Palantir (NASDAQ:PLTR | PLTR Price Prediction) has been the hottest AI stock on Wall Street, right behind Nvidia (NASDAQ:NVDA). The company has been on a beat-and-raise cadence for a long time, and even some of the bearish voices are second-guessing themselves.

A large number of people remain skeptical and hesitant to touch Palantir. PLTR stock trades at an earnings multiple that hasn’t been seen since the Dot-Com bubble, at least not for a company of this size. It’s why the stock cratered today despite Palantir reporting blockbuster earnings.

All that said, it’s worth looking deeper to see why the bulls are so confident about Palantir. It’s a special company that has embedded itself in several governmental and commercial operations. Palantir has shown that once it gains a toehold in an industry, it can scale exceptionally well, to the point where it can reduce headcount while growing.

Let’s first take a look at the earnings before we take a look at the valuation.

Palantir’s Q3 earnings show a red-hot business

Palantir’s U.S. commercial revenue grew 121% year-over-year, with total revenue growth of 63% YOY. Full-year revenue guidance was also raised to 53% YOY. All of these numbers are above expectations.

Total contract value (TCV) jumped 151% YOY to $2.76 billion, and U.S. commercial TCV surged 342% YOY. Free cash flow guidance was increased to a range of $1.9 billion to $2.1 billion.

Almost every facet of the business is showing upward momentum.

The stock still fell, due to “doubts” about whether or not AI companies were growing fast enough. Palantir may have beaten expectations, but the market expects these AI companies to beat the consensus by wider and wider margins. In short, the market appears to be desensitized to strong earnings reports.

That said, Wall Street won’t punish the stock for too long if Palantir keeps growing at this pace.

Is the market valuing Palantir correctly?

You can use the trusty forward-price to earnings method to value Palantir, in which case you’ll realize that you’re paying 284 times 2025 earnings.

This does sound rather scary, but bullish analysts are actually using free cash flow to evaluate Palantir. Palantir guided for up to $2.1 billion in FCF. Using the upper range makes sense, as Palantir has consistently beaten its own guidance for a while.

Dividing by that cash flow number gets you almost a slightly less scary 218 times 2025 FCF multiple.

Going back to revenue estimates, analysts expect revenue to increase 54% for all of 2025, 35.8% in 2026, and then hold in the 30-40% range through 2030.

Now the Q3 FCF margin was 46%. If Palantir grows that to 50% and meets revenue estimates, that’s $7.81 billion in 2029 FCF. That’s 59 times earnings four years out. If we were to be even more speculative and extrapolate it to 2034, you’re paying 15 times expected FCF (upper range ~$29.5 billion).

Wall Street is unlikely to keep paying over 200 times FCF by then, but 100 times 2034 FCF would put Palantir’s market cap close to $3 trillion by then. This is roughly 663% upside from here, or close to $1,500… Obviously, lots of its and buts are involved.

Where I see PLTR stock going

The above valuations are perhaps as bullish as you can get. Unfortunately, things are unlikely to pan out that way. PLTR stock is well above what you’d consider fair value. And perhaps Palantir’s CEO Alex Karp may be able to humiliate the doubters again, but this will be an uphill battle the bigger the company gets.

The reaction to Q3 is a good barometer for what the market expects: complete perfection. And anything but that can lead to a sharp re-rating of the stock.

