The market has spent the past several years reminding investors of one timeless truth: time matters more than timing. A few extra years of compounding can turn modest savings into life-changing wealth. That’s why the federal government’s new “Trump Accounts” program has drawn so much attention.

Beginning July 4, families can officially start contributing to the accounts — and surprisingly, even doing the bare minimum could produce a meaningful nest egg by adulthood.

The bigger story isn’t politics. It’s compounding. And when all is said and done, that’s what smart investors should focus on.

What Trump Accounts Are — and Why They Were Created

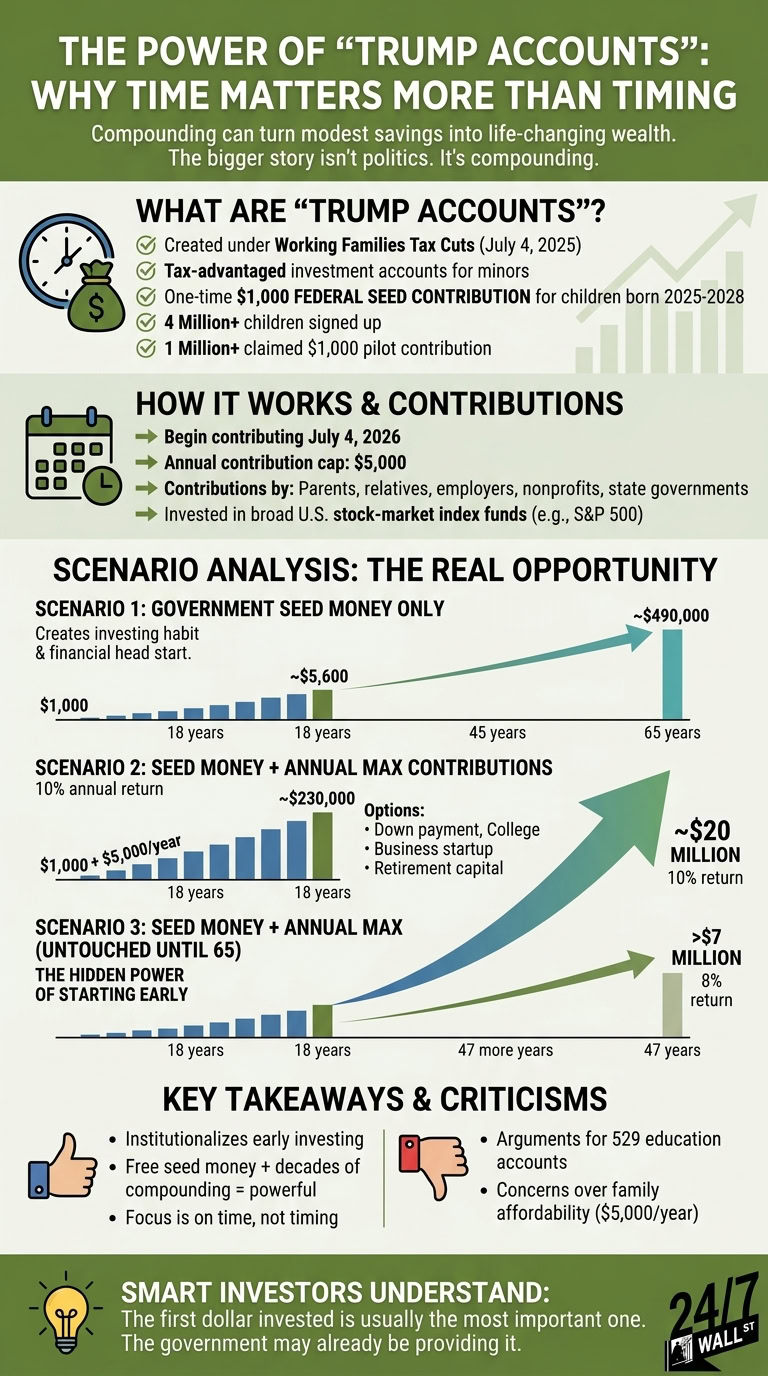

Trump Accounts were created under the Working Families Tax Cuts legislation signed into law on July 4, 2025. According to the IRS, the accounts function as tax-advantaged investment accounts for minors under age 18. Eligible children born between Jan. 1, 2025 and Dec. 31, 2028 can also receive a one-time $1,000 federal seed contribution.

