By Gene Munster and Will Thompson of Loup Ventures

Tesla released Sep-18 production and delivery numbers this morning. While the numbers were in line with guidance, the update is incremental, given Tesla investors have been conditioned to brace for negative news. This is a good day for Tesla. The focus now shifts to the Sep-18 earnings report (likely late this month), specifically the update on cash flow and profitability.

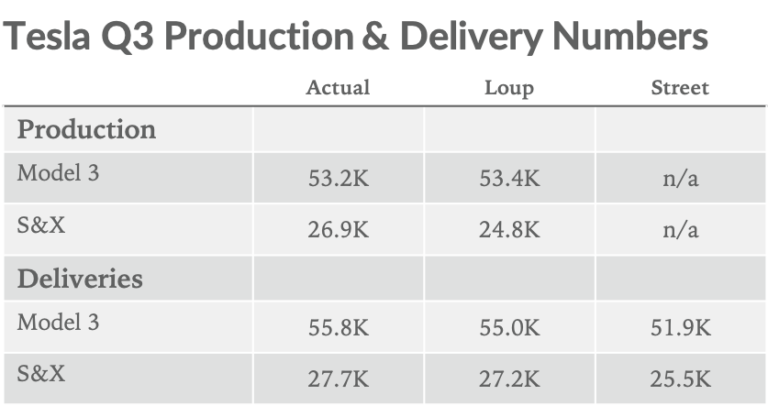

- Model 3 production totaled 53,239 vs Loup estimates of 53,398, compared to 28,578 in the Jun-18 quarter.

- Model 3 deliveries totaled 55,840 compared to the Street at 51.9K.

- S&X production totaled 26,903 vs Loup estimates of 24.8K.

- S&X deliveries totaled 27,660 compared to the Street at 25.5K

- Average weekly Model 3 production increased to 4,095 vehicles from 2,198, an 86% q/q improvement.

[nativounit]

Vehicles in transit this quarter totaled 11,824, compared to 15,058 in Jun-18. While Jun-18’s high number could be attributed to gaming the U.S. tax credit, this quarter highlights the issue of delivering cars to customers at volume without a dealer network. This is a lower-order challenge and we don’t believe it will impact the company’s goal to sustain profitability.

The Cash Flow and Profitability Question Remains

As expected, Tesla did not include updates on cash flow and profitability in today’s announcement. Those details will be part of the formal Sep-18 earnings report. We believe, based on the level of Model 3 deliveries, of which 11.1K were vehicles in transit from the Jun-18 quarter, the company will likely be cash flow positive (excluding the impact of non-recourse lease financing) and slightly profitable. This is a step in the right direction, but more work remains. Specifically, the Dec-18 quarter will not enjoy quite as much of a vehicles-in-transit tailwind, and the Mar-19 quarter will face a demand headwind form the declining U.S. tax credit.

Cash on Hand

We estimate Tesla needs about $1.5B on hand to sustain operations, and they ended the Jun-18 quarter with about $2.3B. Conceptually as production volume grows faster than receivables in 2019, minimum cash needed to sustain operations will likely increase to our estimate of ~$2B. Bottom line is cash is tight. Based on today’s updated numbers, we expect the cash balance in Sep-18 to increase slightly. This assumes Model 3 will reach its target of 15% gross margin.

Tesla, of course, has three looming convertibles notes that are due in the next year, which will impact cash. The first is $230M due in November (conversion price is significantly out of the money), for which the company is sufficiently funded to service. The second is $920M due in March of 2019 (convertible at $360). Following the Dec-18 quarter, we expect the company will have cash on hand to service the $920M note. There is also a chance the debt converts if the share price is above $360 on the due date. The last note due in the next year is $566M due in November of 2019. Similar to the November ’18 note the conversion price is significantly out of the money.

[recirclink id=496599]

Disclaimer: We actively write about the themes in which we invest or may invest: virtual reality, augmented reality, artificial intelligence, and robotics. From time to time, we may write about companies that are in our portfolio. As managers of the portfolio, we may earn carried interest, management fees or other compensation from such portfolio. Content on this site including opinions on specific themes in technology, market estimates, and estimates and commentary regarding publicly traded or private companies is not intended for use in making any investment decisions and provided solely for informational purposes. We hold no obligation to update any of our projections and the content on this site should not be relied upon. We express no warranties about any estimates or opinions we make.

[wallst_email_signup]