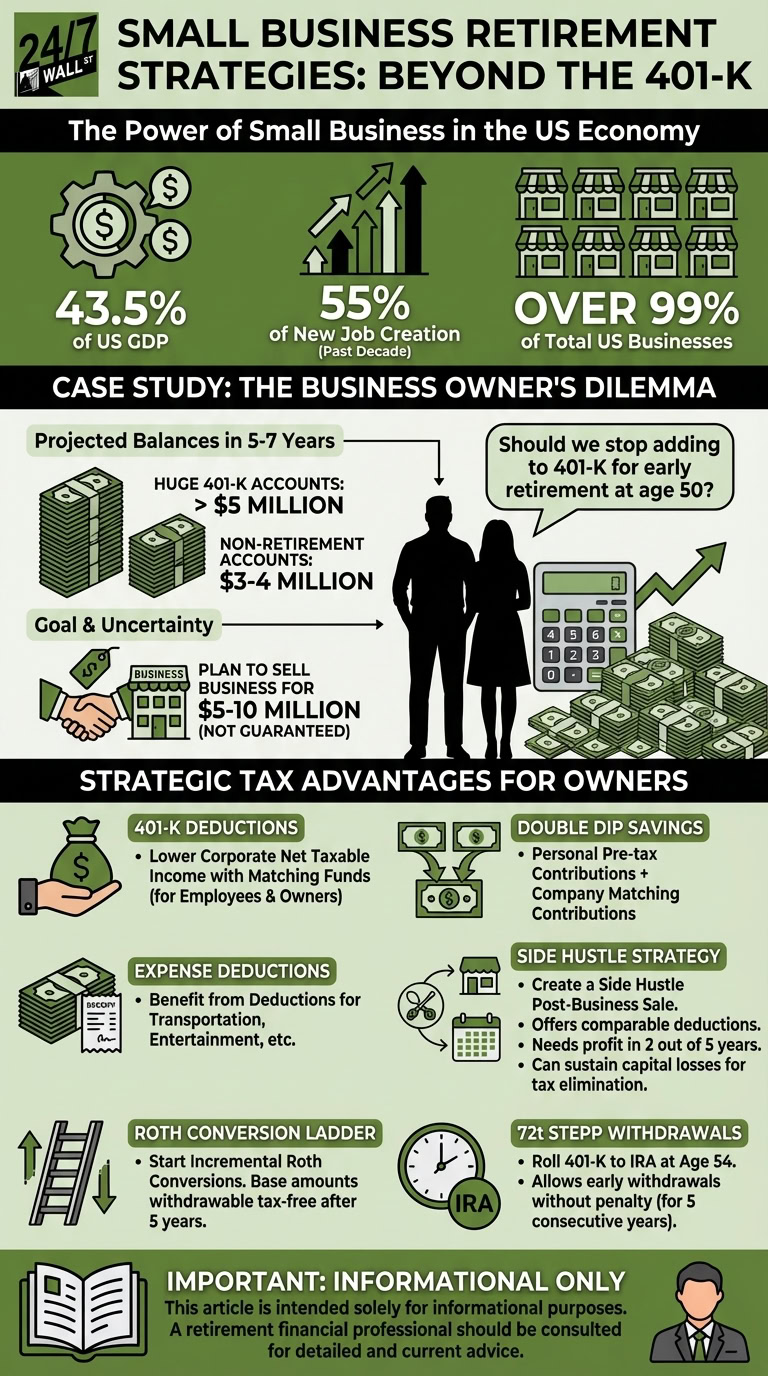

Entrepreneurs and small businesses are the crucial component of a thriving, capitalism-based market economy. Small businesses account for 43.5% of US GDP, 55% of new job creation in the past decade, and over 99% of total US businesses.

Due to how tax laws were originally written to help foster entrepreneurism, there are other options that small business owners have available to them that salaried workers for larger companies cannot access, especially when it comes to handling retirement funds.

Business Owner’s 401-K and Non-Retirement Investment Imbalance?

A Reddit poster in his 40s was trying to solicit advice. Although his details are minimal, he cited the following scenario:

- Both his and his wife’s 401-K accounts were huge, relative to their non retirement brokerage accounts.

- In the next 5-7 years, he anticipated that the 401-Ks would cumulatively hold over $5 million.

- By the end of that same time period, he expects that their non-retirement brokerage accounts will hold $3-4 million.

- The poster and his wife own their own business, and plan to sell it for between $5-10 million 5-7 years into the future, however, it is not a sure thing.

- The poster asked whether or not it was a good idea to stop adding to their 401-K accounts in light of their plans to retire close to age 50 with the eventual sale of the business and the relatively low post-tax holdings vs. the pre-tax 401-K accounts.

Small Business Retirement Account Strategies

While it is not explicit, the nature of the poster’s query implies that he is looking at the 401-K account from the perspective of an employee, and not from the broader one of a small business owner. As a result, some of the responses that he can choose to incorporate for his and his wife’s use should be looked at in a larger equation to evaluate how helpful they might be. Some of the aspects of his scenario that he seems to overlook include:

- The IRS allows for small business owners to deduct 401-K account matching funds from gross revenues, thus lowering the company’s corporate net taxable income. This includes matching contributions for any employees, as well as for themselves.

- As the poster and his wife presumably take the largest salaries in their company, they each get an annual savings “double dip” by contributing personal salary pre-tax income plus the company 401-K matching contributions for their retirement accounts.

- Small businesses routinely are allowed a range of other deductions by the IRS, such as for transportation, entertainment, and other expenses, which the poster and his wife also benefit from, while the business is still an ongoing concern.

- In anticipation of retirement in the next 7 years, the poster should consider creating a side hustle from a hobby or pastime that can be declared a primary occupation after the company business is sold. The side hustle can offer comparable business deductions, and the lower personal tax bracket will allow for larger take-home withdrawals from the pretax 401-K account. The side hustle needs only to make a profit in 2 out of 5 years for the IRS to approve of its status for tax purposes. Therefore, some years can prospectively sustain capital losses to eliminate taxes completely and even entitle one for a tax refund.

- While still contributing to the 401-K, there is nothing to stop the couple from starting an incremental Roth conversion ladder. This allows for the base amounts to be withdrawn tax free after 5 years from the date of each conversion.

- Once each person reaches age 54, they can roll 401-K account proceeds into an IRA and qualify for a 72t STEPP, which allows for early withdrawals without tax penalty as long as the same amount is withdrawn for 5 consecutive years.

This article is intended solely for informational purposes. A retirement financial professional should be consulted for more detailed and current advice.