A lot of people reach retirement age without much money in savings. But if you worked hard and saved well, you may be in a very different position. And if you’re retiring with a respectable nest egg, it’s important to know how to manage it.

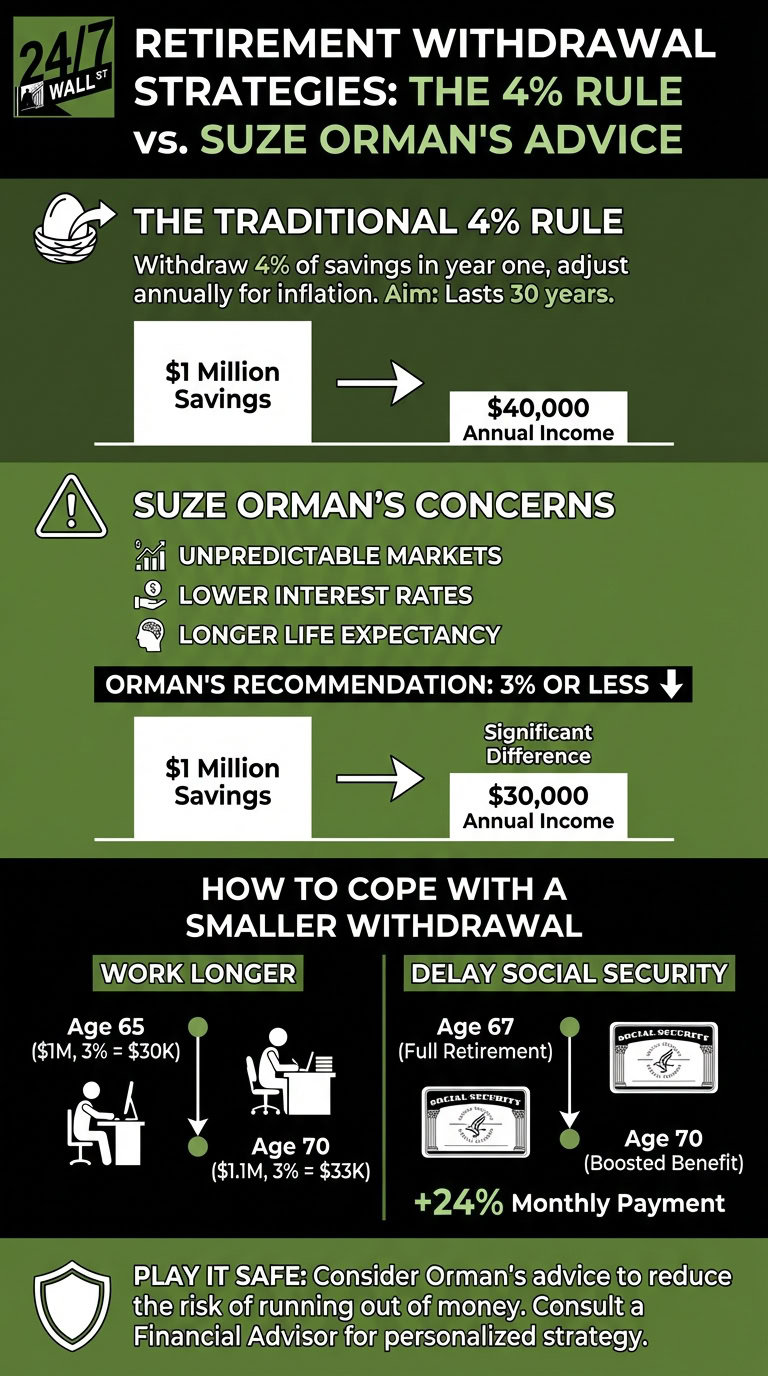

Many financial experts recommend using a strategy called the 4% rule. The rule has you withdrawing 4% of your savings balance your first year of retirement and adjusting future withdrawals for inflation.

It’s a strategy that, if all goes well, should be conducive to having your savings last for 30 years. But while a lot of financial insiders are fans of the 4% rule, Suze Orman is not.

Orman thinks the 4% rule no longer works for today’s retirees and recommends a different approach to managing savings.

Why Orman think the 4% rule is a problem

The 4% rule makes a number of assumptions that could render it less effective. It assumes a fairly even mix of stocks and bonds and certain market conditions.

Orman thinks markets are unpredictable, interest rates aren’t what they were back when the 4% rule was established, and Americans are living longer. This combination makes the 4% rule a bit dangerous, in her opinion.

Orman therefore recommends starting with a 3% withdrawal rate, or even less, depending on how your portfolio is invested.

What does that mean for you?

Let’s say you retire with $1 million in savings. With the 4% rule, you’d be looking at about $40,000 a year in income from your portfolio.

With a 3% withdrawal rate, you’d be looking at $30,000 a year. Clearly, that’s a huge difference, and one you may need to take steps to compensate for.

How to cope with a smaller withdrawal rate

One of the biggest fears you might have in the context of retirement is that your money will eventually run out. That’s why it’s important to withdraw from your savings carefully.

That said, it’s not easy to accept a lower income than what you’re hoping for. To compensate, Orman has a few suggestions.

First, she recommends working longer. This could allow you to boost your savings so that if you end up sticking to a smaller withdrawal rate, it’ll result in more annual income.

For example, let’s say you’ve saved $1 million by age 65, which is your planned retirement age, but you push yourself to work until age 70. In doing so, you might manage to grow your portfolio to $1.1 million.

In that case, a 3% withdrawal rate gives you $33,000 a year, as opposed to the $30,000 you’d have with a $1 million balance.

Next, Orman recommends that people delay claiming Social Security until age 70 if possible. Claims that are delayed past full retirement age result in boosted benefits.

Age 70 is when you stop getting credit for holding off on Social Security. But if your full retirement age is 67 and you wait until 70 to sign up, you can boost your monthly payments by 24% on a permanent basis.

Having more Social Security is another great way to make up for smaller withdrawals from your savings.

All told, you don’t want to risk having your money run out during retirement. The 4% rule is supposed to prevent that from happening, but Orman isn’t convinced. If you want to play things safe, you may want to heed her advice.

It’s also a good idea to talk to a financial advisor about your situation. They can look at your portfolio makeup, your income needs, and market conditions to suggest a withdrawal rate that’s most suitable for you.