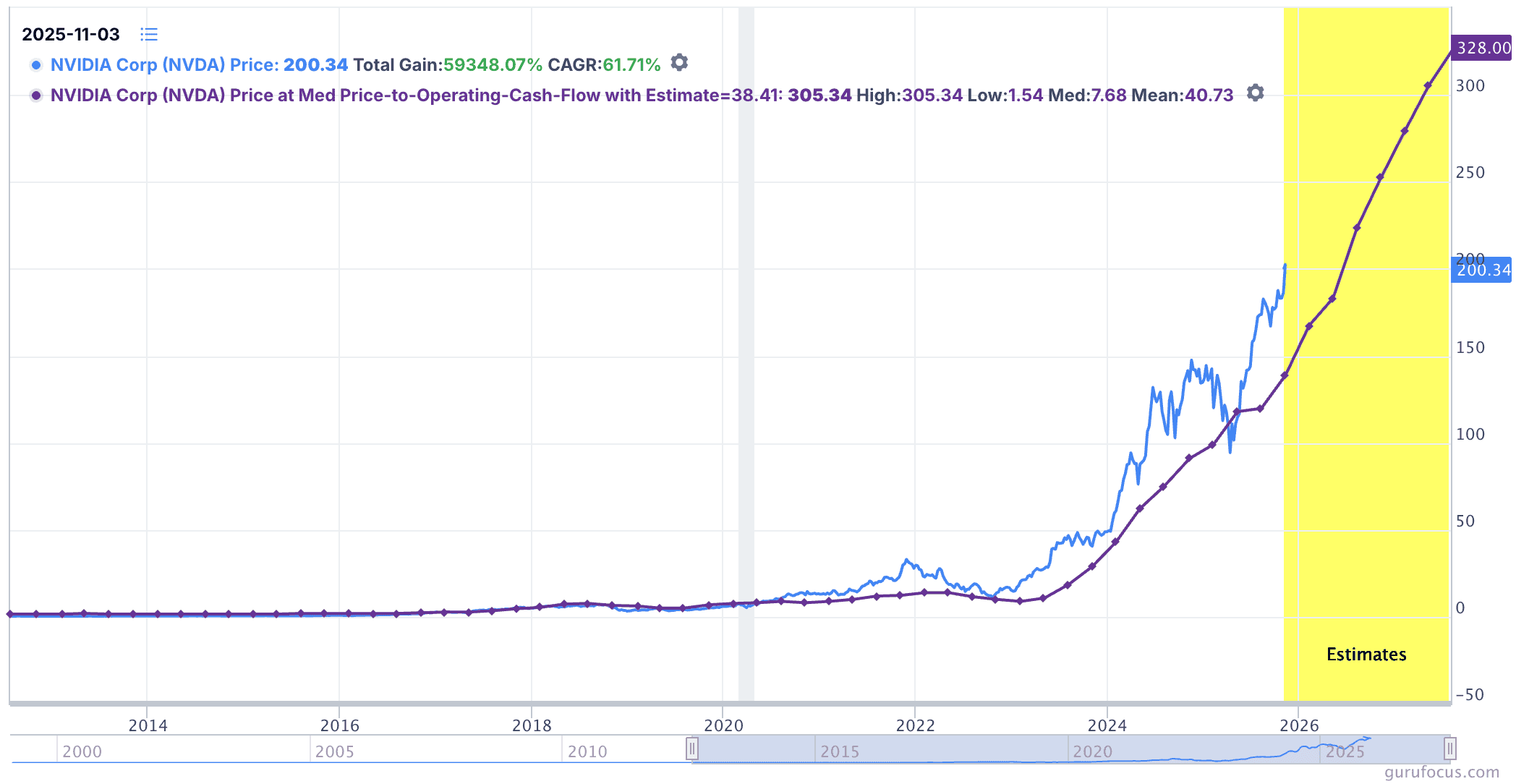

I believe Palantir remains investable as the company is still posting great results, but the easy money has been made. PLTR stock is also ahead of its fundamentals. Let’s take a look at Nvidia, for example.

The above chart shows NVDA’s projected price if it keeps trading at the current operating cash multiple and meets estimates. The rally looks quite organic. NVDA stock is moving in sync with Nvidia’s operating cash flow.

