It won’t come as any surprise to learn that millions of Americans are trying to put money away for retirement, with varying degrees of success. Unfortunately, the number of people behind is shockingly high, putting millions at risk of not enjoying their retirement years.

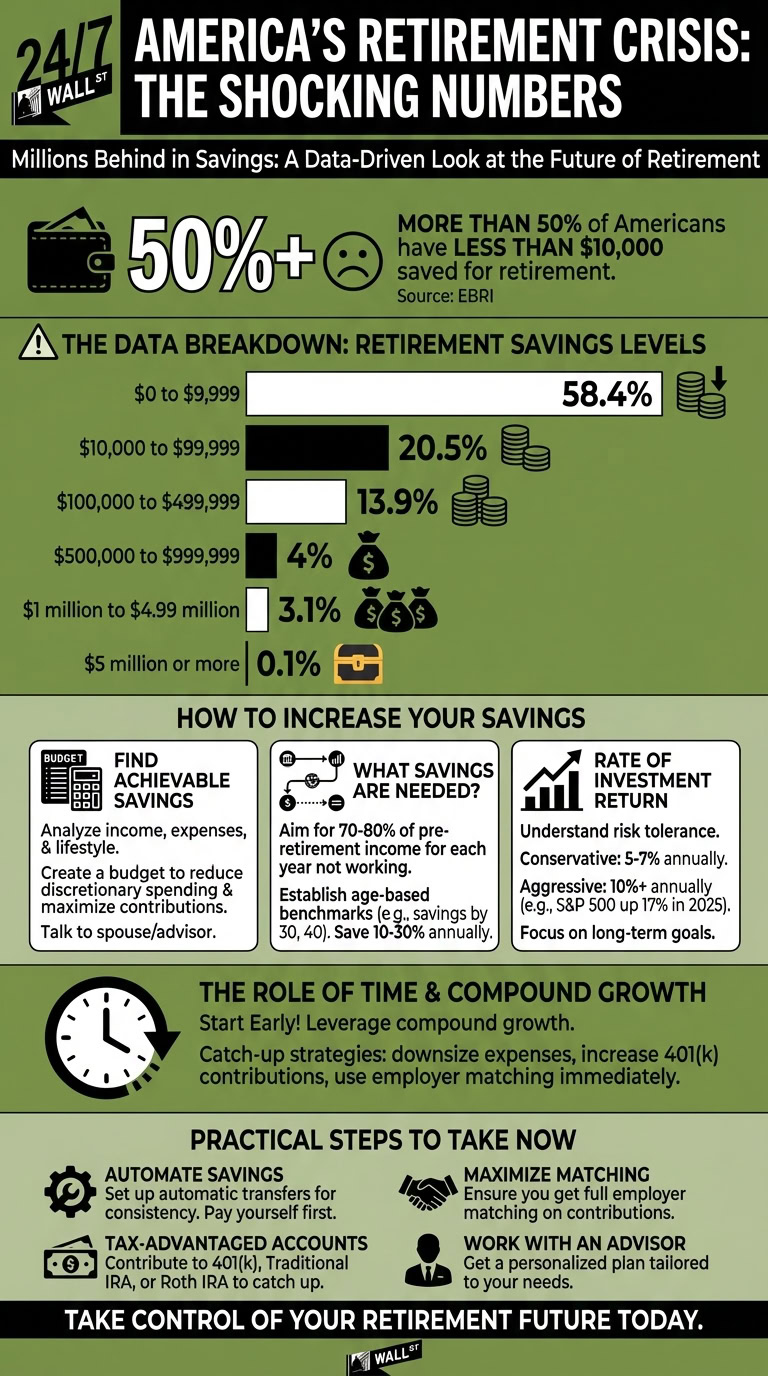

According to the Employee Benefit Research Institute, more than 50% of Americans have less than $10,000 saved for retirement. This is a big concern, especially considering how shocking it is that a much smaller number have more than $500,000 tucked away for retirement.

The Data Breakdown

When you look at the data breakdown provided by the research, there is no question that it will shock people of all income and savings levels. According to the study, it found the following amounts are currently in American’s retirement accounts:

- $0 to $9,999: 58.4%

- $10,000 to $99,999: 20.5%

- $100,000 to $499,999: 13.9%

- $500,000 to $999,999: 4%

- $1 million to $4.99 million: 3.1%

- $5 million or more: 0.1%

Given these numbers, it’s essential to consider how you can increase your retirement savings.

Find Achievable Savings Numbers

When the time comes, you should sit down with your spouse or a financial advisor and consider how much you can save immediately. This would include your current income level, expenses, lifestyle choices, etc.

Knowing your financial position, you can consider maximizing savings without entirely sacrificing your quality of life. This might include creating a new budget focused on reducing discretionary spending that can be put into savings instead.

What Kind Of Savings Are Needed?

As you look at what kind of financial injection you need to move yourself from one savings level to the next, you must consider what number you really need. As a general rule of thumb, you want to put aside around 70-80% of your pre-retirement income for every year you consider not working. This could mean establishing a baseline where you put 10%, 20%, or even 30% of your net income annually into a retirement account.

This is understandably a not-so-insignificant amount of money, which goes back to creating a new budget and looking at where you can cut out unnecessary spending. You should try setting up savings benchmarks for different ages so you know how you are progressing. In other words, turning 30 means you want X dollars put aside. By the time you turn 40, you want Y dollars set aside, and so on.

Rate of Investment Return

One of the most significant factors that will help you move into another savings space is understanding how the rate of investment return affects your growing retirement savings. You need to think through what kind of return you are comfortable with, as some people are more risk-averse and may want to set up a portfolio with a financial advisor that looks to earn between 5-7% annually.

On the other hand, if you have the stomach for riding out market volatility, you can be more aggressive and look to achieve a 10% annual return. So far in 2025, the S&P 500 is up 17%, so it’s not impossible to achieve a 10% return, but it does come with the downside of taking on more risk. This would mean you are okay with market corrections and remain focused on the long-term goals.

What Role Does Time Play?

If you’re worried about timing, and you may be closer to retirement than your first day of corporate life after college, you have to consider the role of time in retirement planning. The bottom line is that the earlier you start, the more likely you will take advantage of compound growth.

You can also consider what strategies are available for starting later to catch up, which ties directly back to downsizing expenses. This could also mean upping the money you contribute to a 401(k) account and ensuring you take advantage of employer matching to maximize your savings opportunities immediately.

Practical Steps You Can Take

You should already know some practical steps you can take to catch up. First and foremost, make sure you automate savings to ensure consistency and that your budget plan allows these savings to be the first thing you put aside with every pay period.

The second significant consideration is jumping into any tax-advantaged accounts like a 401(k), Traditional IRA, or even a Roth IRA to help you start catching up with retirement savings. Don’t forget the importance of working with a qualified financial advisor who can create a personalized plan that is right for you.