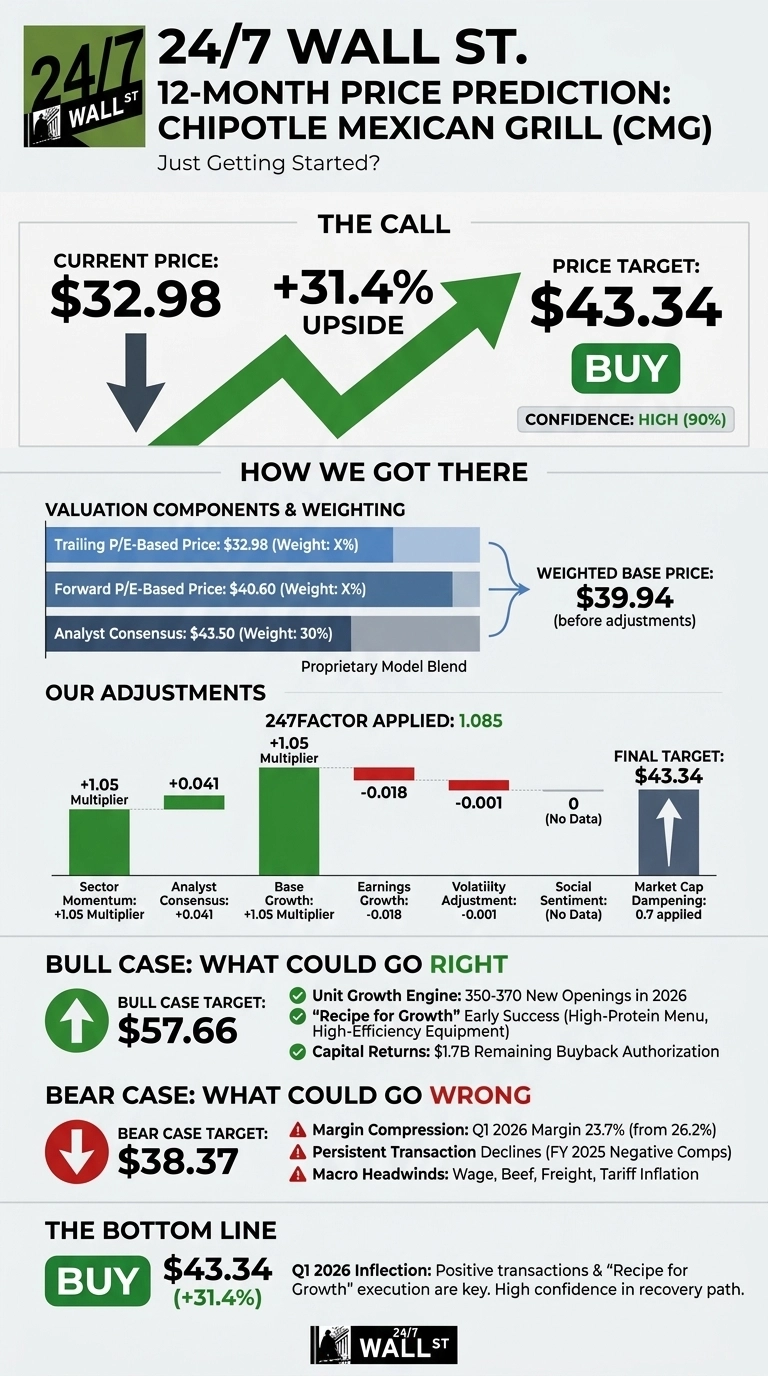

After a brutal year for shareholders, Chipotle Mexican Grill (NYSE:CMG | CMG Price Prediction) just delivered its first quarter of positive transaction growth in over a year. With the stock down 34.46% over the past 12 months and trading near multi-year lows, I think the setup looks compelling.

Our 24/7 Wall St. price target for Chipotle is $43.34, implying roughly 31.41% upside from the current $32.98 price. The recommendation is buy, and our model carries high confidence at 90%.

| Metric | Value |

|---|---|

| Current Price | $32.98 |

| 24/7 Wall St. Price Target | $43.34 |

| Upside | 31.41% |

| Recommendation | BUY |

| Confidence Level | 90% |

The Q1 2026 Inflection Has Arrived

Chipotle reported Q1 2026 results on April 29, 2026, and the earnings report marked the inflection bulls have been waiting for. Revenue rose 7.4% to $3.1 billion, comparable restaurant sales returned to positive territory at +0.5%, and transactions grew 0.6%. That snaps a streak that produced the chain’s first full year of negative comps in 2025.

Diluted EPS came in at $0.23, with restaurant-level operating margin compressing to 23.7% from 26.2% on beef and freight inflation plus higher labor costs. Digital sales reached 38.6% of food and beverage revenue, extending the steady climb from 35.4% in Q1 2025. Chipotle opened 49 new company-owned restaurants, with 42 including a Chipotlane.

Why Bulls See a Breakout Ahead

The bull case rests on three engines. First, unit growth: management guided to 350 to 370 new openings in 2026, with a long-term goal of 7,000 restaurants in U.S. and Canada.

Second, the “Recipe for Growth” strategy is starting to work, with CEO Scott Boatwright noting “early success of our high-protein menu and benefits from our high-efficiency equipment package.”

Third, capital returns: Chipotle repurchased $2.43 billion of stock in 2025 with $1.7 billion remaining authorized.

Wall Street agrees. The consensus target sits at $43.50, supported by 4 strong buy and 22 buy ratings against 12 holds. Our bull case scenario takes CMG to $57.66 over 12 months if comps accelerate above the flat 2026 guide.

The Risks Worth Watching

Margin compression is the main bear concern. Restaurant-level margins have now declined for five consecutive quarters, hit by wage inflation, beef and freight costs, and tariff-driven supply pressure.

The P/E of 30 still prices in growth that 2025 results did not deliver. Bears would argue persistent traffic softness amid food services spending of $1,526.4 billion in March 2026 reflects a saturated brand, not a temporary slump. Our bear case lands at $38.37.

It should be noted that bulls would counter that 2025’s margin pressure reflects investment in the high-efficiency equipment rollout, manager training, and 334 new units, costs that should normalize as new restaurants mature.

The Bottom Line

The 24/7 Wall St. price target is $43.34 with a buy rating and 90% confidence. Q1’s return to positive transactions is the catalyst that tips the scale. The bullish thesis hinges on the Recipe for Growth playbook continuing to translate into transaction gains through 2026. The thesis weakens if Q2 transactions reverse back into negative territory.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $43.34 |

| 2027 | $51.41 |

| 2028 | $60.05 |

| 2029 | $65.71 |

| 2030 | $71.99 |

These projections assume Chipotle hits its 7,000-restaurant domestic target while expanding internationally. Significant upside or downside could result from execution on the high-protein menu rollout and the international JV pipeline in the Middle East and Asia.