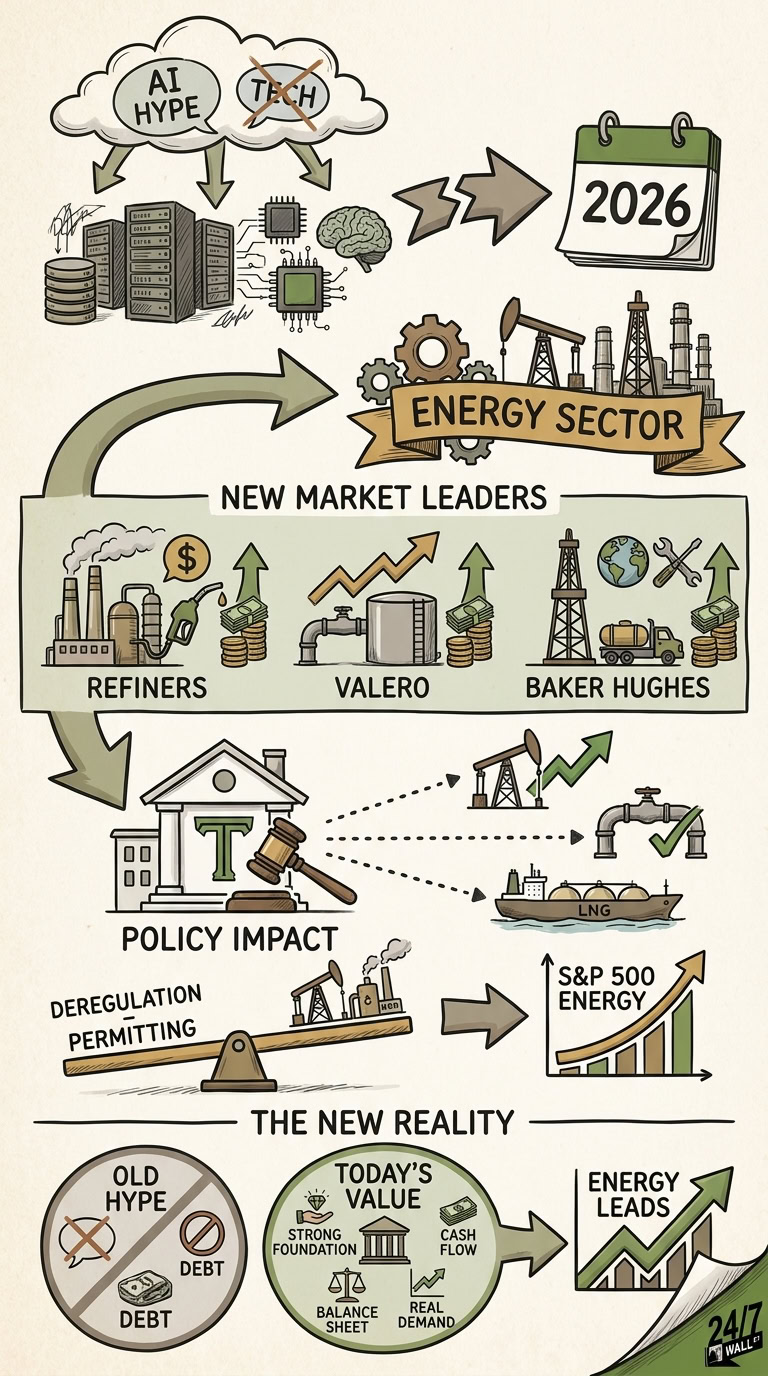

For the last two years, investors were trained to chase anything tied to artificial intelligence. Semiconductor stocks. Cloud stocks. Power-grid plays. If it touched a data center, Wall Street wanted in.

Then 2026 happened.

Suddenly, the market’s leadership changed. The flashy growth names cooled off while one of the market’s oldest industries started printing gains again: energy.

The surprise isn’t just that energy stocks are outperforming. It’s how decisively they’re doing it. The S&P 500 Energy sector has become one of the market’s best-performing groups this year as oil prices climbed, geopolitical tensions tightened supply expectations, and investors rotated toward companies generating real cash flow today — not promises five years from now.

And now investors are asking the obvious question: Could President Donald Trump’s policy agenda push the rally even further?

