What took place on Friday is going to potentially destroy the mindset of all investors who bought into this story any time since the IPO. How many people want to think of new IPOs with growth prospects galore as a value prospect? Class action suits seem more than just likely here.

On top of the earnings, Fairway announced that CEO Herbert Ruetsch will retire after fifteen years with the company. His leadership is what helped manage the transformation from a small family business into a specialty growth retailer. He will remain as a special advisor to the company, but that is far from running day to day growth operations.

The company reported that net sales increased $38.4 million, or 22.9%, to $205.7 million. The problem is that Same store sales, excluding the Red Hook store, decreased 1.7% in the quarter – with the blame placed on the compressed holiday shopping period and also the prior year’s impact from Hurricane Sandy previously helping its figures. Fairway ended the quarter with approximately $73 million of liquidity ($54 million of cash and $18 million in borrowing capacity under the senior credit facility).

Multiple analyst downgrades were seen on Friday:

- cut to Hold from Buy at BB&T;

- cut to Market Perform from Outperform at BMO Capital Markets;

- cut to Underperform from Neutral at Credit Suisse;

- and cut to Perform from Outperform at Oppenheimer.

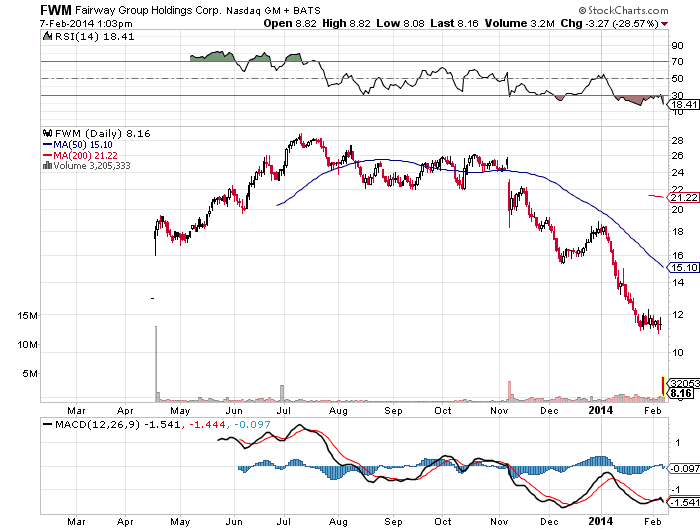

Fairway shares were down 21% after earnings in early Friday trading, and the stock was down over 28% to $8.15 by mid-afternoon on Friday. This marked a new post-IPO low for company, and that old $23 consensus price target from analysts is now history. Thursday’s closing price was $11.43, and that was already down well over half from its post-IPO high of $28.87.

The chart below shows just how bad this story has become. Every single investor who bought this stock at the IPO and since the IPO is now buried. Some investors are likely buried much deeper than the traditional six feet under.