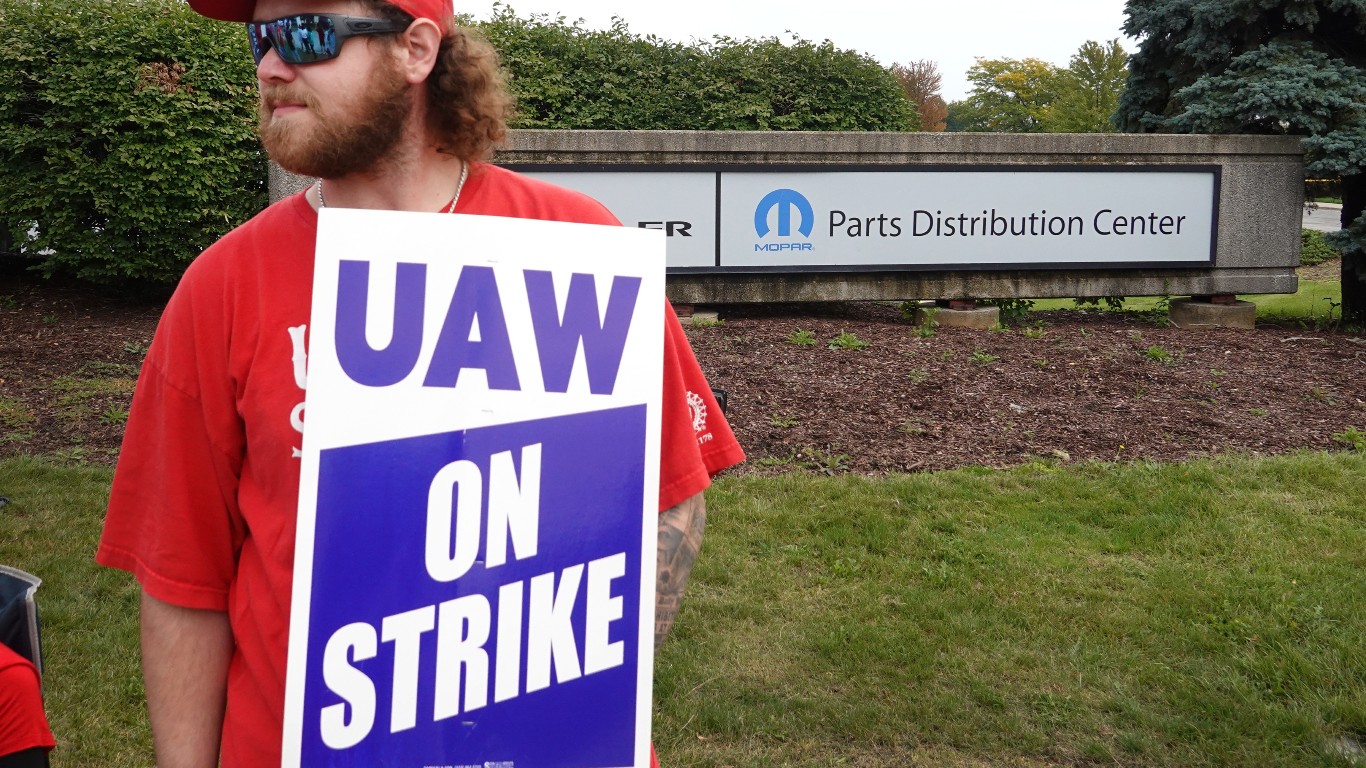

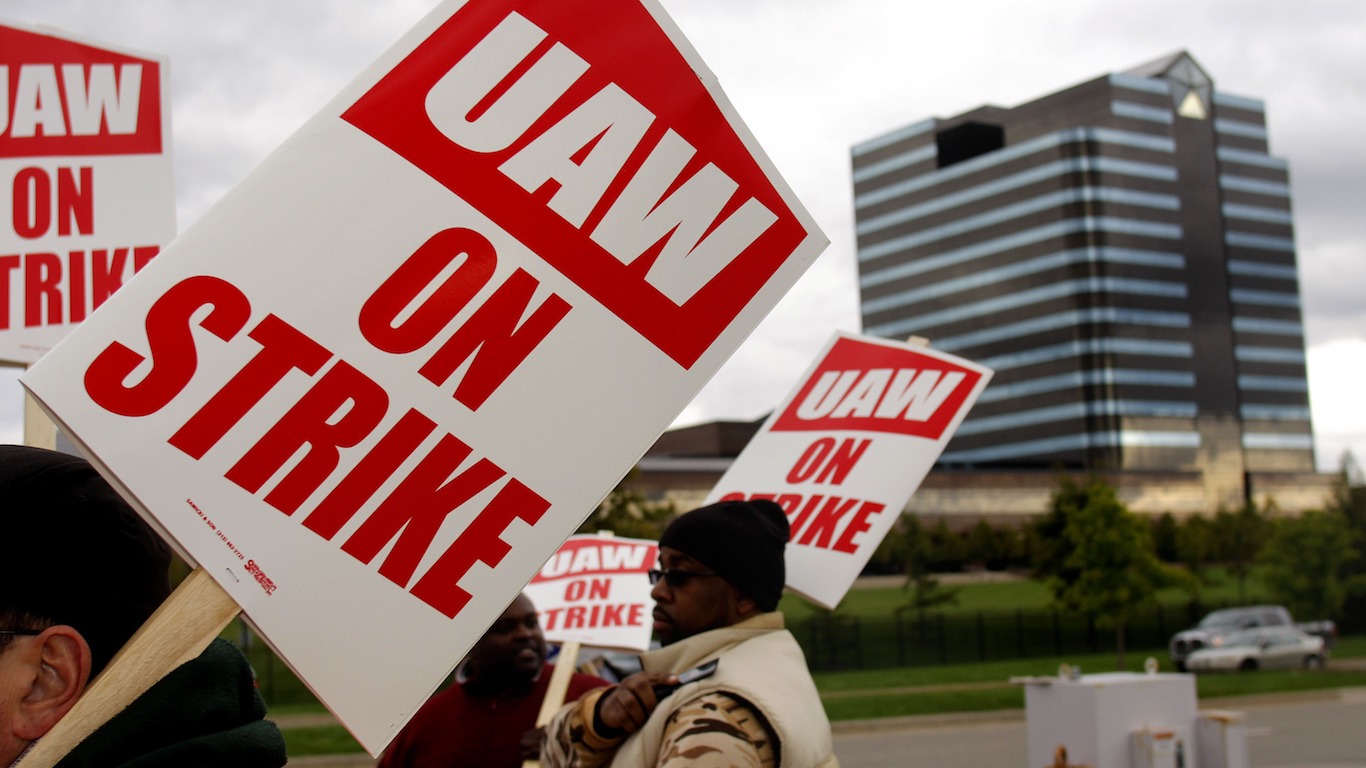

The big news this morning is the autoworkers strike triggered last night at midnight, when the United Autoworkers Union (UAW) could not agree to new contract terms with the “Detroit 3” automakers, Ford F, General Motors GM and Stellantis STLA. The UAW, claiming having been kept behind due to pay structures not keeping pace with inflation for years, are firm in their demand for 36% pay increases over the next four years — the same level of pay increase reportedly received by top executives.

States of Michigan, Ohio and Missouri will be affected by this strike, and a total 8% of membership. President Biden, the most vocally pro-union U.S. president in decades, will speak on this matter later today. Everyone hopes for a quick resolution, though from this vista the two sides still look far apart. And if the writers and actors strike in Hollywood is any indication, workers are feeling confident their demands will be met eventually, even if work stoppages go to protracted lengths.

Empire State manufacturing for September unexpectedly brought us a positive +1.9, up from -10 expected and -19 reported a month ago. This marks only the fourth positive month of 2023 for productivity from the state of New York, and the highest figure we’ve seen since May’s +6.6. Multi-year lows in this metric (ex-Covid months) reached a whopping -32.9 in January of this year. It’s nice to see Empire State data gaining at least a little bit of traction.

