Palantir Technologies (NASDAQ:PLTR | PLTR Price Prediction) stock is down 5% in Tuesday morning trading. There’s no company-specific news driving this move; the selloff appears to be entirely macro-driven.

The NASDAQ 100 fell nearly 1% today. Palantir is moving with the broader market, not against it, which makes the central question for investors a simple one: is this punishment, or just noise?

It’s Just a Market in Fear

When fear spikes, high-multiple growth stocks get hit hardest. Palantir, trading at a premium valuation, is a textbook target in that environment.

The VIX, Wall Street’s primary measure of expected market volatility, has climbed nearly 37% over the past month. That kind of sustained fear elevation doesn’t come from one bad data point. It reflects a market repricing risk across the board, and high-conviction AI names with stretched multiples tend to absorb more of that repricing than the average stock.

The Fundamental Backdrop Hasn’t Changed

Palantir’s most recent earnings report, filed February 2, was a blowout across every major metric. Q4 2025 revenue came in at $1.406 billion, up 70% year over year, beating consensus by 5.74%.

The growth was broad-based across both business lines. U.S. commercial revenue grew 137% year over year to $507 million, while U.S. government revenue grew 66% to $570 million.

Free cash flow for the quarter hit $791 million, a figure that underscores the company is not just growing fast but converting that growth into real cash.

Palantir Technologies CEO Alex Karp framed the quarter with characteristic directness on the earnings call:

“Palantir’s Rule of 40 score is now an incredible 127%. Last quarter, our U.S. revenue grew 93% year-over-year and U.S. commercial revenue grew 137% year-over-year. We are also announcing a 2026 revenue growth guide of 61% year-over-year. We are an n of 1, and these numbers prove it.”

A Rule of 40 score of 127% means that when you add Palantir’s revenue growth rate and profit margin together, you get a number that is more than three times the threshold most software investors consider healthy. In other words, a single day of unfavorable share-price action doesn’t mean Palantir Technologies is in financial trouble.

The Defense Angle Adds Another Layer

Beyond the commercial AI story, Palantir’s government business provides a strategic floor that few pure-play AI companies can claim. The company’s recent Pentagon Maven AI program of record designation reflects how deeply integrated Palantir has become in U.S. defense infrastructure.

To put it another way, Palantir Technologies isn’t just pitching AI to the government and hoping for the best. At this point, Palantir is a company the government already depends on.

For 2026, Palantir guided for total revenue of roughly $7.2 billion, representing roughly 61% year-over-year growth. U.S. commercial revenue alone is guided to exceed $3.1 billion, which would represent at least 115% growth from 2025 levels. Management doesn’t issue guidance like that without conviction in the pipeline.

Where Bulls and Bears Stand Today

The bulls will point to the absence of any company-specific negative catalyst as the clearest possible signal. Palantir has beaten earnings estimates in each of the last four quarters, with the beat margin accelerating sharply through 2025. A macro-driven dip in a stock with that kind of execution track record is the scenario long-term investors typically evaluate most carefully.

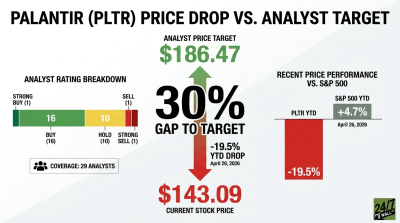

Still, the bears have a legitimate counterpoint. Palantir’s valuation is elevated, and a stock priced for perfection is always more vulnerable to broad market selloffs than a cheap cyclical. PLTR stock was already down roughly 9.5% year to date heading into today’s session, even after a 19% bounce over the past month. High sentiment, high valuation, and a fearful macro backdrop are a combination that can produce more volatility than the fundamentals alone would suggest.

Palantir’s fundamentals haven’t changed. The growth is accelerating, the defense contracts are expanding, and the earnings beat streak is intact. A macro-driven dip in a stock with that execution record is worth understanding, not panicking over.