Two major Wall Street firms raised the bar on Bloom Energy (NYSE:BE) stock today following a blowout quarter. JPMorgan lifted its BE stock price target to $267 from $231 while keeping an Overweight rating, and Susquehanna boosted its target to $293 from $173 with a Positive rating. The dual price target raise marks a clear institutional endorsement of Bloom Energy stock as a core AI infrastructure power play.

For prudent investors, the message is that Bloom Energy’s on-site fuel cell power has moved from a niche industrial offering to a strategic asset for hyperscalers racing to plug AI workloads into the grid. The question now is whether the data center power thesis can keep compounding from here. For broader context on AI power demand, see our recent coverage of the data center electricity crunch.

| Ticker | Company | Firm | Action | Old Rating | New Rating | Old Target | New Target |

|---|---|---|---|---|---|---|---|

| BE | Bloom Energy | JPMorgan | Price target raised | Overweight | Overweight | $231 | $267 |

| BE | Bloom Energy | Susquehanna | Price target raised | Positive | Positive | $173 | $293 |

The Analyst’s Case

JPMorgan points to Bloom Energy’s Q1 2026 results being well above expectations and a fiscal year (FY) 2026 guidance increase that arrived only two months after the prior update. The firm sees margin leverage building as the business scales.

Susquehanna echoes that view, citing Bloom Energy’s beat on revenue and earnings before interest, taxes, depreciation, and amortization (EBITDA), driven by stronger deliveries and margins. Bloom Energy’s management told the analyst firm that the demand environment is accelerating as data centers chase any available power, with the FY revenue midpoint now at $3.6 billion.

Company Snapshot

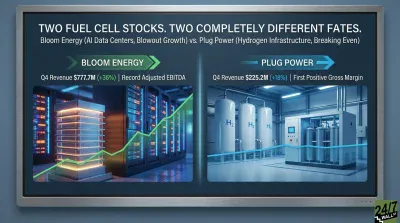

Bloom Energy designs solid oxide fuel cell systems that deliver on-site, 24/7 electricity for commercial and industrial customers. Q1 2026 revenue jumped to $751.05 million, up 130.4% year over year (YoY), with non-GAAP earnings per share of $0.44 versus $0.13 expected.

The company has 1.5 GW deployed across 1,200+ installations globally and reports a $20 billion total backlog. Bloom Energy CEO KR Sridhar said, “Bloom is rapidly becoming the standard and ‘go-to choice’ for on-site power.”

Why the Move Matters Now

The upgrades land alongside Bloom Energy’s expanded Oracle partnership, which secures 2.8 GW of capacity for AI data centers, and a $5 billion strategic AI infrastructure partnership with Brookfield Asset Management. BE stock has rallied, with a year-to-date advance of 161%.

The Bloom Energy bull case rests on accelerating fuel cell demand, raised FY 2026 guidance of $3.4 billion to $3.8 billion, and gross margin expanding toward ~34%. The bear case centers on capital intensity, deployment timing, tariff exposure, and the risk that hyperscaler capex eventually moderates. For context, the broader analyst consensus target price sits at $166.96 for BE stock, well below where JPMorgan and Susquehanna now stand.

What It Means for Your Portfolio

Bloom Energy stock offers genuine exposure to one of the most concrete AI bottlenecks: power delivery. The price target raise from both firms reflects rising confidence that fuel cells solve a problem grid operators cannot.

For long-term investors, the analyst upgrade signals warrant a closer look at Bloom Energy, though position sizing should account for a beta of 3.185 and rich forward P/E ratio of 164x. Watch for whether Bloom Energy’s margin leverage holds as manufacturing capacity ramps toward 2 GW.