Institutional money is moving into U.S. refiners with conviction, and the earnings data backs it up. Marathon Petroleum (NYSE: MPC | MPC Price Prediction), Phillips 66 (NYSE: PSX), and Valero Energy (NYSE: VLO), have all surged roughly 31% to 40% year-to-date as of March 11, 2026, yet analyst consensus ratings have not kept pace with where institutions are positioning.

The Earnings Signal Is Unmistakable

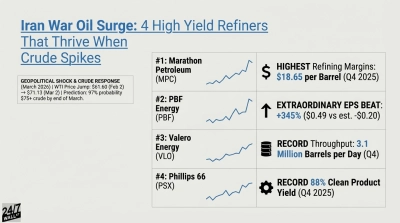

All three refiners delivered substantial Q4 2025 earnings beats. Marathon Petroleum reported adjusted EPS of $4.07 against a $2.71 consensus estimate, a 50.18% beat. Phillips 66 beat by 50.10%, posting $2.47 versus a $1.65 estimate. Valero Energy came in at $3.82 adjusted EPS versus the $3.27 consensus, a 16.82% beat. These aren’t one-quarter flukes; all three also beat in Q3 2025.

The driver is refining margins. Marathon Petroleum’s Refining & Marketing adjusted EBITDA hit $2.00 billion in Q4 2025, up from $559 million in Q4 2024, with margin per barrel at $18.65 and crude utilization at 95%. Phillips 66 achieved record 88% clean product yield with 99% crude utilization, while Valero Energy set a record throughput of 3.1 million barrels per day in Q4. A key margin catalyst across all three: access to discounted Venezuelan heavy crude, which widens the spread between feedstock cost and refined product prices.

Where Analyst Ratings Diverge From Institutional Action

This is where the gap becomes investable intelligence. For Marathon Petroleum, the analyst consensus sits at eight Hold ratings, six Buys, and four Strong Buys, with an average price target of $202.50—a level the stock has already blown past. Marathon Petroleum trades near $225 today, roughly 10% above that consensus target. Yet Vanguard, Quantbot, and GF Fund Management have all been increasing their Marathon Petroleum stakes, and institutional ownership is at 77.1%.

Phillips 66 presents the sharpest divergence. Analysts carry a consensus target of $160.15, with 10 Hold ratings, seven Buys, one Sell, and one Strong Sell. The stock is trading near $168 today, above that target. Phillips 66 has raised its quarterly dividend for 14 consecutive years, and institutional ownership stands at 78.5%. For Valero Energy, the average analyst target is $202.72 with seven Buys, seven Holds, and one Strong Sell, while the stock has run 84.89% over the past year and institutional ownership is at 87.8%, the highest of the three.

The Gap and What It Means for Retail Investors

When institutional ownership is this high and stocks are trading above analyst price targets, the traditional buy/hold/sell framework loses its edge. Institutions aren’t waiting for analyst upgrades. They are responding to operating leverage in a favorable crack spread environment, disciplined capital return programs, and low crude feedstock costs. Benchmark West Texas Intermediate (WTI) crude settled at $64.51 in February 2026, down sharply from $75.74 in January 2025—lower input costs that directly support refiner margins when product prices hold.

The risks are real and shouldn’t be dismissed. All three companies have warned Governor Newsom about potential California refinery shutdowns tied to CARB regulatory pressure. Valero is already ceasing operations at its Benicia refinery by the end of April 2026. Phillips 66’s CFO sold 21,800 shares at approximately $165 to $168 in early March 2026, though this followed a coordinated executive buying event in February. Tariff exposure on crude imports and crack spread volatility remain the sector’s structural wildcards.

The Takeaway

The smart money is right that refiner fundamentals are strong. Four consecutive quarters of earnings beats, expanding margins, record throughput, and aggressive shareholder returns confirm it. For retirement-focused investors, the question isn’t whether the thesis is valid—it is. The question is entry points. With all three stocks trading at or above consensus analyst targets, the easy money has been made. Investors adding here are buying operational excellence at a premium, betting that institutions know something the ratings haven’t caught up to yet. Given the institutional conviction on display, that bet has a credible foundation, but position sizing matters when the gap between price and target is already this wide.