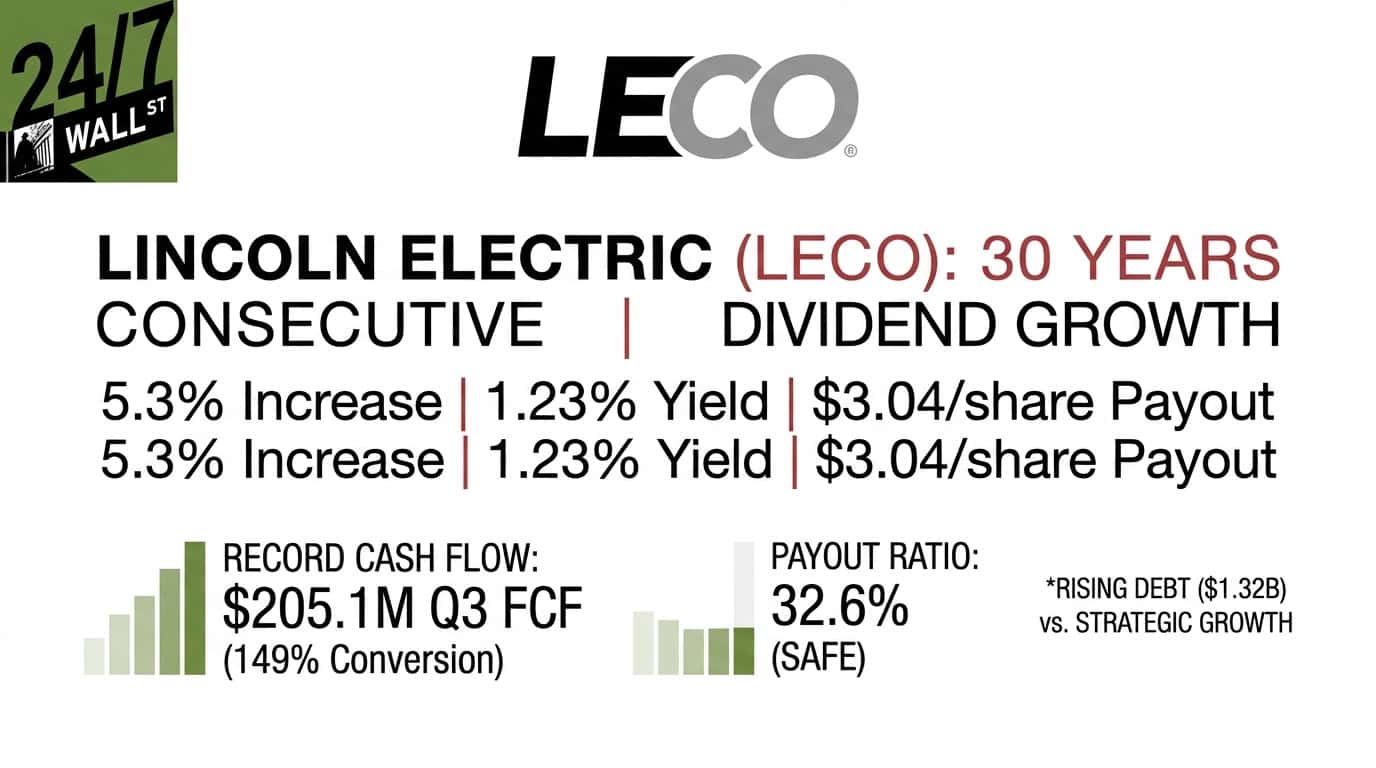

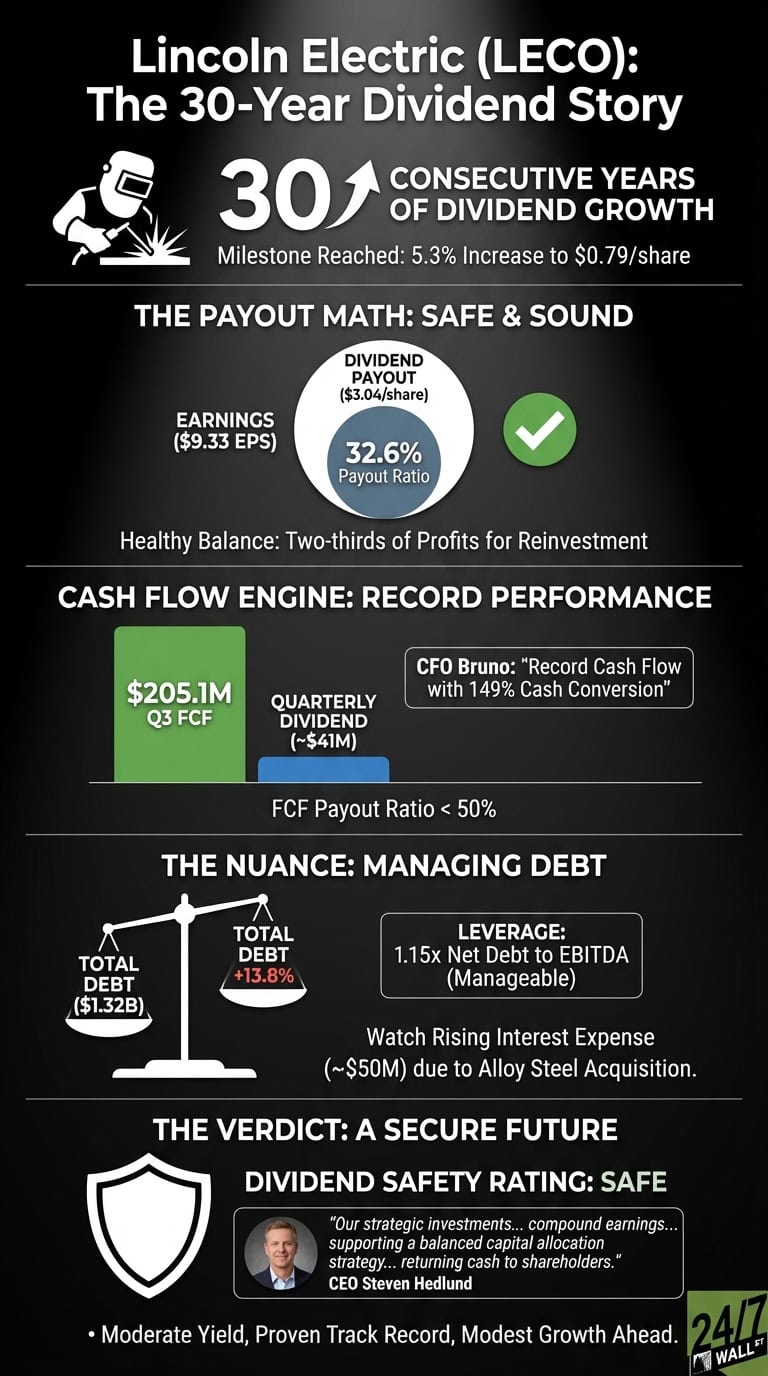

Lincoln Electric Holdings (NASDAQ: LECO | LECO Price Prediction) declared a quarterly dividend of $0.79 per share, a 5.3% increase marking the company’s 30th consecutive year of dividend growth. With a current yield of 1.23% and annual payout of $3.04 per share, can this industrial welding giant sustain its three-decade streak?

| Metric | Value |

|---|---|

| Annual Dividend | $3.04 per share |

| Dividend Yield | 1.23% |

| Consecutive Years of Increases | 30 years |

| Most Recent Increase | 5.3% (October 2025) |

| Dividend Aristocrat Status | Yes (25+ years) |

The Payout Math Works, With Room to Spare

Lincoln Electric’s dividend coverage looks comfortable. With trailing twelve-month diluted EPS of $9.33, the annual dividend of $3.04 translates to an earnings payout ratio of 32.6%, leaving two-thirds of profits for reinvestment or debt reduction.

Cash flow reinforces this strength. In Q3 2025, the company generated $205.1 million in free cash flow (operating cash flow of $236.7 million minus capex of $31.6 million). Against quarterly dividends totaling around $41 million based on 55 million shares outstanding, the FCF payout ratio sits comfortably below 50%. CFO Gabriel Bruno noted the company achieved “record cash flow generation with 149% cash conversion,” providing substantial cushion for dividend payments.

| Metric | Value | Assessment |

|---|---|---|

| Earnings Payout Ratio | 32.6% | Healthy |

| Q3 FCF | $205.1M | Strong |

| Cash Conversion | 149% | Excellent |

| Operating Margin | 17.4% | Solid |

Rising Debt Levels Deserve Attention

The balance sheet presents a more nuanced picture. Total debt increased 13.8% year over year to $1.32 billion, driven by the Alloy Steel acquisition. Net debt stands at $939 million after accounting for $377 million in cash. At 1.15x net debt to EBITDA, leverage remains manageable but has trended upward from 0.91x in 2023.

