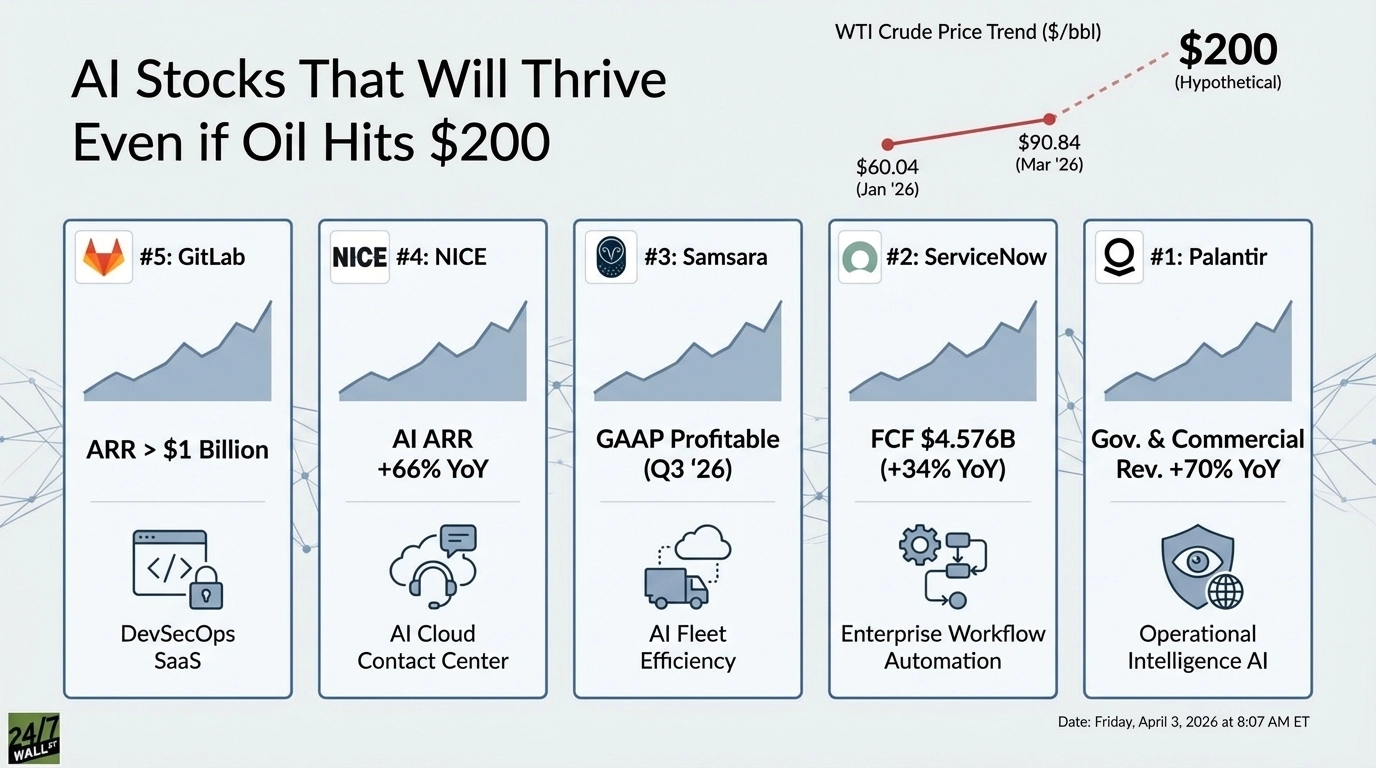

Practically all of my personal investing is centered around AI companies, or those who will benefit from it. But we can’t ignore macro events. What happens if things get ugly out there?

Not mild-recession ugly. Oil-at-$200 a barrel ugly.

That scenario carries only a 2.55% implied probability on Polymarket, but that’s not the point. The point is stress-testing. WTI crude has already moved from $60.04 in January 2026 to $110 in March 2026, a sharp move that reminds us how fast energy markets can reprice. The AI stocks that survive a genuine oil shock are asset-light, subscription-driven, and whose value proposition accelerates when operating costs surge everywhere else. Here are five that fit.

#5: GitLab

GitLab (NASDAQ:GTLB | GTLB Price Prediction) builds the platform enterprises use to write, secure, and ship software. No trucks, no factories, no fuel. Pure DevSecOps SaaS.

In Q4 FY2026, GitLab posted revenue of $260.40M, up 23.2% year over year, ahead of estimates, non-GAAP EPS came in at $0.30, ahead of the $0.23 estimate and exceeding expectations by a wide margin. Full-year free cash flow hit $219.55M, up 424% year over year. ARR crossed $1 billion, and non-GAAP operating margin expanded to 21% from 18%.

