Our SoFi Technologies (NASDAQ:SOFI | SOFI Price Prediction) thesis comes down to a simple question: how much should investors pay for a digital bank growing members 35% per year while the market punishes a single soft segment? After Tuesday’s brutal post-earnings session, our model says the selloff went too far.

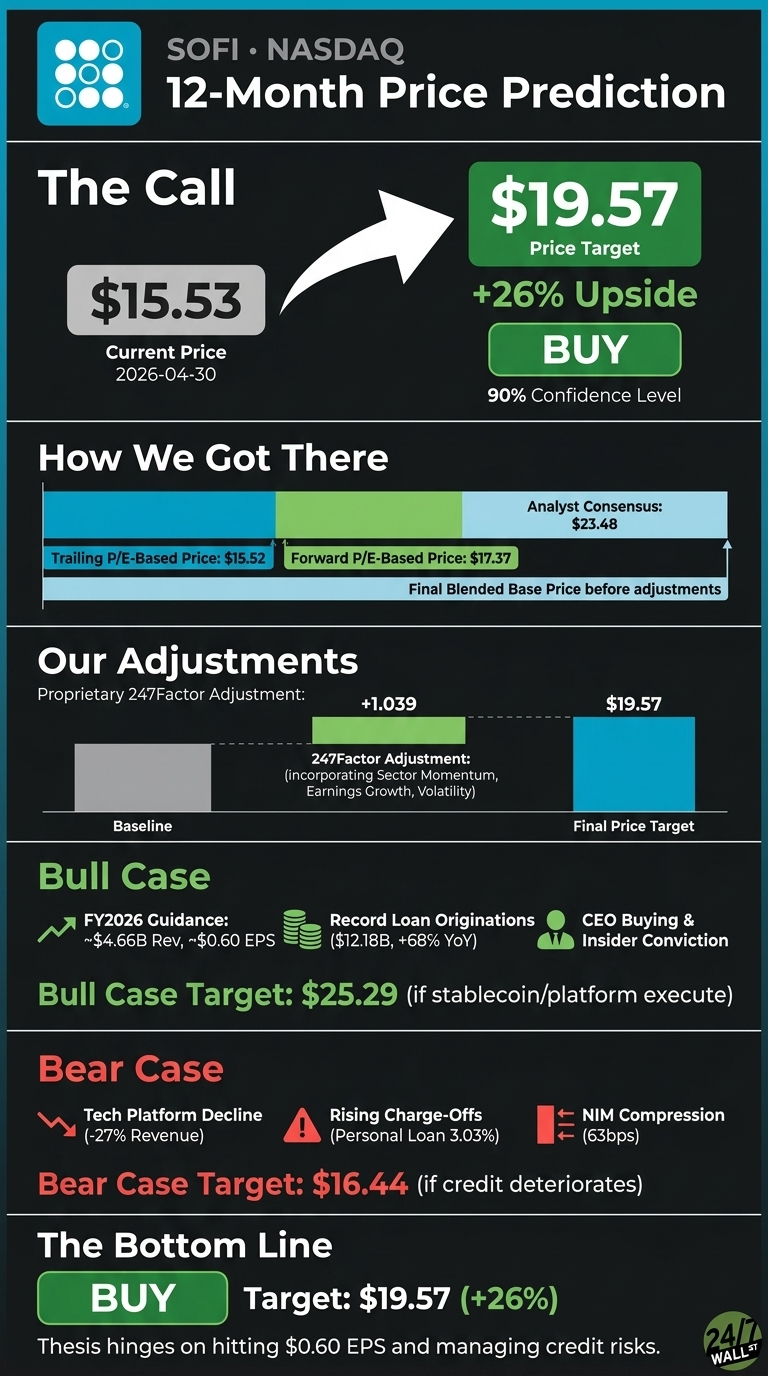

The 24/7 Wall St. price target for SoFi is $19.57 over the next 12 months, implying 26.05% upside from $15.53. Our recommendation is buy with high conviction (90% confidence).

24/7 Wall St. Price Target Summary

| Metric | Value |

|---|---|

| Current Price | $15.53 |

| 24/7 Wall St. Price Target | $19.57 |

| Upside | 26.05% |

| Recommendation | BUY |

| Confidence Level | 90% |

An Earnings Beat That Traded Like a Miss

SoFi reported Q1 2026 on April 29, 2026, posting revenue of $1.10 billion, beating consensus by 5%, with EPS of $0.12 in line with estimates. GAAP net income jumped 134.45% and loan originations hit a record $12.18 billion, up 68% YoY. Yet shares fell 15.44% on the day.

The culprit: Technology Platform revenue declined 27% on a large client departure, and net interest margin compressed 63 basis points. SOFI is now down 40.7% YTD and sits between its 52-week high of $32.73 and low of $12.43.

The Case for $25 and Beyond

Bulls have plenty to point at. Management guided FY2026 adjusted revenue of $4.66 billion (30% growth), adjusted EBITDA of $1.6 billion, and adjusted EPS of $0.60. Deposits reached $40.24 billion, funding over 90% of liabilities at lower cost.

CEO Anthony Noto noted, “We had an excellent Q1 delivering another quarter of durable growth and strong returns, fueled by our relentless focus on innovation and brand building.”

Our bull-case 12-month scenario hits $25.29 (62.87% return) if the SoFiUSD stablecoin, Mastercard partnership, and Loan Platform Business (running at a $15B annualized pace) re-rate the multiple.

Director Steven Freiberg’s 250,000-share purchase and Noto’s 84,900 shares of open-market buying signal insider conviction.

What Could Go Wrong

The bear case centers on credit and the Tech Platform. Personal loan charge-offs ticked from 2.80% to 3.03%, and student loan charge-offs rose to 0.65%. Galileo’s 27% revenue drop is the real overhang. With a beta of 2.251 and a forward P/E of 31, any slip on the $0.60 EPS guide could compress the multiple fast.

That said, bulls would counter that the Tech Platform decline is one client and that $3.6 billion in new Loan Platform commitments more than offsets it. Our bear-case 12-month price is $16.44, only modestly below today.

The Setup From Here

The 24/7 Wall St. price target of $19.57 reflects a buy rating at 90% confidence. The tipping factor: a 30% growth bank trading at a forward multiple that no longer prices in the guide.

The bull thesis hinges on stomaching the 2.251 beta and management hitting the $0.60 adjusted EPS target. The thesis breaks if personal loan charge-offs breach 3.5% or Tech Platform losses spread to a second major client.

SoFi Price Prediction 2026-2030

Looking further ahead, here is where our 24/7 Wall St. price target model projects SoFi could trade, assuming management hits its medium-term 14.52% base-case CAGR.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $19.57 |

| 2027 | $22.41 |

| 2028 | $25.66 |

| 2029 | $27.85 |

| 2030 | $30.59 |

These projections assume SoFi sustains its 30%+ revenue CAGR and 38-42% EPS CAGR. Material upside or downside could come from stablecoin adoption, Galileo client wins, or a credit cycle deterioration.