The IRS reported in March that more than 4 million children have already been signed up for Trump Accounts, while roughly 1 million children have already claimed the $1,000 pilot-program contribution.

Beginning July 4, 2026, parents, relatives, employers, nonprofits, and even state governments can begin contributing money to the accounts. The annual contribution cap is $5,000. Funds must generally be invested in broad U.S. stock-market index funds, such as those tracking the S&P 500.

That last part matters. It means the money is designed to grow alongside Corporate America for decades.

A $1,000 federal boost today could grow into a $20 million legacy tomorrow. This is the math of compounding that the government is betting on for the next generation.

A $1,000 federal boost today could grow into a $20 million legacy tomorrow. This is the math of compounding that the government is betting on for the next generation.

Here’s What the Numbers Tell Us

Let’s start with the simplest scenario possible.

Suppose parents do absolutely nothing beyond claiming the government’s free $1,000 contribution. If that money compounds at the S&P 500’s long-term historical average annual return of roughly 10%, the account could grow to about $5,600 by age 18.

Not bad for doing almost nothing.

Granted, inflation will reduce some purchasing power over that period. But investors should remember the point here isn’t instant wealth. It’s creating an investing habit and giving children a financial head start many Americans never had.

Now let’s look at what happens when families consistently contribute.

If parents invested the maximum $5,000 annually starting at birth and earned an average 10% annual return, the account could grow to roughly $230,000 by the child’s 18th birthday.

That changes the equation entirely. A young adult with $230,000 already invested has options most people spend decades trying to create:

- A down payment on a home

- College funding flexibility

- A business startup cushion

- Long-term retirement capital

Regardless of how you look at it, the math gets powerful quickly.

The Real Opportunity Isn’t Age 18 — It’s Age 65

Here’s where things become genuinely eye-opening.

Suppose contributions stop at age 18 and the $230,000 simply remains invested until retirement at age 65, earning that same 10% annual return. The result? Roughly $20 million. Even using a more conservative 8% annual return assumption, the account could still grow to more than $7 million over that time period.

That’s the hidden power of starting early.

| Scenario | Contributions Made | Time Horizon | Assumed Annual Return | Estimated Ending Value |

| Government seed money only | One-time $1,000 deposit | 18 years | 10% | ~$5,600 |

| Government seed money only | One-time $1,000 deposit | 65 years | 10% | ~$490,000 |

| Seed money + annual max contributions | $1,000 initial deposit + $5,000 annually for 18 years | 18 years | 10% | ~$230,000 |

| Seed money + annual max contributions, then untouched | $1,000 initial deposit + $5,000 annually for 18 years, then no further contributions | 65 years | 10% | ~$20 million |

Surprisingly, most investors don’t fail because they pick bad stocks. They fail because they start too late. A 40-year-old investor can save aggressively and still struggle to catch someone who began compounding at birth.

That’s what makes Trump Accounts interesting from an investing perspective. They institutionalize early investing.

That said, there are reasonable criticisms. Some financial planners argue 529 education accounts offer better tax advantages for college savings. Others question whether families already struggling financially can realistically contribute $5,000 annually.

Those concerns are valid. But even critics generally acknowledge one thing: free seed money combined with decades of compounding is difficult to ignore.

Key Takeaway

In short, Trump Accounts are less about politics than they are about time.

A single $1,000 government contribution probably won’t transform a child into a millionaire overnight. But paired with regular investing and decades of compounding, it absolutely can become the foundation of serious long-term wealth.

Smart investors understand that the first dollar invested is usually the most important one. And in this case, the government may already be providing it.