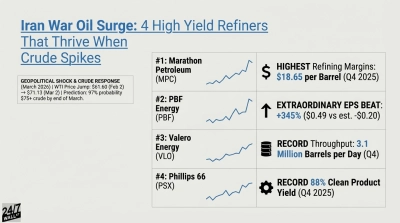

Refiners Are Leading the Charge

The biggest winners inside the energy trade have not been the oil majors. Surprisingly, refiners and energy service companies have stolen the spotlight.

Here’s how three of the sector’s top performers stack up so far in 2026:

| Company | YTD Return | Dividend Yield | Forward P/E |

| Marathon Petroleum (NYSE:MPC | MPC Price Prediction) | 52.3% | 1.6% | ~13 |

| Valero Energy (NYSE:VLO) | 51.5% | 1.9% | ~13 |

| Baker Hughes (NYSE:BKR) | 51.4% | 1.3% | ~24 |

That says investors are suddenly willing to pay more for businesses tied to energy production, fuel demand, and drilling infrastructure.

Let’s start with Marathon Petroleum. The refiner is benefiting from stronger refining margins as gasoline and diesel spreads widened during the first quarter. Marathon also continued aggressively returning capital to shareholders. It repurchased billions in stock over the past year while maintaining one of the strongest balance sheets in the refining industry.

Valero followed a similar path. Refiners tend to thrive when crude supply disruptions create volatility because fuel prices often rise faster than input costs. In short, chaos can actually help margins — at least temporarily.

Then there’s Baker Hughes, which gives investors a different angle on the trade. Instead of refining fuel, Baker Hughes sells the equipment, services, and technology energy producers need to drill, transport, and process oil and natural gas. As exploration budgets expanded globally, Baker Hughes captured higher orders across its LNG and oilfield services segments.

Why Trump Could Add More Fuel to the Rally

Markets do not move on politics alone. Earnings still matter. Cash flow still matters. But policy absolutely shapes industries — and energy investors know it.

Trump has consistently pushed for expanded domestic energy production, faster permitting approvals, reduced environmental restrictions, and increased LNG exports. Whether investors agree politically is almost beside the point. Markets care about what policies could mean for profits.

More drilling activity generally benefits companies like Baker Hughes. More pipeline approvals can improve transport economics. Expanded refining demand can support companies like Marathon and Valero.

According to the U.S. Energy Information Administration, U.S. crude production already reached record levels above 13 million barrels per day entering 2026. Additional deregulation could keep that trend moving higher.

Granted, there are risks. Oil remains cyclical. A recession could reduce fuel demand quickly. OPEC production changes could pressure prices — the UAE just quit OPEC+, which could introduce significant price volatility. And if inflation stays sticky, the Federal Reserve may keep interest rates elevated longer than investors expect.

That said, energy stocks look far different than they did during previous commodity booms.

Many companies spent the last several years reducing debt, cutting unnecessary expansion spending, and focusing on shareholder returns instead of reckless production growth. That discipline matters.

This Rally Looks Different From Past Energy Booms

Back in the shale boom years, many energy companies chased production growth at any cost. Investors got rising oil output but weak returns.

Today’s market looks more restrained.

For example:

- Marathon Petroleum generated $8.3 billion in free cash flow in 2025 while reducing share count.

- Valero had refining utilization rates between 97% and 98% of capacity last year..

- Baker Hughes’ Industrial & Energy Technology expanded margins to its 20% target while growing internationally in LNG infrastructure.

Regardless, this is not simply a speculative oil spike trade anymore. Investors are rewarding profitability, balance-sheet strength, and capital returns.

And compared to many technology stocks still trading above 25 or 30 times forward earnings, several energy leaders remain valued near 11 to 17 times earnings. That valuation gap matters.

Key Takeaway

In any case, 2026 has reminded investors that market leadership changes faster than most people expect. Energy stocks entered the year rising a moderate 7.9%. Now they’re leading the S&P 500.

Could the rally continue? Yes — especially if Trump’s energy policies accelerate domestic production and infrastructure investment. But smart investors should also recognize this remains a cyclical industry tied closely to oil prices and global demand.

Still, companies like Marathon Petroleum, Valero, and Baker Hughes are giving investors something Wall Street increasingly values in this market: strong cash flow, shareholder returns, and businesses built around real-world demand instead of hype alone.