The debt-to-equity ratio of 0.99 sits near parity, while total liabilities jumped 14.8% year over year. Bruno noted the company is “increasing our interest expense assumption to a low $50 million range due to recent borrowings for the Alloy Steel transaction.” With EBITDA of $813 million, interest coverage appears adequate, though rising debt service will consume cash that could otherwise support dividend growth.

Management Signals Continued Commitment

CEO Steven Hedlund framed the dividend increase within a broader capital allocation strategy: “Our strategic investments and operating model continue to compound earnings […] supporting a balanced capital allocation strategy that invests in long-term growth while returning cash to shareholders through the cycle.”

Bruno was explicit about the milestone: “Looking ahead, we announced our 30th consecutive annual dividend payout rate increase, which is 5.3% starting early next year.” The company returned $94 million to shareholders in Q3 through dividends and $53 million in share repurchases, demonstrating management’s commitment to shareholder returns while funding acquisitions.

This Dividend Remains Safe With Modest Growth Ahead

Dividend Safety Rating: Safe

The combination of a 32.6% earnings payout ratio, strong cash flow generation, and 30 years of consecutive increases supports the view that Lincoln Electric’s dividend is secure. The company’s 38.1% return on equity and expanding margins provide earnings power to sustain the payout through normal business cycles.

Lincoln Electric offers a moderate-yielding industrial with a proven track record, though dividend growth may moderate to mid-single digits as the company balances debt reduction with shareholder returns. Watch for continued leverage increases or automation segment weakness, as cyclical industrial equipment demand could pressure cash flows during a downturn.