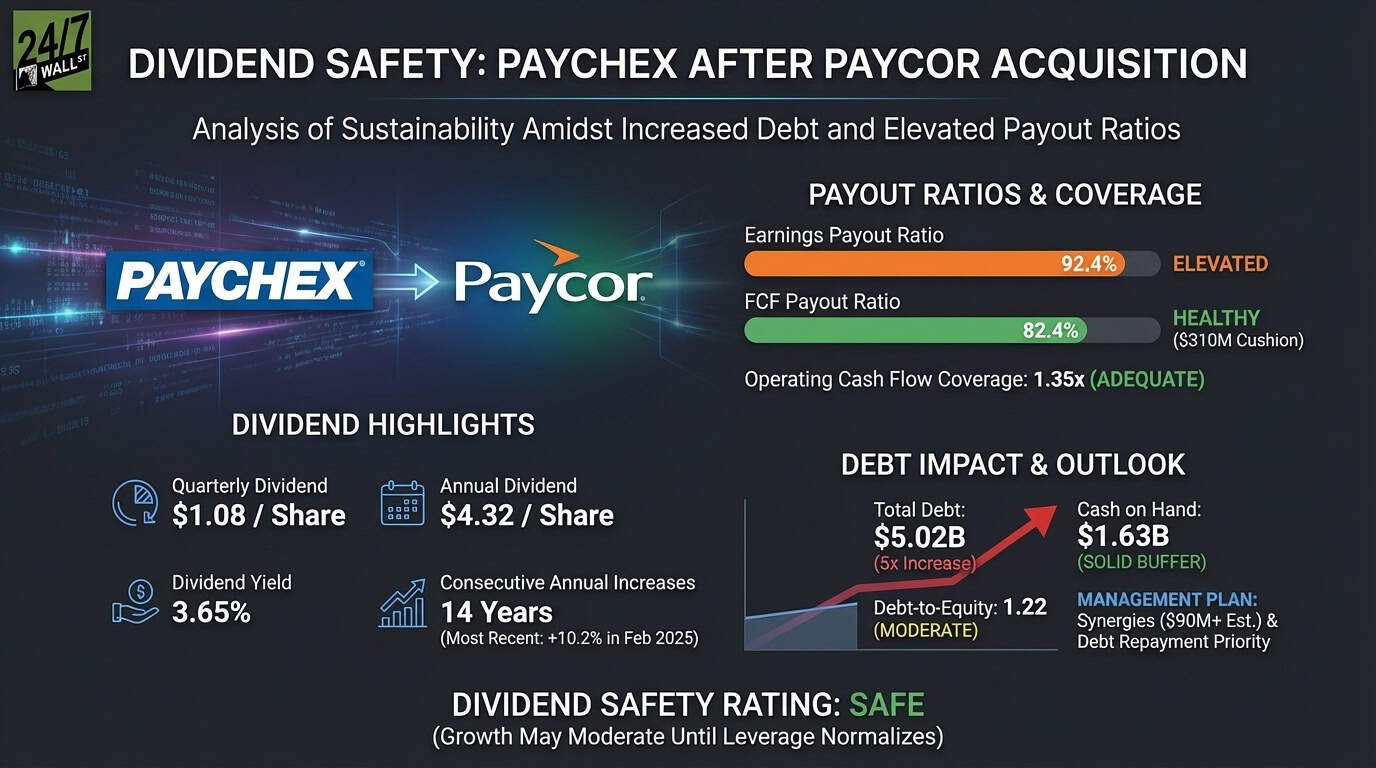

Paychex (Nasdaq: PAYX | PAYX Price Prediction) pays a quarterly dividend of $1.08 per share, yielding 3.65%. The company has raised its dividend for 14 consecutive years, with the most recent 10.2% increase in February 2025. The question for income investors: can Paychex sustain this dividend after taking on $4.2 billion in new debt to acquire Paycor?

| Metric | Value |

|---|---|

| Annual Dividend | $4.32 per share |

| Dividend Yield | 3.65% |

| Consecutive Years of Increases | 14 years |

| Most Recent Increase | 10.2% (Feb 2025) |

| 5-Year Dividend CAGR | 12.4% |

Cash Flow Covers the Dividend Comfortably

Paychex generated $1.95 billion in operating cash flow during fiscal 2025 against capital expenditures of $192 million, producing free cash flow of $1.76 billion. The company paid $1.45 billion in dividends, resulting in a free cash flow payout ratio of 82.4%. That leaves $310 million in cushion.

The earnings payout ratio tells a tighter story. With diluted EPS of $4.46 and dividends of $4.12 per share paid in fiscal 2025, the earnings payout ratio stands at 92.4%. That is elevated, leaving little room for error if earnings decline.

| Metric | FY2025 Value | Assessment |

|---|---|---|

| Earnings Payout Ratio | 92.4% | Elevated |

| FCF Payout Ratio | 82.4% | Healthy |

| Operating Cash Flow Coverage | 1.35x | Adequate |

The FCF payout ratio has crept up from 72.8% in fiscal 2022 to 82.4% today, reflecting both dividend growth and Paycor integration costs. Still, the company generates enough cash to cover the dividend with margin to spare.

Debt Jumped Fivefold, But Management Has a Plan

Paychex carried $866 million in total debt before acquiring Paycor. That figure jumped to $5.02 billion by May 2025. Debt-to-equity surged from 0.23 to 1.22. This is the biggest risk to the dividend.

| Metric | Value | Assessment |

|---|---|---|

| Total Debt | $5.02B | Elevated |

| Debt-to-Equity | 1.22 | Moderate |

| Cash on Hand | $1.63B | Solid Buffer |

CFO Bob Schrader addressed the debt load on the July 2025 earnings call: “We expect to manage leverage effectively […] due to two main factors. First, the additional EBITDA generated from this transaction through synergies. Second […] there is some long-term debt maturing within the next 12 months that we plan to pay down.”

The company expects $90 million in cost synergies from Paycor in fiscal 2026, up from initial estimates. That additional EBITDA will help service debt and protect the dividend. Operating margins of 39.6% remain industry-leading.

Management Prioritizes the Dividend Over Buybacks

Schrader made the capital allocation hierarchy clear: “We believe we are well positioned to maintain our dividend policy […] when we have excess cash, our main method of returning it to shareholders will be through dividends rather than share buybacks.”

Paychex returned $1.5 billion to shareholders in fiscal 2025, split between $1.45 billion in dividends and $160 million in share repurchases. The dividend comes first.

Safe, But Growth May Slow

Dividend Safety Rating: Safe

The free cash flow payout ratio of 82.4% provides adequate coverage, and management has committed to dividend priority. The 14-year growth streak remains intact. However, the elevated earnings payout ratio at 92.4% and the fivefold increase in debt add risk. Paychex should maintain the dividend through the integration period, but future increases may moderate from the recent 10% pace until leverage normalizes. Paychex works for income investors prioritizing stability over aggressive dividend growth, but expect more modest increases until debt normalizes.