Finance expert Suze Orman warns a common mistake can cost you big money in retirement.

That includes focusing more on wants than what you need, as she explains in this video.

In fact, according to Orman, she could afford to buy a more expensive apartment, but she didn’t need it. And if people apply that way of thinking of needs instead of wants, their lives could dramatically change. The financial guru also challenged people to buy only the things they need and not want for the next six months to see an impressive transformation.

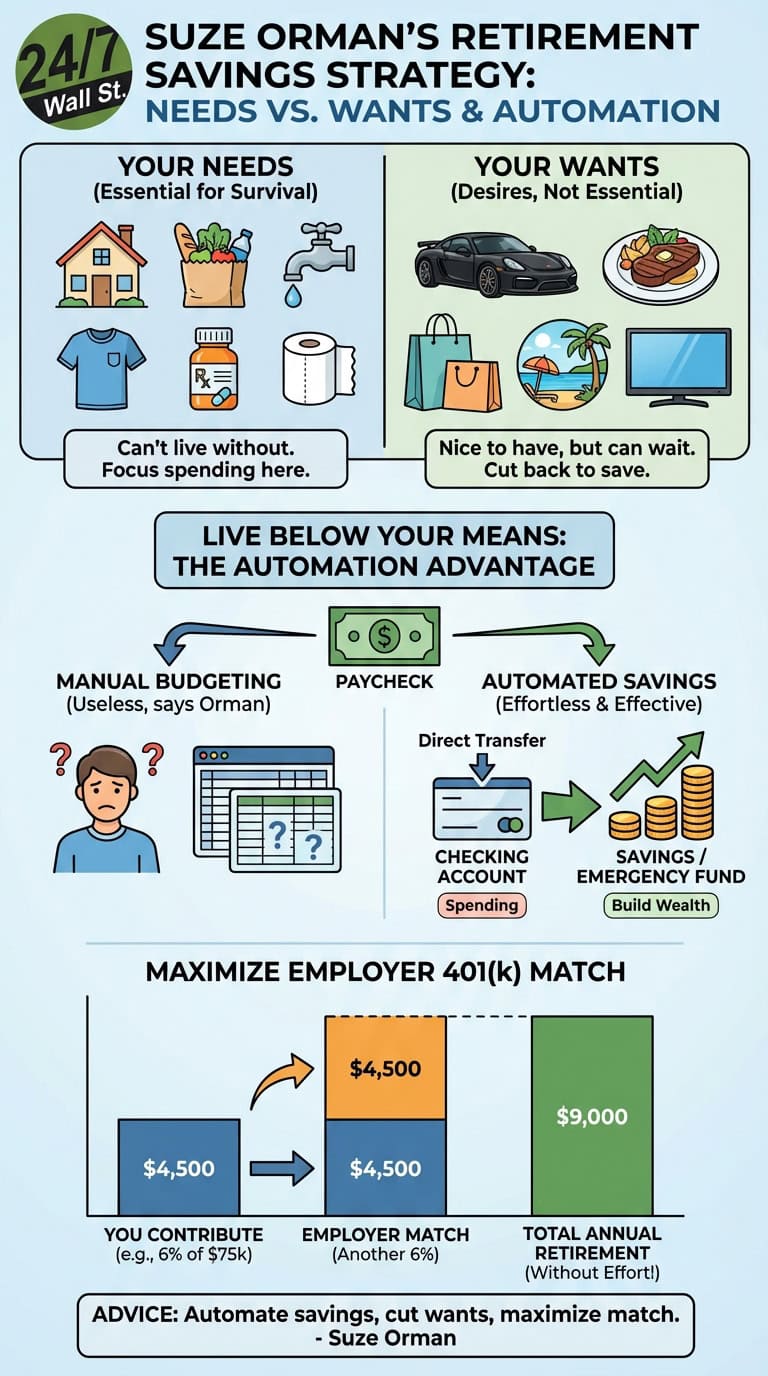

Your Needs vs. Your Wants

Needs are things you and your family can’t live without. That includes food, water, shelter, clothing, medication, and toilet paper, which came under substantial demand a few years ago.

Wants are your desires, which aren’t really needed to survive.

I’d love to buy a black Lamborghini, which can cost about $230,000. But I don’t need it. Plus, I’m not a big fan of getting in a car and sitting on the floor essentially. And sure, you need food to function. But you don’t need a Ruth Chris steak every night of the week, which can set you back about $150 a night. It’d be nice to have, but it’s not a top need.

In short, by cutting back on your wants, you have much more money in your pocket.

Live below your means and within your needs

Suze Orman also believes the most important thing to do is live below your means and within your means. While budgeting and creating a list are often suggested, Orman says she’s not a fan of budgeting. She finds them to be useless.

Instead, she argues you should automate the process of saving money. Arrange for an automatic transfer so that every time you’re paid, a portion goes to checking and a portion goes directly into savings. By doing so, you can help build your overall savings and even create an emergency fund account, which many people do not have.

You can even take advantage of your employer’s 401(k) match program.

If you have an employer that will match your 401(k), maximize your contributions up to the amount your employer will match. If your employer will match up to 6% of your salary, maximize that. If you earn $75,000 a year, and you contribute 1%, that’s $750 for retirement. If your employer matches that, you have $1,500 for retirement per year. If you contribute 6% and your employer matches that, that’s about $6,750 in retirement per year.

Another good idea is to check in with your financial advisor for more suggestions.