Flywheel Publishing has partnered with CardRatings for our coverage of credit card products. Flywheel Publishing and CardRatings may receive a commission from card issuers.

24/7 Wall St Key Takeaways:

- Many people aim to retire early but making that transition can be understandably hard mentally. Even if all the numbers work out, it isn’t uncommon for those with financial independence to question the jump to retirement.

- Coming into sudden wealth means learning how to manage that wealth, which is completely different from accumulating wealth!

- Also: Smart spenders know a top rated cash back card is free money. You can see our favorite cash back credit cards here.

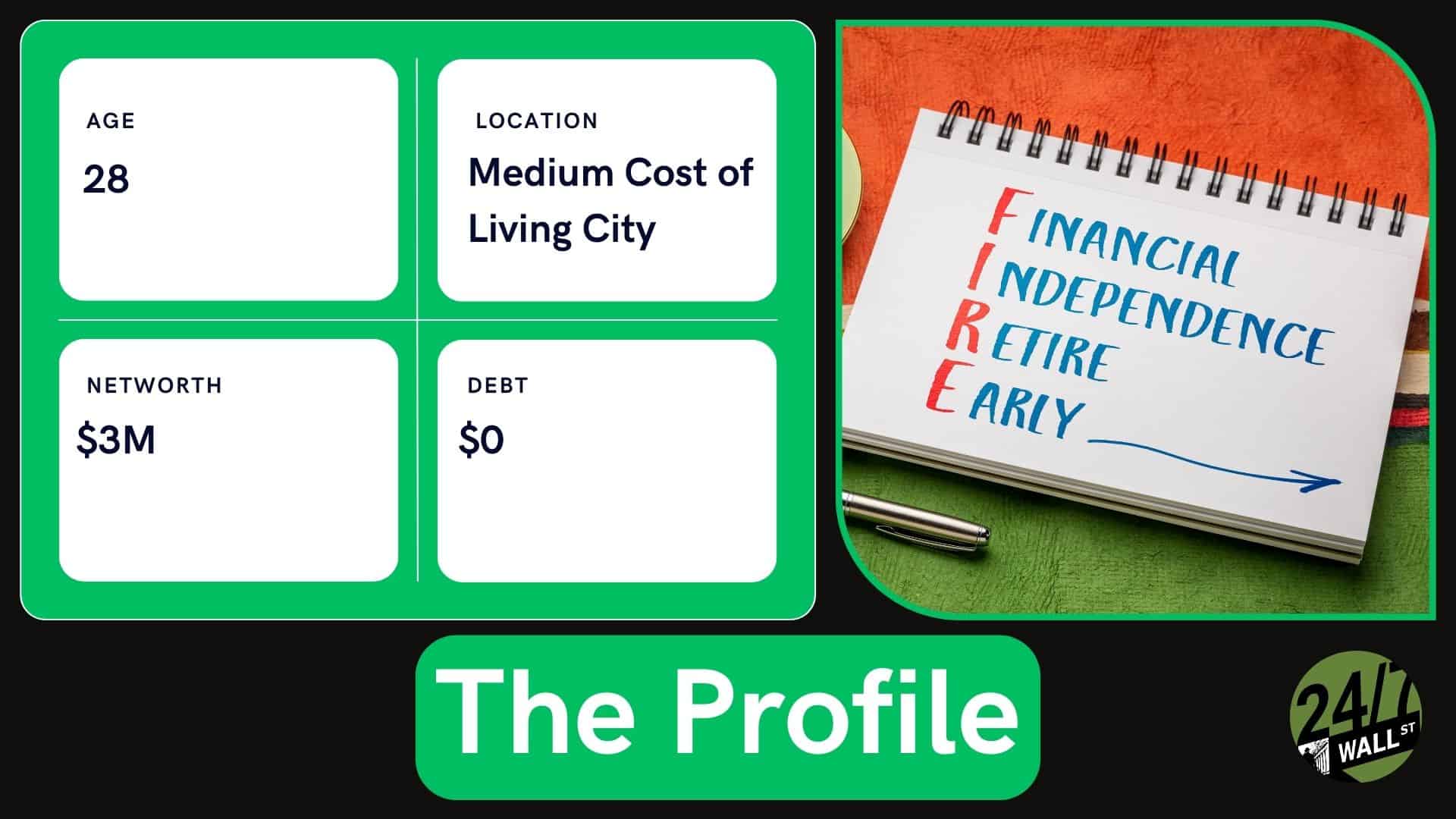

Reaching financial independence (or even anything resembling financial independence) at 28 is a huge achievement. However, it does bring out some interesting considerations. A recent Reddit post I came across highlights the challenges of moving from accumulating wealth to managing it effectively.

Whether you’re just starting your FIRE journey or nearing your goal, there’s something everyone can learn from this milestone. Practically everyone will need to manage their wealth at some point.

I’ll cover some of my suggestions below. Remember, these are just my suggestions, not financial advice.

This post was updated on November 7, 2025 to clarify the recommended balanced approach to taxable accounts like 401(k)s.

1. Diversification is Key to Long-Term Security

The poster’s $3M net worth is heavily concentrated in one investment with significant unrealized gains. This is a huge problem. While the concentrated position could grow wealth quickly, it also adds a lot of risk. It could go down quickly, too.

Diversify to protect your portfolio from volatility, especially if you’re planning to live on your wealth.

2. Seek Professional Guidance for Big Decisions

This Redditor knows he probably needs professional advice for their finances. However, he doesn’t know who he’s supposed to go to!

For those with significant wealth, consult a fiduciary financial advisor or a tax professional to explore options like tax-efficient selling or hedging strategies. You’ll preferably want an advisor with some understanding of early retirement.

3. Taxable Accounts Offer Flexibility

The poster has about $170K in a 401(k) and $60K in a taxable brokerage account, and wonders whether continuing 401(k) contributions makes sense given his overall wealth.

It usually does. Contributing to a 401(k) still lowers taxable income and allows investments to grow tax deferred. However, maintaining and growing a taxable brokerage account is also valuable—especially for someone considering early retirement. Taxable accounts can provide penalty-free access to funds before age 59½, offer more control over realized gains and losses, and enable tax-efficient withdrawals.

A balanced approach is key: maxing out any 401(k) match while steadily building the taxable account. This strategy provides both long-term growth and short-term flexibility.

4. Understanding Sequence of Returns Risk

The Redditor currently has around $30K in annual expenses, which is very low. However, he expects this to increase substantially as his life progresses. A family and kids can easily double those expenses.

Transitioning into early retirement requires planning for these higher future expenses and potential market downturns. To minimize risks, a conservative withdrawal strategy must be built.

5. Ease Into Lifestyle Adjustments

The poster is considering taking a temporary leave from work but is hesitant about permanently leaving a stable income source. Leaving a job that you find stable is a huge risk. Anxiety over making the jump to retirement is extremely common.

That said, I do recommend part-time work or sabbaticals before fully retiring, especially if you have anxiety over the transition. This allows you to test the waters before jumping right in.

Flywheel Publishing has partnered with CardRatings for our coverage of credit card products. Flywheel Publishing and CardRatings may receive a commission from card issuers.