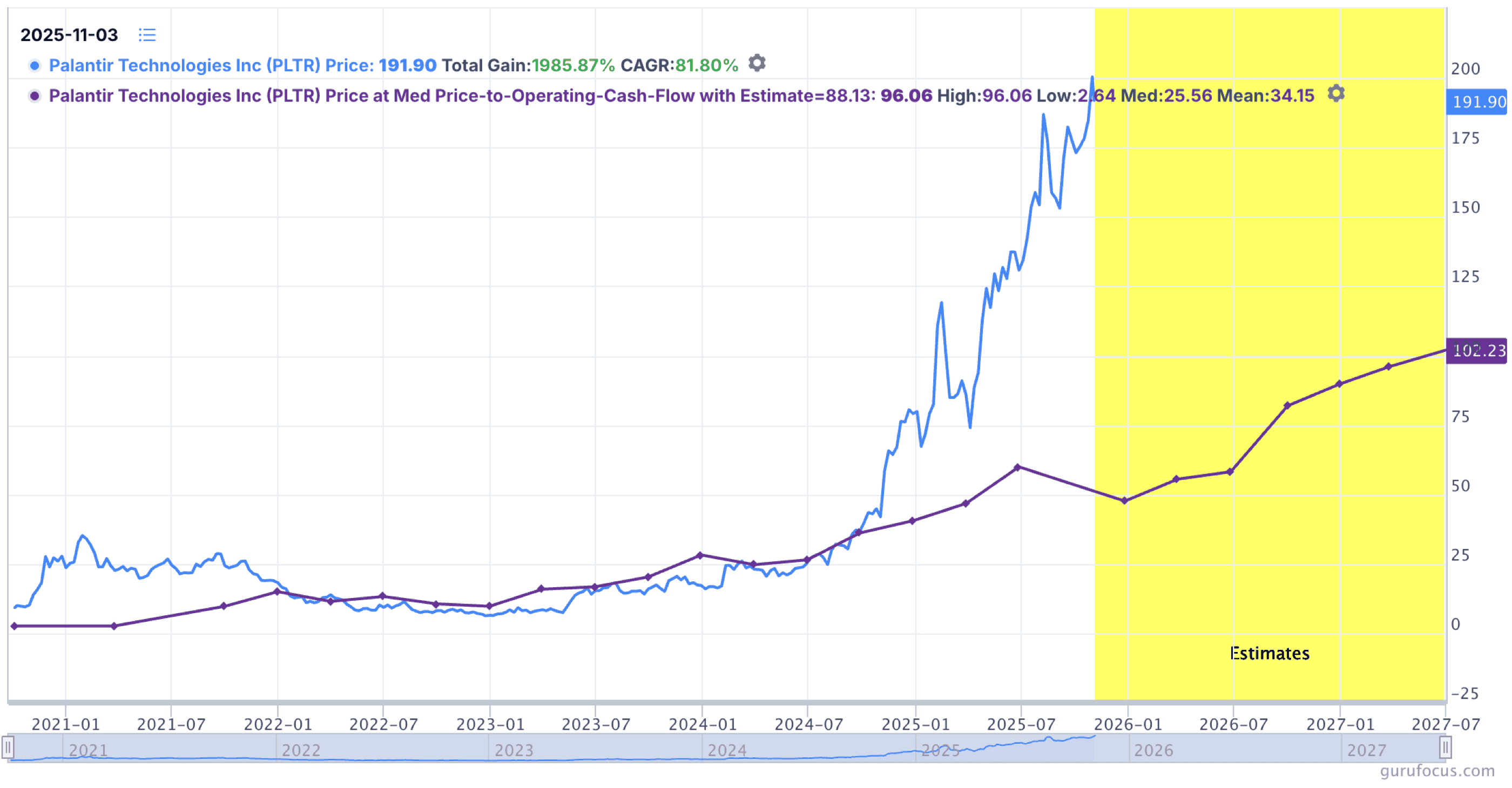

Now let’s look at Palantir.

The market is bidding up every $ of Palantir’s operating cash. No one can say how long it will stay that way. But it’s clearly a far more speculative investment that will end in tears if the market’s sentiment on AI reverses.

Only in the absolute best-case scenario can it surpass even $1,000 within the next decade.