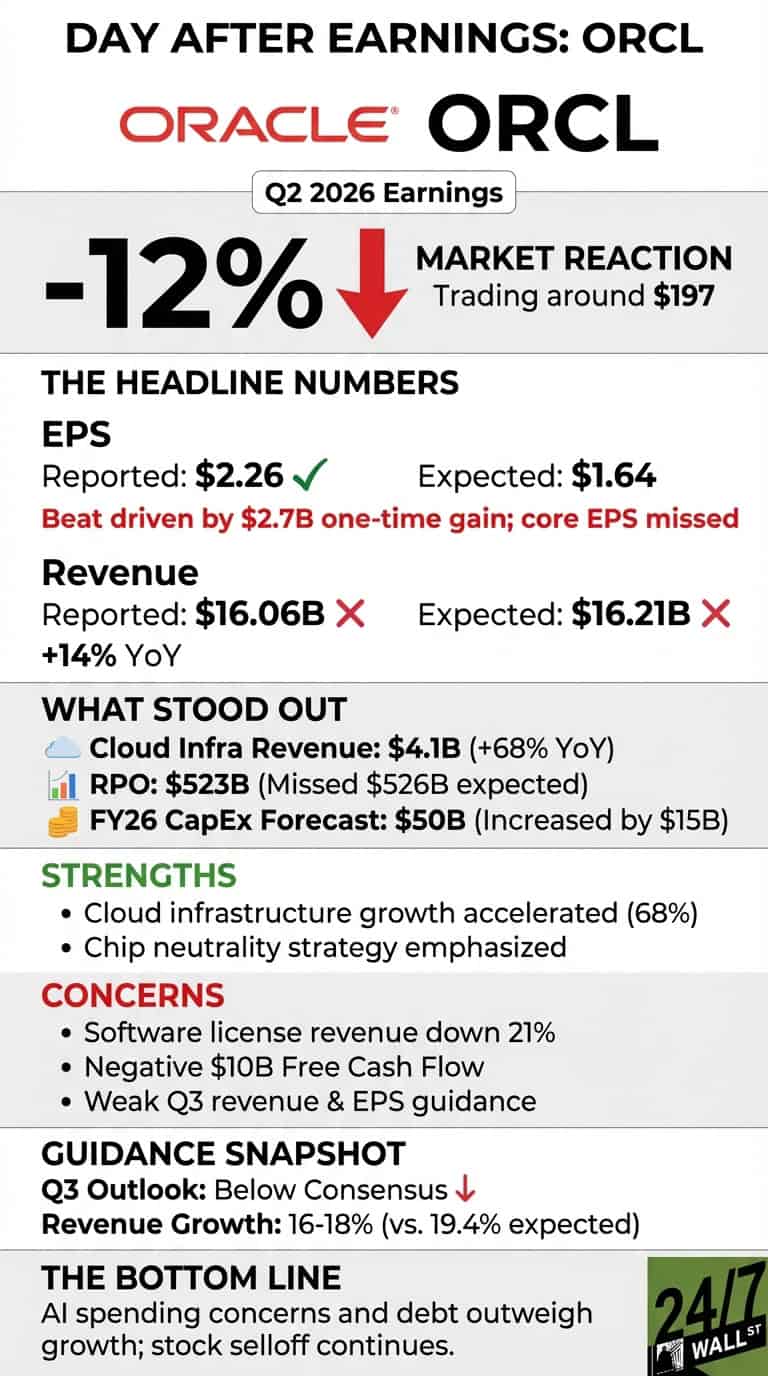

Yesterday we highlighted Oracle’s massive $455 billion cloud backlog and the question of whether infrastructure spending would finally convert to sustainable margin expansion. This morning, investors are answering decisively. Shares plunged 12% to around $197 in Thursday trading after the company reported a 38.6% earnings beat that came with a $2.7 billion one-time gain, weak guidance, and a stunning $15 billion increase to capital expenditure forecasts.

The Beat That Wasn’t

Oracle posted adjusted EPS of $2.26 versus the $1.64 estimate, but the headline number obscures the reality. The company booked a $2.7 billion pretax gain from selling its Ampere chip unit to SoftBank. Stripping that out, core earnings would have landed near $1.33, well below expectations. Revenue of $16.06 billion missed the $16.21 billion estimate despite 14% year-over-year growth. Software license revenue dropped 21%, and total software revenue fell 3% to $5.88 billion, missing the $6.06 billion consensus.

Cloud infrastructure revenue grew 68% to $4.1 billion, accelerating from 55% last quarter. Remaining performance obligations hit $523 billion, up from $455 billion in September but still below the $526 billion Wall Street expected. The real shock came when Principal Financial Officer Doug Kehring announced that fiscal 2026 capital expenditures would reach $50 billion, $15 billion higher than the September guidance of $35 billion. Free cash flow was negative $10 billion in the quarter, marking three consecutive quarters of cash burn.

Management Optimism Meets Market Reality

Co-CEO Clay Magouyrk tried to calm concerns about financing the data center buildout, noting Oracle is exploring models where customers bring their own chips or vendors rent capacity rather than sell it outright. Chairman Larry Ellison emphasized the company’s shift to “chip neutrality,” saying Oracle will deploy “whatever chips our customers want to buy” rather than manufacturing its own. The message: flexibility will ease capital intensity.

Investors weren’t convinced. The company’s third-quarter revenue growth guidance of 16% to 18% missed estimates of 19.4% growth to $16.87 billion. Adjusted EPS guidance of $1.64 to $1.68 came in below the $1.72 consensus. At least 12 brokerages cut price targets following the report, with Stifel dropping its target from $350 to $275 and Evercore lowering from $385 to $275.

What Comes Next

As we noted in our live coverage yesterday, the core question was whether Oracle’s AI infrastructure spending would translate to profitability. This report suggests the answer is “not yet.” The stock now trades at a forward P/E of 29.6x, down from over 50x trailing but still elevated compared to Microsoft at 27.2x and Amazon at 29.1x. Analysts are calling this a “question of patience,” but with five-year credit default swaps hitting record highs and debt concerns mounting, investors appear unwilling to wait. We’ll be watching whether the selloff stabilizes or if concerns about the AI spending cycle spread to other infrastructure plays.