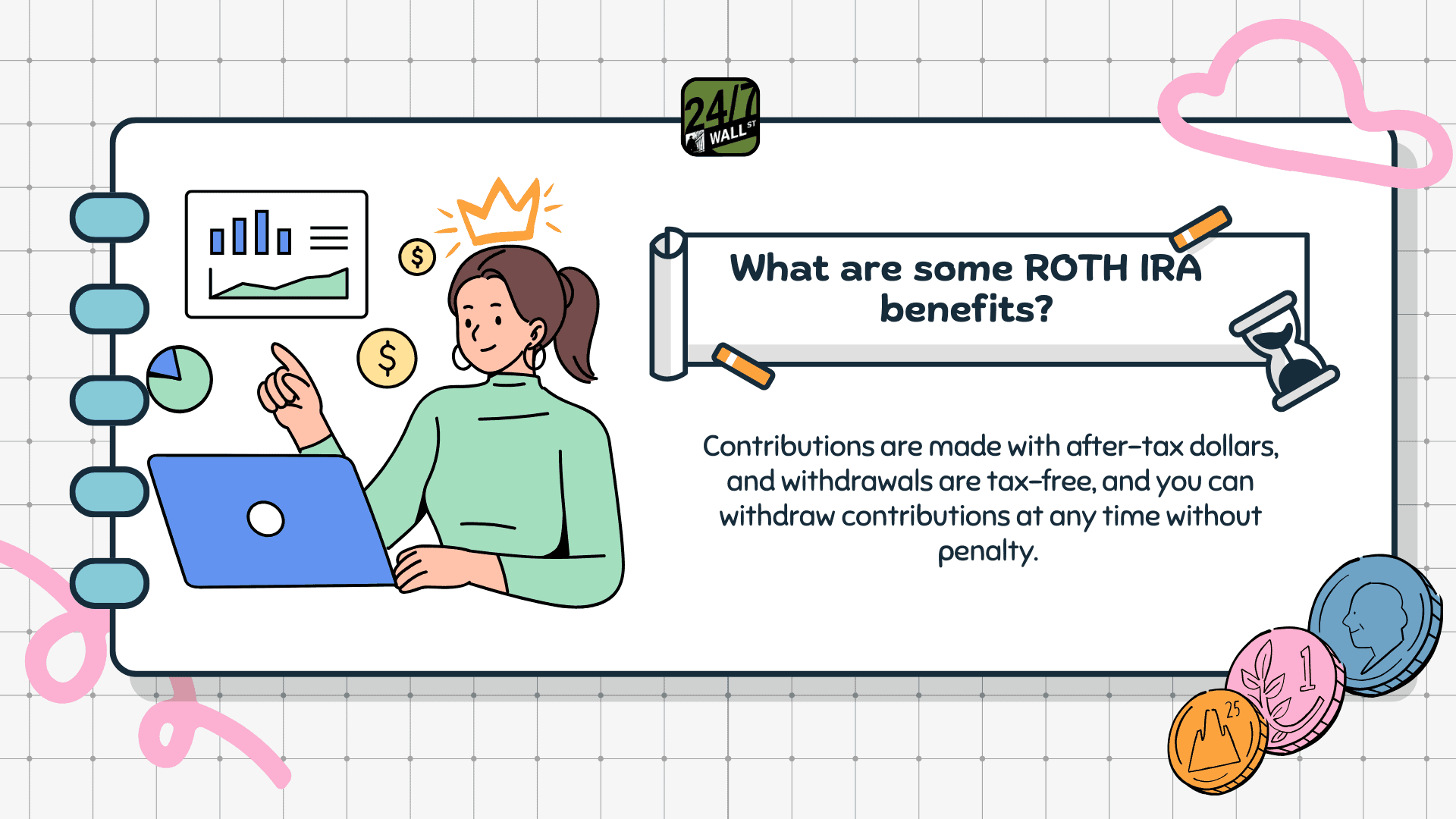

Traditional retirement accounts offer immediate tax relief, while Roth accounts come from pre-tax contributions. However, Roth retirement accounts have become more popular among young investors since they shield capital gains and dividends from taxation.

A Redditor has done their research and is considering moving funds from a 401(k) account to a Roth IRA. This individual has a gross salary of $84k and recently paid $20k in taxes bill. The Redditor currently has $117k in an Empower 401(k) that invests in four mutual funds.

Does it make sense for the Redditor to move their 401(k) funds into a Roth account? I’ll share my thoughts, but it is always good to speak with a financial advisor if you can.

Tax-Free Gains Create Less Uncertainty

One of the disadvantages of 401(k) plans is that your withdrawals get taxed. That makes it more difficult to plan for retirement since a $1 million 401(K) isn’t really $1 million. Sure, you can take out less money when you retire to ensure you have a low tax rate, but it still creates uncertainty, especially if you work for longer than expected.

Meanwhile, a Roth account offers tax-free gains. The Redditor currently has a $117k 401(k) portfolio. Assuming this was a Roth account that maintained an annualized 8% return over 30 years, it would become a $1.2 million portfolio. That’s not including any additional contributions.

It’s much better to have $1.2 million tax-free than it is to have those funds locked up in a traditional 401(k). Sure, the Redditor will take a tax hit when they withdraw funds from their 401(k), but it’s worth it in the long run.

Gradual Withdrawals Are Better Than Entire Withdrawals

The one problem with moving all of your funds from a 401(k) to a Roth IRA is that those funds are treated as ordinary income. If you move $117k, you will have to report $117k in income on top of what you already make. Moving everything over at once will result in a higher tax bill, but there is a solution.

The Redditor can opt to move $10k-$15k per year to minimize their tax burden. If the Redditor gets laid off or fired, they can use that one year to make a bigger transfer to their Roth account since they’ll report a lower taxable income. While this isn’t the best-case scenario, it’s good to keep this in mind in case it happens.

Are the Growth Funds Good?

The Redditor mentions four funds that he has in his portfolio:

- Fidelity 500 Index Fund (MUTF:FXAIX)

- Fidelity Blue Chip Growth Fund (MUTF:FBGRX)

- Fidelity Extended Market Index Fund (MUTF:FSMAX)

- DFA U.S. Targeted Value Portfolio Institutional Class (MUTF:DFFVX)

These funds have delivered respectable returns over the years. However, I would also add the Fidelity Nasdaq Composite Index Fund (MUTF:FNCMX) to the mix. This fund tracks the Nasdaq Composite and has outperformed the Redditor’s other funds.

The Nasdaq Composite is for investors who are willing to take on more risk in exchange for a higher potential reward. However, it’s outperformed the S&P 500 for more than two decades. That trend has continued over the past five years.

I would consider putting the funds from FSMAX and DFFVX into FNCMX, as the Nasdaq fund has consistently outperformed the other two by wide margins. For instance, FSMAX is up by 37% over the past five years, while DFFVX has gained 48% over the past five years. During that same 5-year stretch, FNCMX has soared by 105%.