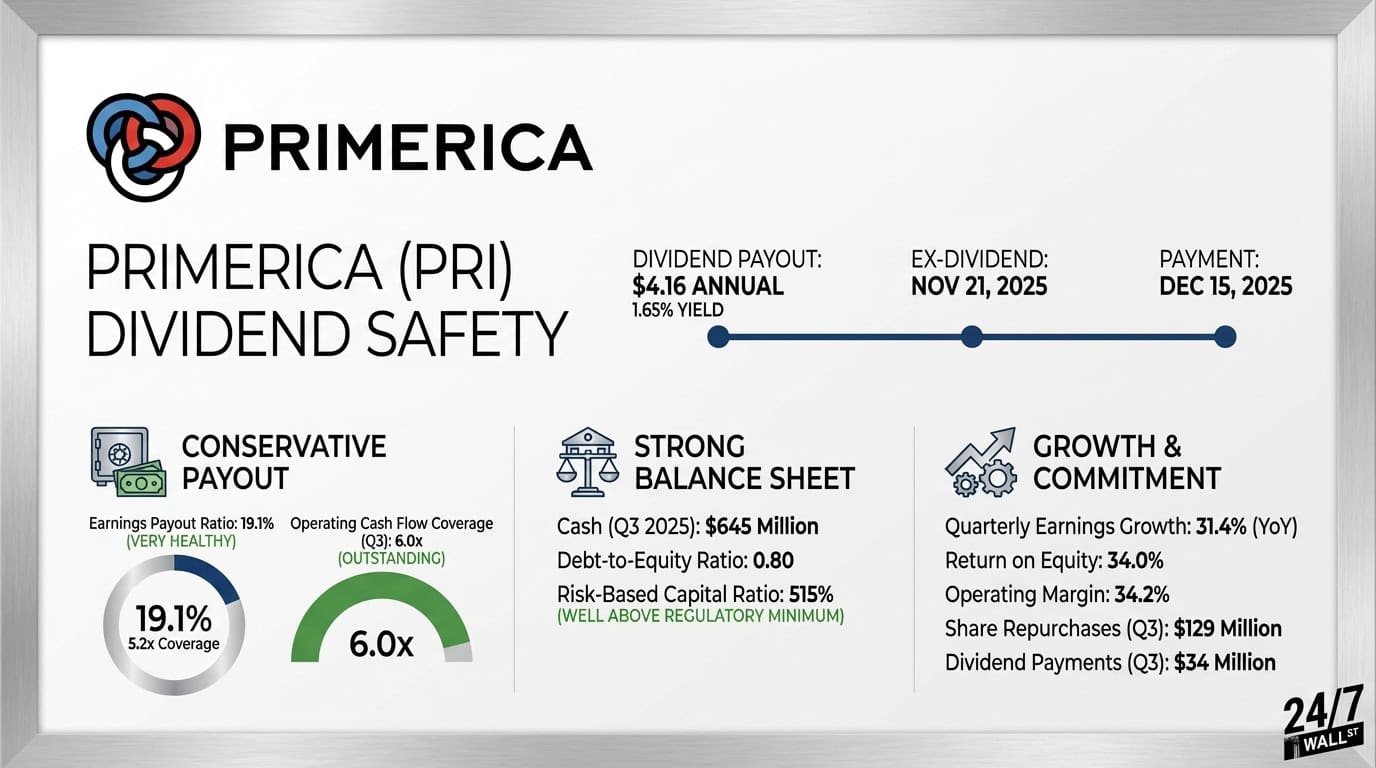

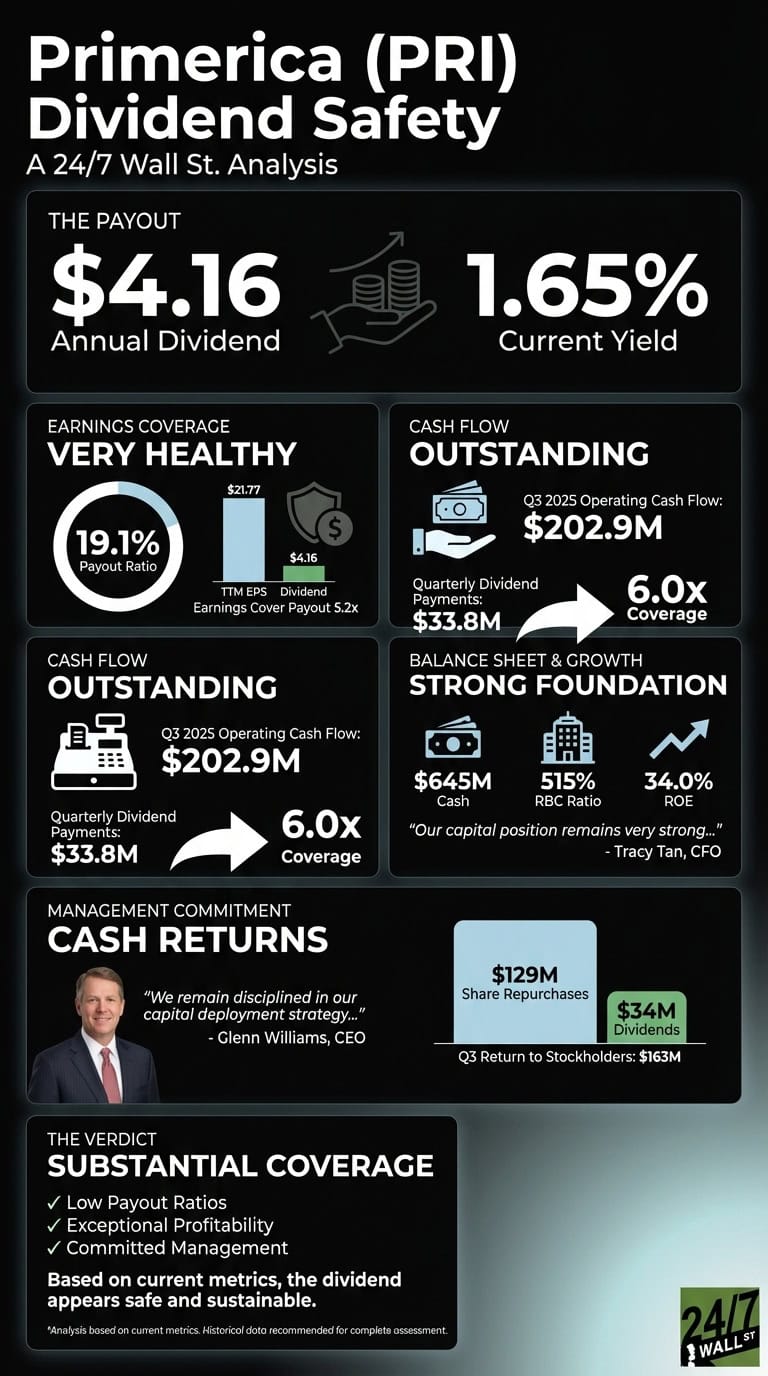

Primerica (NYSE: PRI | PRI Price Prediction) pays a $4.16 annual dividend with a 1.65% yield. Based on current financial metrics, we examine whether this financial services provider can sustain this payout.

| Metric | Value |

|---|---|

| Annual Dividend | $4.16 per share |

| Dividend Yield | 1.65% |

| Ex-Dividend Date | November 21, 2025 |

| Payment Date | December 15, 2025 |

Current Coverage Metrics Show Conservative Payout

Primerica’s current payout ratios are remarkably conservative. The company earned $21.77 per share over the trailing twelve months while paying $4.16 in dividends, producing an earnings payout ratio of just 19.1%. Current earnings cover the payout 5.2 times over.

The free cash flow picture is even stronger. In Q3 2025, Primerica generated $202.9 million in operating cash flow and spent only $12.3 million on capital expenditures, leaving $190.6 million in free cash flow for the quarter. Against quarterly dividend payments of $33.8 million, operating cash flow coverage stands at 6.0 times.

| Metric | Value | Assessment |

|---|---|---|

| Earnings Payout Ratio | 19.1% | Very Healthy |

| Operating Cash Flow Coverage (Q3) | 6.0x | Outstanding |

Balance Sheet Supports Growth

Primerica ended Q3 2025 with $645 million in cash and a debt-to-equity ratio of 0.80. The company’s insurance subsidiary maintains a risk-based capital ratio of 515%, well above the 200% regulatory minimum.

