This article explores the growth experienced by Bloom Energy ($BE) and Caterpillar($CAT) over the past year. These companies could extend their bull run, due to their competitive advantages that sets them as critical players in the AI capex buildout.

Bloom Energy ($BE)

Context

Bloom Energy is a non-traditional tech company, it focuses on on-site electricity production. The company’s flagship product consists of Bloom Energy server. Unlike nuclear, renewables, or combustion-based power generation, Bloom’s servers rely on fuel cells. These convert natural gas, among other fuels, into electricity without combustion but through an electrochemical process.

Fuel Cells

While the technology might sound novel, it has been around since the 18th century. The first commercial use of fuel cells was during the Apollo program. NASA chose fuel cells to generate electricity inside the ship due to several advantages over other technologies. Fuel cells were safer than nuclear approaches, worked with the available materials in the rocket ( Hydrogen and Oxygen) and provided useful byproducts for the crew, including water. During the Apollo missions, the fuel cells started with limited electricity production, only a couple of kW. Nonetheless, the power output increased with the years as the technology matured. By the 2000’s, people widely knew the technology, but it still showed several shortcomings. These factors reduced its competitiveness compared to other on-site generation methods, due to higher cost per kW and shorter lifespan.

Bloom Energy started as an academic project for NASA’s Mars Missions program, but soon evolved as a fuel cell company. The company realized the technology’s limitations, and invested heavily to improve costs and lifespan. As a result, it achieved significant reductions in the cost per kW and longer systems lifespans.

By 2006 it deployed its first 5kW unit to the University of Tennessee, and by 2008 it launched its Energy Server. Its first big clients were Google, Walmart, Coca-Cola among others. The company continued to scale its operations, expanding its manufacturing capacity with a new plant in Delaware in 2012 and eventually going public by 2018. From there, the company has continued to expand. The company scaled to 1 GW by 2024 and secured its first Hyperscaler deal by 2025.

Today, Bloom Energy is becoming a critical player in the AI CAPEX and OPEX buildout. Its energy server presents an alternative for ever increasing power needs that the grid just can’t follow up.

Bloom Energy’s technology

Bloom Energy servers allow on-site electricity production, that means the electricity is offgrid. The main fuel used is natural gas but it can work with several others, such as hydrogen, biogas, or propane. The output is DC which means it can directly power the computing racks in data centers without AC to DC conversions and the energy loss implied. The company claims 99.999% uptime, being cleaner than combustion technologies and to be improving its technology cost at an average rate of 19% YoY.

For Hyperscalers, Bloom’s technology translates to reliable energy, constant power, predictable cost. Overall, data centers can meet modular electricity needs as they grow, without dealing with grid contract bureaucracy. Experts expect that by 2030, the data center energy demand will grow by around 100%, reaching 950 TWh. In moderate calculations that is around 120 GW of additional electricity capacity. Energy demand is expected to grow progressively. Only a handful of options can meet data center reliability and power constraints at this scale: nuclear, combustion-based systems, and fuel cells.. These methods share the capacity to handle the enormous power needs and similar reliabilities.

