When you first think about a Dividend Aristocrat stock, it’s likely not Canadian Natural Resources (NYSE:CNQ | CNQ Price Prediction). People usually assume Dividend Aristocrats are slow-growing cash cows that will keep you ahead of inflation with dividends, and perhaps a bit more on top of that. Very rarely do you assume a Dividend Aristocrat would have the bearings to outperform even the Nasdaq-100 over the past 25 years.

That’s a perfect sign that you’re underestimating the power of compounding. These dividend stocks look boring on the surface, but their snowballing dividends can make you outperform even growth stocks in the long run.

Let’s take a look at what made it possible with CNQ and whether or not you can expect similar returns in the next 25 years with this stock.

Canadian Natural Resources’ dividend strategy

Canadian Natural Resources is one of the world’s largest independent crude oil and natural gas producers. It operates across the entire oil and gas value chain, from exploration to marketing. The company also owns midstream infrastructure.

The magic behind its outperformance over the long run is the rising dividend and the company’s ability to capitalize whenever there’s an increase in oil and gas prices.

CNQ stock is up over 180% in the past five years and still comes with a forward dividend yield of nearly 5%. It has been raising its dividends for 25 years straight and has returned over CAD 6 billion in the first nine months of 2025.

What’s even more impressive is that the 5-year dividend growth rate is at 22.37% annually. The forward payout ratio is still 64%. If there’s ever trouble in the oil and gas markets, there’s ample breathing room.

CNQ raised dividends through 2020 (when oil prices briefly dipped into the negatives). It also kept paying dividends through the 2014 oil price collapse.

