Bernstein analyst Peter Weed raised his price target on ServiceNow (NYSE:NOW | NOW Price Prediction) to $236 from $226 while maintaining an Outperform rating, framing the company’s Analyst Day as a long-term margin and free cash flow win. The catch: the same event armed the bears with a 2030 subscription revenue target of $30 billion that implies growth decelerating toward the mid-teens.

That’s the rare analyst note that lays out exactly why ServiceNow stock could move in either direction off the same set of facts. The price target raised by Bernstein sits well above the consensus, but the bullish thesis hinges on margins, not growth.

| Ticker | Company | Firm | Action | Old Rating | New Rating | Old Target | New Target |

|---|---|---|---|---|---|---|---|

| NOW | ServiceNow | Bernstein | Price target raised | Outperform | Outperform | $226 | $236 |

The Analyst’s Case

Bernstein highlighted ServiceNow’s revised long-term framework, which lifts the Rule of 40 target toward Rule of 60-plus by 2030. Free cash flow margins are implicitly rising 900 basis points versus 2025, and stock-based compensation is set to fall to less than 10% of revenue by 2029.

Yet, the firm conceded ServiceNow “also fed the bears.” The $30 billion 2030 subscription target points to mid-teens growth, which bears read as confirmation that the days of 20%-plus growth are ending. For broader context on enterprise AI software valuations, see our recent analysis of enterprise AI software stocks.

Company Snapshot

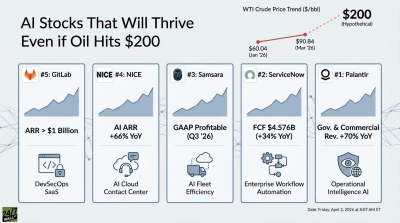

ServiceNow, led by CEO Bill McDermott, runs an AI-driven workflow platform now positioned as an “AI control tower for business reinvention.” Q1 2026 subscription revenue reached $3.671 billion, growing 19% year-over-year (YoY) in constant currency, with operating margin at 32% and free cash flow margin at 44%.

The Now Assist AI revenue target was raised from $1 billion to $1.5 billion for 2026, reflecting agentic AI traction. ServiceNow customers spending $1 million-plus grew over 130% YoY, and the company integrated Moveworks into Employee Works in under three weeks.

Why the Move Matters Now

NOW stock has been punished, down 41.5% year to date and 54% over the past year, as growth-deceleration fears collided with SaaS multiple compression. ServiceNow shares trade with a forward P/E ratio of 22x and a trailing P/E ratio of 55x, against a consensus analyst target of $144.88.

Bernstein’s $236 target sits materially above consensus, signaling conviction that margin expansion and AI monetization can re-rate ServiceNow stock even if top-line growth normalizes. The Analyst Day cracked open both the bull and bear thesis at once.

What It Means for Your Portfolio

For prudent investors, ServiceNow stock sits at the intersection of a credible Rule of 60-plus margin story and a real top-line deceleration debate. The bullish read leans on McDermott’s framing that “ServiceNow is the AI-defining enterprise software company in the 21st century” and tangible Now Assist traction.

The bearish read questions whether any SaaS name decelerating to mid-teens growth can sustain a premium multiple. Reddit’s most-engaged thread during Analyst Day week was titled “Service Now (NOW) : Screaming BUY or Rightly SOLD Off?”, capturing the divide perfectly.

Position sizing and patience matter. The long-term free cash flow story could reward ServiceNow shareholders, while volatility around quarterly growth prints may persist as the bull and bear camps trade punches.