Snowflake (NYSE:SNOW | SNOW Price Prediction) currently trades around $140 versus a Wall Street consensus price target of $232.74, implying that analysts see roughly 66% upside for the stock today. Snowflake operates a cloud data platform that is now positioned as an AI data cloud under CEO Sridhar Ramaswamy. Enterprises use it to query, share, and build applications on structured and unstructured data, with new AI features layered on top through partnerships with OpenAI, Anthropic, and Google Cloud. That 66% upside gap is particularly high even amongst large-cap software companies, which have sold off on SaaSpocalypse fears. To add to that, many analysts regard Snowflake as a company with a fairly wide moat that can benefit from AI.

A 36% Year-to-Date Wipeout Has Left SNOW Trading Near Its 52-Week Low

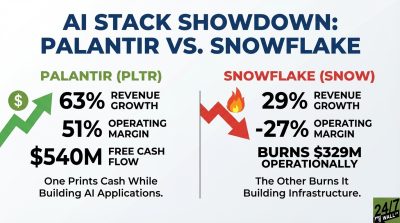

Snowflake is down 36.03% year to date and sits well below its 52-week high of $280.67, hovering just above the 52-week low of $118.30. The Q4 FY2026 report was solid on the surface. EPS came in at $0.32 versus $0.27 expected, and revenue grew 30% to $1.28 billion. Remaining performance obligations rose an impressive 42% to $9.77 billion, pointing to continued demand. However, the key issue is profitability and sentiment. Snowflake posted a GAAP operating loss of $318 million, alongside $423 million in stock-based compensation. Shares then fell roughly 17% following the report and continued lower, with ongoing pressure from litigation tied to the 2024 disclosure controversy.

The S&P 500 is up 4.7% year to date, so SNOW is underperforming the index by roughly 40 percentage points. That could point to the business being meaningfully undervalued today.

Why Analysts Are Doubling Down on the AI Data Cloud Thesis

Analysts remain firmly bullish. The bull case rests on Snowflake compounding consumption-led growth while AI workloads layer on top of an already-sticky data platform. Guidance supports that thesis. FY2027 product revenue is expected to reach $5.66 billion, up 27%, with improving margins as the business scales.

AI adoption is also ramping quickly. Snowflake Intelligence reached about 2,500 accounts within three months, while more than 9,000 customers are already using AI features. The company also continues to expand its footprint, serving 790 companies in the Forbes Global 2000, with over 700 customers generating more than $1 million in annual product revenue.

Of the analysts covering Snowflake, 10 rate the stock a Strong Buy, 35 a Buy, 7 a Hold, and 0 a Sell or Strong Sell. Net revenue retention of 125% and a record 740 net new customers in Q4 give the bulls a usage trajectory to point to. The CFO has framed FY2027 as the year operating leverage shows up, which is the catalyst window most price targets are anchored to.

What I See with Snowflake at $140

The bull case for Snowflake rests on the company’s success in turning AI into incremental consumption on top of its existing platform. If product revenue scales toward $5.66 billion, net revenue retention stays elevated, and margins expand as guided, the current multiple can hold, and the stock has a real path toward the $230+ target range. The bear case rests on the model breaking under pressure. If consumption slows, stock-based compensation continues to weigh on profitability, or litigation creates another sentiment reset, the stock can stay stuck or move lower despite solid top-line growth.

My view is that Snowflake is a stock with a high potential upside but it’s ultimately dependent on execution. At ~$140, the market is already discounting a lot of risk, which is why you’re seeing a ~66% gap to targets. But that upside only materializes if Snowflake proves it can convert AI enthusiasm into durable revenue and margin expansion.