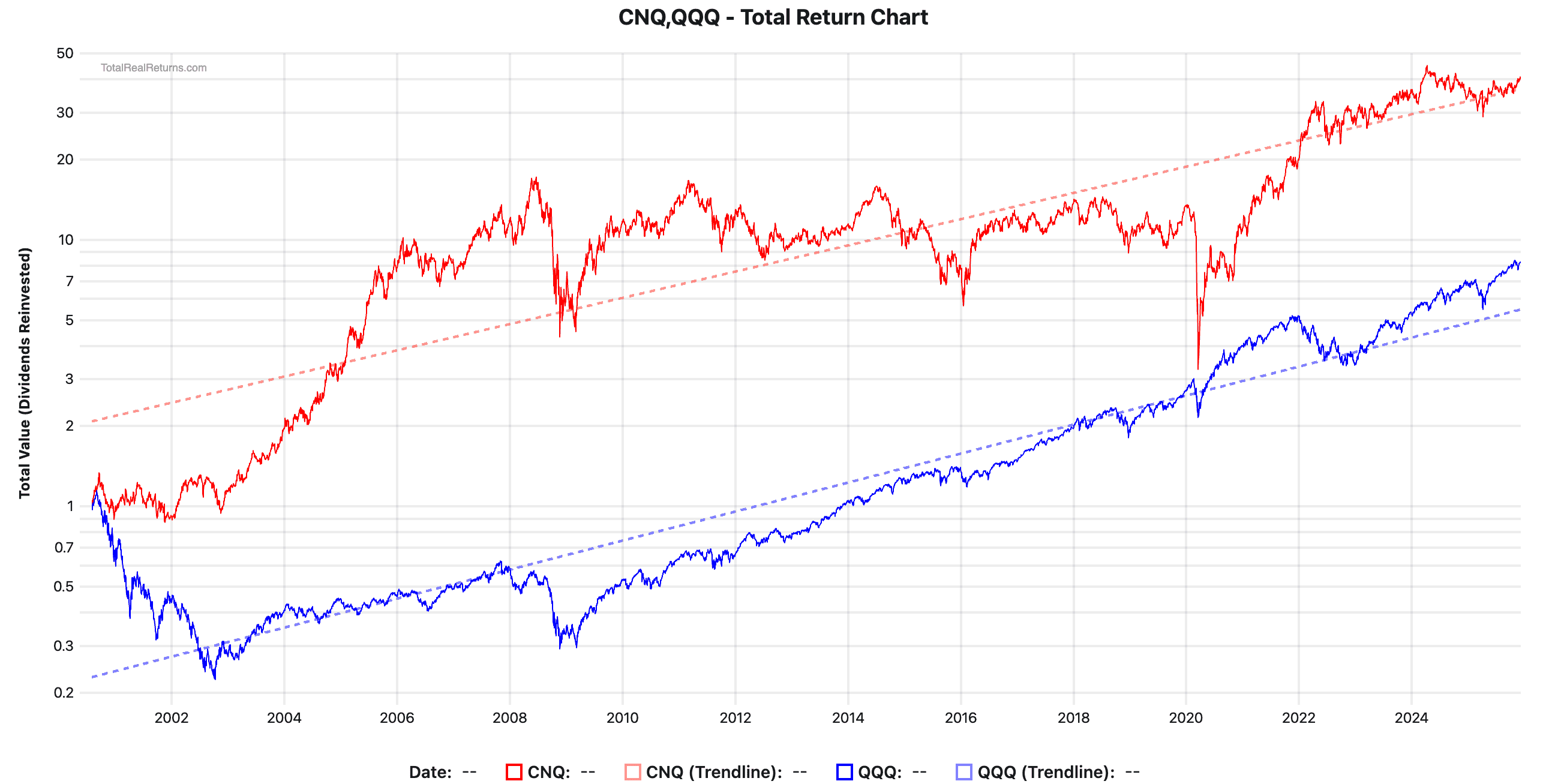

The numbers behind its “snowballing returns” from 2000 to 2025

If you invested $100k in mid-2000 and kept reinvesting dividends, your overall return would be 3,925.28%. This means your original investment would top $4 million today. If you put the same amount of money into the Invesco QQQ Trust (NASDAQ:QQQ) and reinvested the meager dividends, you’d end up with $823,680 today.

The Dot Com bubble slowed down the QQQ significantly, whereas the 2014-2016 oil slowdown also caused CNQ stock to underperform for a long stretch.

Regardless, long-term investors still made progress as they reinvested dividends, and the company eventually made a recovery in earnest.

Can it repeat its magic again?

CNQ stock is unlikely to hand you another 40x in the next 25 years, but it is still worth owning since it comes with great yields and still has upside potential.

The company’s performance in the past 25 years was due to oil prices rising significantly in the early 2000s, which coincided with the company building out massive oil sands mining and thermal operations, transitioning from higher-decline conventional assets to 57% long-life, low-decline production with only an 11% corporate decline rate. This gave it a large early head start.

Average crude oil prices jumped from $19.69 in 1999 to $98.69 in 2008. So far in 2025, it is much lower at $64.39. If you adjust for inflation, crude oil prices are actually lower today than they were in late 2000.

This shows the company can keep expanding and paying dividends even if the broader energy market is flat or trending downwards.

Why I’d buy CNQ stock hand over fist today

The demand for oil and gas should remain strong, at least for a North American company like Canadian Natural Resources. There is an ongoing push towards re-industrialization and onshoring. Plus, the drive towards renewable energy has been nowhere near as aggressive as previously thought. Countries are relying heavily on oil and gas, even more so than before.

Sanctions on certain countries after 2022 make it even more likely that CNQ stock is well-positioned to deliver. European countries have turned to North America for their energy needs. Both the U.S. and Canada are seeing an oil and gas export boom to Europe, with analysts saying Canada’s current Prime Minister’s aim is “…to author a sequel to the oil boom that Canada experienced between the start of the century and 2014. He’s never put it so plainly, but it’s clearly the target.”

In short, CNQ can keep growing in the coming decades and keep outperforming most other dividend stocks. Analysts expect EPS to double from 2025 to 2029.