CFO Tracy Tan addressed capital strength on the Q3 earnings call: “Our capital position remains very strong […] we do have plans to increase that conversion from our insurance entities.”

The company’s return on equity of 34.0% and operating margin of 34.2% demonstrate efficient capital deployment. With a profit margin of 21.6%, Primerica converts revenue to cash effectively.

Strong Recent Performance

Primerica has demonstrated strong operational momentum. Quarterly revenue grew 8.1% year-over-year to $839.8 million in Q3 2025, while quarterly earnings surged 31.4% year-over-year to $206.8 million.

Management Commits to Returns

CEO Glenn Williams stated in the Q3 call: “We remain disciplined in our capital deployment strategy and returned a total of $163 million to stockholders through a combination of $129 million in share repurchases and $34 million in regular dividends during the quarter.”

Tan added: “We’re confident about our ability to generate cash and our ability to return a good amount of cash back to the stockholders in various ways.”

Current Dividend Coverage Assessment

Based on current metrics, the 19.1% earnings payout ratio provides substantial coverage. The company’s exceptional profitability metrics, with a 34.0% return on equity and 34.2% operating margin, support the current dividend level. Strong quarterly cash flow generation of $202.9 million against dividend payments of $33.8 million demonstrates solid current coverage. The company has demonstrated commitment to shareholder returns through both dividends and share repurchases, though the current yield of 1.65% remains modest.