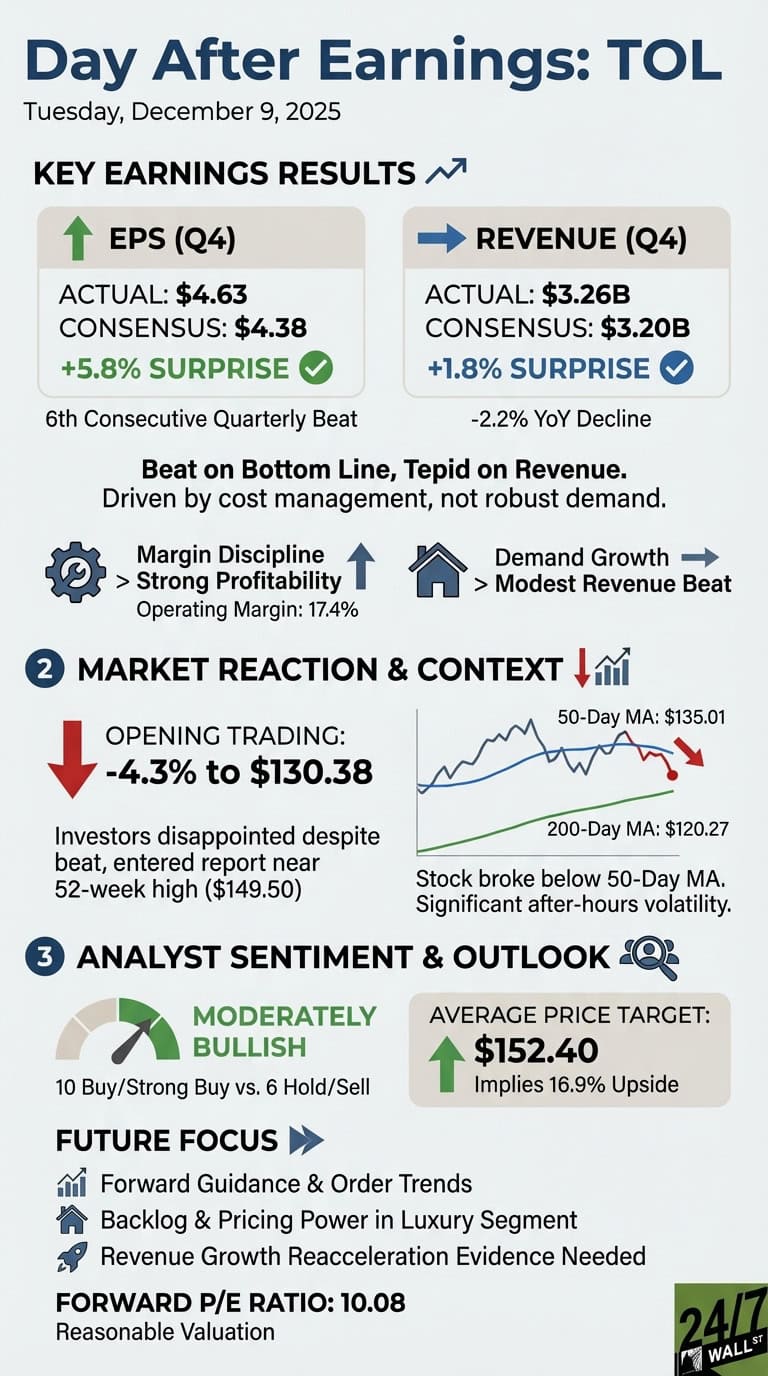

Yesterday we were watching whether Toll Brothers could deliver another earnings beat amid a challenging housing market. The luxury homebuilder reported fourth-quarter results before Monday’s open, posting EPS of $4.63 versus the $4.38 consensus estimate. This morning, shares opened in the pre-market down approximately 4.3% to $130.38, suggesting investors found something to dislike despite the headline beat.

Beat on Bottom Line, Tepid on Revenue

The $0.25 per share earnings beat represented a 5.8% surprise, marking the sixth consecutive quarter Toll Brothers has exceeded analyst expectations. However, revenue of $3.26 billion came in just 1.8% above the $3.20 billion estimate. More concerning for investors: that revenue figure declined 2.2% year over year from the prior fourth quarter’s $3.33 billion.

This pattern suggests the earnings outperformance came more from cost management and margin discipline than from robust demand growth. The company maintained strong profitability metrics, with operating margins at 17.4% on a trailing basis, but the modest revenue beat against elevated expectations appears to have disappointed the market.

Context matters here. Toll Brothers entered the report trading near its 52-week high of $149.50, meaning strong results were already priced in. The stock needed more than a modest beat to justify its premium valuation.

Market Reaction Reflects Growth Concerns

Pre-market trading volume remained light, with shares drifting lower in early activity. The stock broke below its 50-day moving average of $135.01, though it still holds above the 200-day moving average of $120.27. After-hours trading Monday evening showed significant volatility, with a spike to 212,990 shares at 7:00 PM and wide price swings between $129.22 and $136.47.

Despite the negative reaction, analyst sentiment remains moderately bullish. Ten analysts maintain Buy or Strong Buy ratings versus six Hold or Sell ratings, with an average price target of $152.40. That implies 16.9% upside from current pre-market levels, suggesting the sell-side views this pullback as temporary.

Focus Shifts to Guidance and Demand Trends

The key question now centers on forward guidance and order trends, neither of which appear in the preliminary data. With a forward P/E ratio of just 10.08, the stock trades at a reasonable multiple for a profitable homebuilder. However, investors need evidence that revenue growth can reaccelerate to justify even that modest valuation.

We’ll be watching how the stock trades through the morning session and whether management commentary on the earnings call provides clarity on backlog trends and pricing power in the luxury segment. Any analyst target adjustments should emerge within 24 to 48 hours.