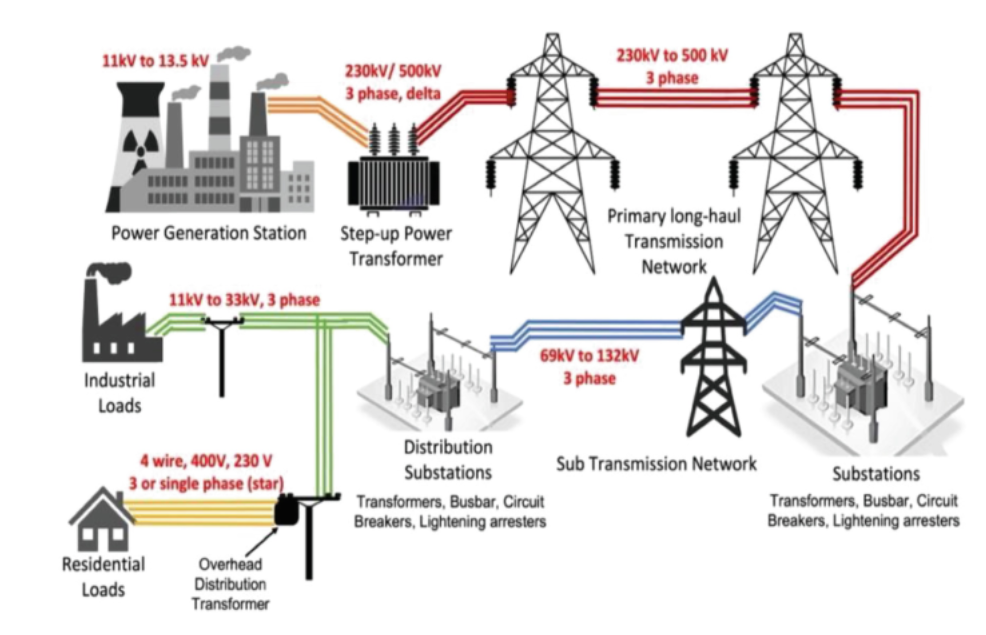

The Grid and the AI buildout

With electricity production, the endgame is in the distribution. With the incoming wave of electricity needs, the timeframes for many generation methods seem limited. New generation facilities require grid support for power distribution. Transmission lines carry electricity from high-voltage lines to then converted to medium-voltage lines. The system then delivers the power to data centers for consumption. Inside data centers, computing racks convert AC power into DC. All of these steps reduce the effective efficiency in the system, compared to a direct on-site DC energy production.

A general picture of the electric grid

Furthermore, these facilities could experience significant delays, not only for construction, but permissions and regulations that might change over time. To illustrate, a new nuclear plant can take between 5 and 20 years to be fully functional. Natural gas electric generation plants take on average 2 years for the physical construction, but securing permits, purchasing equipment and connecting to the grid can add up to 3 years. Bloom advertises its solution as taking 90 days to install and begin generating power at the selected facility.

Bloom’s approach

As mentioned by Bloom Energy’s CEO ‘AI can’t rely on the Power Grid Anymore’ a single 1 GW data center consumes the same electricity as the city of San Francisco. The grid cannot handle this level of demand, and reconfiguring it takes years, while the AI buildout cannot wait that long.

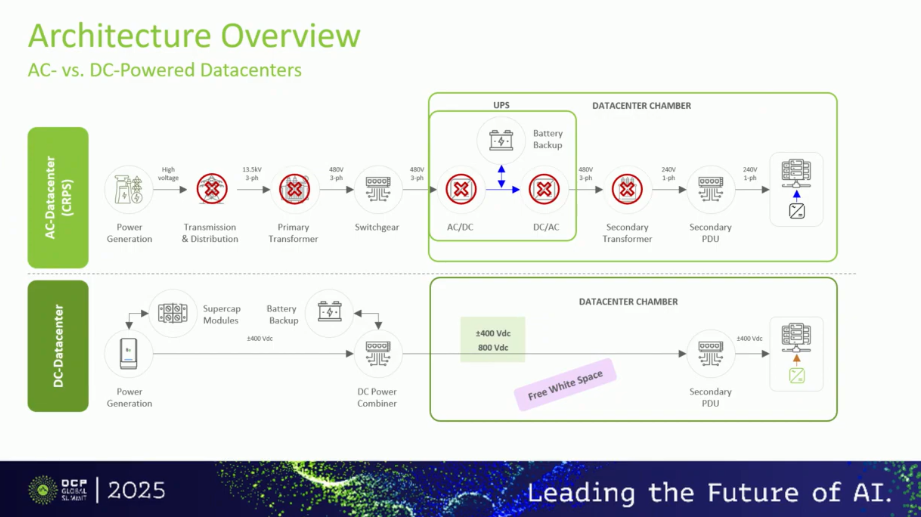

Bloom Energy’s solution removes middlemen from the distribution to the data center. For instance, AC to DC conversion is no longer needed, as Bloom’s Energy servers directly supply DC voltage to computing racks. After all, citing Nvidia’s ($NVDA) new power architecture reference paper ‘Generating 800 VDC at the facility level and delivering it directly to 800 VDC compute racks eliminates redundant conversions, improving overall power efficiency’. Moreover, onsite generation eliminates the transmission steps required in a traditional power generation setup.

Additionally, its energy server is highly modular and expands as required by its clients, the company states that it can deliver power racks of 100 MW. With the new Nvidia Rubin Architecture, 800 volts DC is the norm, and the whole so-called AI factories will be based on such power needs.

AC DC architecture comparison as explained in OCP 2025 by Bloom Energy’s CEO

Bloom’s technology current disadvantages to other technologies

It’s evident that onsite generation has implicit advantages in the AI factory era, however Bloom Energy is not the sole competitor. The traditional on site generation approach is with combustion methods, and among those exists 2 main approaches: gas turbines and reciprocating diesel or natural gas generators.

Gas turbines

Gas turbine generation uses turbines similar to those in planes to generate electricity.. This kind of approach can reach up to 37 MW per turbine. This approach is also modular, as operators can stack many turbines together to increase energy capacity. The main suppliers are GE Vernova Inc ($GEV) and Mitsubishi Electric ($6503.T).