Import Prices for August came in hotter than expected — +0.5% versus +0.3% consensus — which is the hottest figure we’ve seen since +2.9% reported back in March of last year. However, strip out volatile petrol (gasoline fuel) costs, and this number comes down to 0.0%, exactly in-line with expectations. Year over year, Import Prices are down -3% (a big improvement from the -6.1% we were seeing in June). Exports month over month grew +1.3%, and year over year came in above expectations to -5.5%. Estimates had been -7%, and the previous month was slightly downwardly revised to -8%.

Pre-market futures have slipped a bit on this news, as they again point to a warmer economy than the Fed would favor, albeit based recently on higher fuel costs, which fluctuate quite a bit month over month. But as odds begin to creep up that the Fed may consider another rate hike next week, or perhaps more likely at their following meeting in November, market participants are treating this as a somewhat bitter pill to swallow. The Dow is +35 points at this hour, the S&P 500 is -3 and the Nasdaq -45. At these levels, however, we’d still close higher for the week.

Ford Motor Company (F): Free Stock Analysis Report

General Motors Company (GM): Free Stock Analysis Report

Invesco QQQ (QQQ): ETF Research Reports

SPDR S&P 500 ETF (SPY): ETF Research Reports

SPDR Dow Jones Industrial Average ETF (DIA): ETF Research Reports

Stellantis N.V. (STLA): Free Stock Analysis Report

To read this article on Zacks.com click here.

This article originally appeared on Zacks