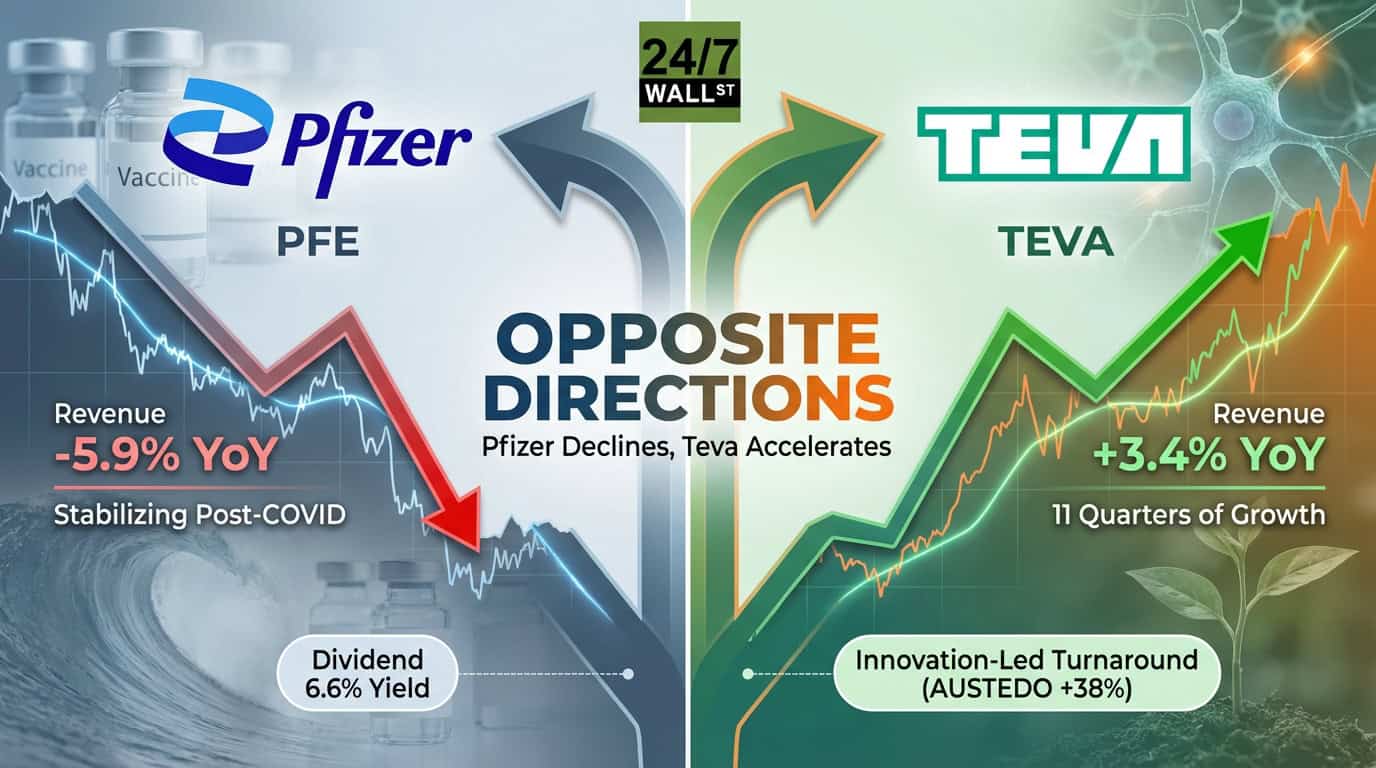

Pfizer (NYSE: PFE | PFE Price Prediction) and Teva Pharmaceutical Industries (NYSE: TEVA) just reported third-quarter earnings that reveal two pharmaceutical companies moving in opposite directions. Pfizer is stabilizing after its COVID revenue collapse while Teva is accelerating through an innovation-led turnaround that has delivered 11 consecutive quarters of growth.

One Declining, One Accelerating

Pfizer posted Q3 revenue of $16.65 billion, down 5.9% year-over-year, as COVID product sales continued declining. Paxlovid dropped 55% operationally and Comirnaty fell 20%. The company beat estimates on revenue and adjusted EPS of $0.87, but the business is still contracting. Non-COVID products grew just 4% operationally, with Eliquis up 22% and Vyndaqel up 7% providing the main lift.

Teva delivered $4.48 billion in revenue, up 3.4% year-over-year, and crushed estimates with adjusted EPS of $0.78 versus consensus of $0.67. AUSTEDO, Teva’s tardive dyskinesia treatment, surged 38% to $618 million. AJOVY climbed 19% to $168 million and UZEDY rose 24% to $43 million. The U.S. segment jumped 12% while Europe declined 2%. CEO Richard Francis pointed to momentum behind the “Pivot to Growth” strategy, shifting Teva from a generics house into a neuroscience and immunology specialist.

| Metric | Pfizer | Teva |

| Revenue Growth YoY | -5.9% | +3.4% |

| EPS Beat | +36% | +16% |

| Main Growth Driver | Non-COVID portfolio (+4%) | Innovative portfolio (+11th quarter) |

| Operating Margin | 35.3% | 28.9% non-GAAP |

Different Paths to Profitability

Pfizer operates at a 35.3% operating margin with massive scale across cardiovascular, oncology, and vaccines. The company generates $4.60 billion in quarterly operating cash flow and pays a 6.6% dividend yield. But it carries $61.71 billion in debt and faces the challenge of replacing $56 billion in annual COVID revenue with organic growth.

Teva is targeting 30% non-GAAP operating margins by 2027, up from 28.9% today. The company just launched a generic liraglutide injection, entering the GLP-1 weight loss market with a lower-cost alternative. Teva terminated exclusive discussions to sell its API business and is restarting that process, which could unlock capital for debt reduction. The company carries $17.09 billion in debt but no dividend, allowing full reinvestment into the turnaround. Operating cash flow of $369 million in Q3 was down 46.8% year-over-year.

Guidance Shows Diverging Confidence

Pfizer reaffirmed full-year revenue guidance of $61.0 to $64.0 billion but raised adjusted EPS guidance to $3.00-$3.15. Management expects significant cost savings by end of 2027.

Teva raised full-year EPS guidance to $2.55-$2.65 non-GAAP and reaffirmed revenue of $16.8-$17.0 billion. Management reaffirmed 2027 AUSTEDO targets even after IRA pricing impacts, signaling confidence in volume growth offsetting price pressure.

Contrasting Investment Profiles

Pfizer offers a 6.6% dividend yield and operates with a massive installed base across multiple therapeutic areas. The company generates $4.60 billion in quarterly operating cash flow but faces the challenge of replacing declining COVID revenue with organic growth from its non-COVID portfolio.

Teva presents a different profile focused on growth rather than income. The company trades at 10x forward earnings with products like AUSTEDO showing 38% growth and new market entries like generic GLP-1. Analyst ratings show 91% Buy ratings for Teva compared to 38% for Pfizer, reflecting different market expectations for the two companies’ trajectories.

Pfizer trades at 8.5x forward earnings despite revenue declines, while Teva trades at 10x forward earnings with 40% earnings growth last quarter. The valuation gap reflects market pricing of Pfizer’s transition challenges versus Teva’s turnaround execution.