The AI product is the GitLab Duo Agent Platform, now generally available, bringing agentic AI across the full software lifecycle. CEO Bill Staples:

“As code volume explodes, security, compliance, and governance are no longer optional; they’re existential. GitLab was built for this environment.”

GitLab is down 39.86% year to date, which makes the setup more interesting today than six months ago. If you believe AI-native DevSecOps is a durable category, the valuation compression is worth understanding in that context.

#4: NICE

NICE (NASDAQ:NICE) runs the CXone platform, the AI-native cloud contact center solution used by large enterprises globally. No supply chain, no energy-intensive manufacturing.

In Q4 2025, NICE posted revenue of $786.50M, up 9% year over year, AI ARR reached $328M, up 66% year over year. AI was embedded in 100% of new seven-figure CXone deals for all of 2025. At a forward P/E of 10x and an analyst consensus target of $154.27 against a current price of $113.20, the valuation is cheap for the growth profile. NICE holds $417.4M in cash with zero debt. A $200 oil world doesn’t touch this business model.

#3: Samsara

Samsara (NYSE:IOT) is the most interesting oil-shock play on this list. Higher oil prices are a direct demand catalyst: Samsara sells AI-powered fleet management and physical operations software to trucking companies, logistics operators, and construction firms. When fuel costs spike, every fleet operator needs Samsara’s efficiency tools more urgently.

Q3 FY2026 revenue hit $415.98M, up 29.2% year over year, ahead of estimates. The company reached its first quarter of GAAP profitability with net income of $7.77M. Non-GAAP operating margin expanded 800 basis points year over year to 19%. ARR stands at $1.75B, up 29%. The analyst consensus target is $44.17 against a current price of $32.26. The efficiency narrative gets stronger as energy costs climb.

#2: ServiceNow

ServiceNow (NYSE:NOW) automates enterprise workflows at scale. In a $200 oil world, every CFO is cutting headcount and automating manual processes. ServiceNow is the platform they turn to.

Q4 FY2025 revenue came in at $3.568B, up 20.7% year over year. Full-year free cash flow reached $4.576B, up 34%. The Now Assist generative AI product saw net new ACV more than double year over year. CEO Bill McDermott:

“With our consistent Rule of 55+ profile, there is no AI company in the enterprise better positioned for sustainable profitable revenue growth than ServiceNow.”

ServiceNow is down 33.42% year to date, trading at $102 against an analyst consensus target of $186.14. If you believe enterprise automation spending is durable through a macro shock, the drawdown reframes the valuation conversation entirely.

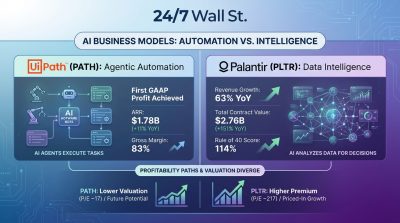

#1: Palantir

Palantir (NASDAQ:PLTR) is the clearest answer to the $200 oil question. Government contracts provide a recession-proof revenue floor. The AIP platform sells operational intelligence to enterprises that need efficiency most when costs are highest.

Q4 2025 revenue hit $1.407B, up 70% year over year, exceeding estimates. U.S. commercial revenue reached $507M, up 137% year over year. GAAP net income was $608.68M, up 670% year over year. The Rule of 40 score stands at 127%. Full-year free cash flow came in at $2.270B, up 99%. FY2026 guidance calls for revenue of $7.182B–$7.198B, implying 61% growth.

Alex Karp:

“Palantir is alone in choosing to exclusively focus on scaling the operational leverage made possible by the rapid advancements of AI models.”

Palantir is down 16.48% year to date despite being up 69.77% over the past year. Reddit sentiment has turned bearish, with the “Getting out of Palantir” post drawing 1,854 upvotes. I read that and see retail investors heading for the exits, not fundamental deterioration. The valuation is demanding at a trailing P/E of 239x, and that’s a real risk. But the growth profile, government contract base, and AI platform positioning make Palantir the most structurally insulated AI stock if energy costs go parabolic.

The $200 Oil Thesis, Delivered

We opened with a stress test: which AI stocks survive if oil doubles? The answer comes down to business model architecture. Every company on this list shares the same core traits: asset-light software models with no meaningful physical supply chain exposure, recurring subscription revenue not tied to consumer discretionary spending, and AI value propositions that accelerate when operating costs are high.

GitLab gets more valuable as code volume explodes. NICE gets more valuable as enterprises automate customer service. Samsara gets more valuable as fuel costs make fleet inefficiency unaffordable. ServiceNow gets more valuable as every CFO hunts for automation. Palantir gets more valuable as governments and enterprises need operational intelligence to navigate chaos.

If oil never hits $200, these businesses still compound. If it does, the demand case for each of them gets stronger by the day.