In addition, it is important to note that current estimates set the price per kW around $2400. Gas turbine-based electric generation is cheaper than Bloom’s, estimated to be around $3000 per kW. Nonetheless, according to several reports, the current lead time for such turbines is around 7 years. Whereas, Bloom Energy has a current capacity of 1 GW and plans to set even more. By this year the company expects to reach 2GW of annual manufacturing capacity and the last earnings report also pointed out that its current manufacturing footprint is prepared to support up to 5 GW in annual output.

Reciprocating generators

In contrast, gas or diesel can fuel reciprocating generators. One of the main suppliers of this kind of technology is Caterpillar ($CAT). The technology is widely known, reliable and modular. Caterpillar products extend up to 5.7 MW generators. Compared to the gas turbines, these types of products have lower lead time and installation can also be done quickly, around 3 months. Its price per kW is also competitive, around $800 – $1200 per kW. The main disadvantage compared to Bloom’s is its lower efficiency. Bloom’s efficiency can reach up to 90%, while combustion-based generation is around 30%.

Furthermore, Bloom has at least 2 other advantages inherent to its technology. First, fuel cells have no moving parts, so maintenance is greatly reduced. On any type of combustion engine such as Gas turbines or Diesel generators, that is not the case. The second advantage is the electric output of Bloom, DC power, compared to the AC of any reciprocating engine.

Earnings and the current state of the company Q1 FY26

At first glance Blooms earning results for the first quarter of 2026 are impressive, and really show the narrative materializing. The company reported $751.1 million in revenue, a 130% increase compared to last year’s quarter. Most of this revenue, $653 million or 208% YoY, is from new sales, the remaining from services and maintenance. The major highlight for the company is that it is now profitable, with operating income improving from -$19.1 million to $72.2 million. Finally it is worth mentioning that management expects the FY26 revenue to be between $3.4B and $3.8B representing between 168% and 188% growth in revenue.

Caterpillar($CAT)

As previously established, the only available solution for the increasing power needs in the AI buildout is for onsite electricity generation. Caterpillar is probably one of the other main beneficiaries in this expansion. Its gas and diesel generators for industrial needs are rated on average at 2.5MW but expand up to 5.7 MW. Moreover, the industry giant has several manufacturing facilities dedicated for large generators. The Lafayette, IN plant already at a colossal size of 1.6 million sq.ft. is expanding to increase the capacity in large engines production.

In addition, Caterpillar has already secured contracts with several energy companies, including a multiyear contract with Atlas Energy Solutions for a total capacity for 1.4 GW. Furthermore, AIP Corp, a company focused on supplying electricity to Hyperscalers, already uses Caterpillar’s technology. AIP Corp signed a contract with Caterpillar for 2 GW of generation to be delivered before 2029. Finally it is worth mentioning that the company already has a backlog of around $51B in projects, which is why even with these large scale contracts, Caterpillar plans to duplicate its current manufacturing capacity.

A realistic approximation of current manufacturing capacity should be around 1000-3000 large generators per year, assuming an average capacity of 2.5 MW, that would be between 2.5 and 7.5 GW per year. Even if capacity doubled, the 120 GW of required electricity capacity in the US alone by 2030 remains far beyond the reach of any single company.

Author’s opinion

If Bloom energy keeps reducing its cost gap with other technologies up to the critical level of $1200 per kW, there won’t be other technologies that could rival it. If the company follows the same path of 19% YoY cost reduction, that could happen in around 5.5 years. The question is if Bloom can reach that milestone before competitors present better solutions. Another critical point for Bloom is its current manufacturing capacity. It is expected to reach 2 GW of annual output this year. However, this capacity still lags traditional approaches such as Caterpillar’s.

Honestly I see Bloom Energy as a top player in the electricity market. If it expands its customer base, increases production capacity and continues to push the limits of its technology, it will be positioned for sustained growth as the AI buildout continues to expand.

In contrast, Caterpillar presents itself as a traditional generator provider with the manufacturing capacity to meet the demand. The company’s main advantage is its current position in the market, estimated at 40% and its enormous manufacturing capacity.

Data centers and Hyperscalers require the power immediately. For me, Caterpillar is set as one of the clear winners at least in the next five years. However, its technology is not directly aligned with the newest Nvidia power architecture. This makes it technologically inferior to Bloom Energy’s approach. I expect Bloom to be relevant for the next 5 years and beyond. I believe its technology will keep maturing. The price per kW should decrease as it scales. I also expect its efficiency to improve significantly.

In my personal opinion both stocks still have the potential to be true home runs, even after their recent surges.