Precious metals are normally sleepy, low return investments. Usually the case for owning them is some version of an inflation hedge or building out additional portfolio allocations. But, with a 62% gain in 2025, the SPDR Gold Trust has quietly delivered one of the year’s best investment performances. The question is whether the rally has room to run or if momentum is exhausted. That answer lies in two forces: the macro tide lifting gold broadly, and the micro mechanics of how GLD operates.

The Central Bank Bid and What It Signals

Gold’s 2025 rally isn’t driven by retail sentiment or inflation panic. It’s structural. Central banks purchased 53 tonnes of gold in October 2025, bringing year-to-date reported buying to 254 tonnes, according to the World Gold Council. Poland added 16 tonnes in October after pausing since May, lifting its reserves to 531 tonnes. Brazil bought for the second consecutive month. These aren’t opportunistic trades. They’re strategic reserve shifts.

Watch the World Gold Council’s monthly central bank statistics, published around the first week of each month. A slowdown in emerging market purchases, particularly from Poland, Kazakhstan, or Turkey, would signal waning institutional confidence. Any acceleration, or new entrants like Serbia (which recently announced plans to double reserves to 100 tonnes by 2030), would reinforce the structural bid.

And then there is the Federal Reserve forward guidance. Gold surged to record highs above $4,300 per ounce after the Fed’s final 2025 rate cut in December. Goldman Sachs now forecasts gold at $4,900 per ounce by the end of 2026, citing persistent central bank demand and macroeconomic uncertainty.

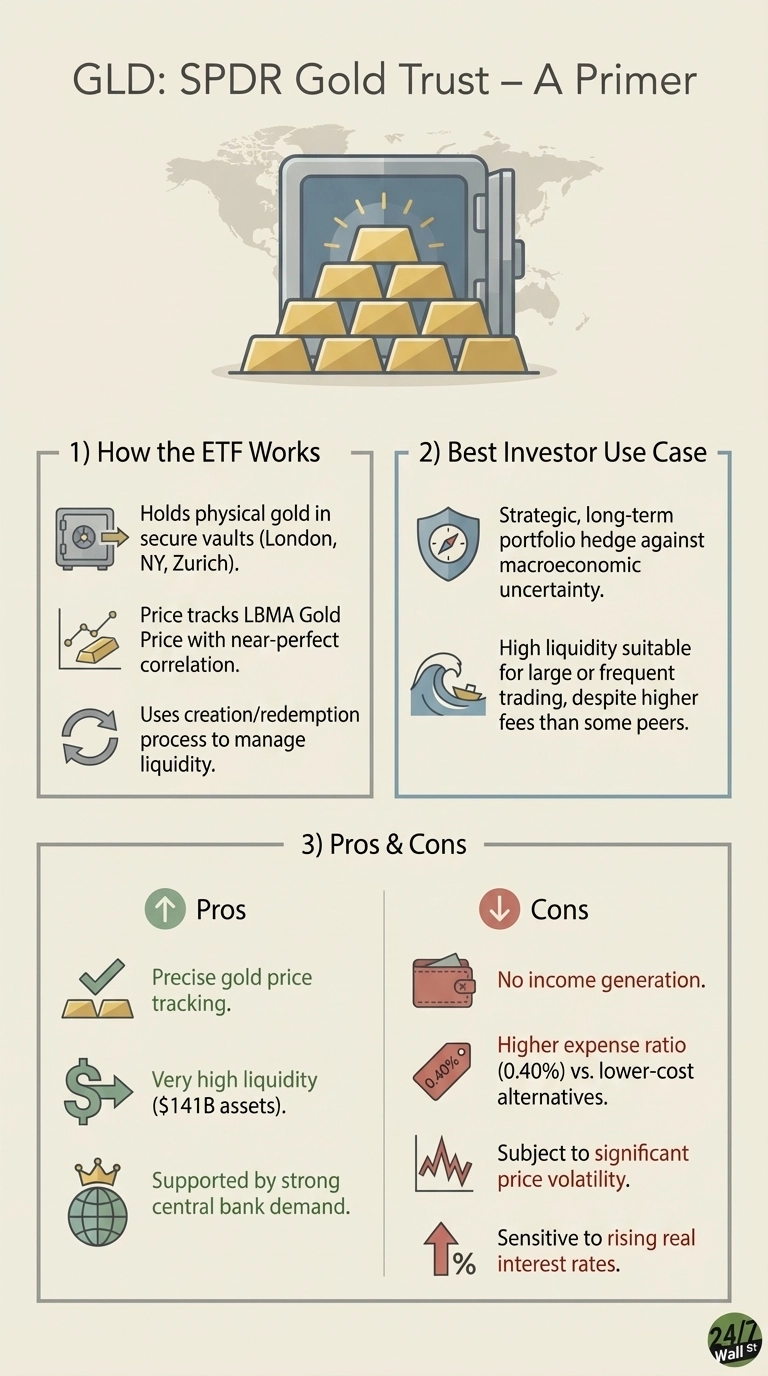

A Lower-Cost Alternative Worth Considering

IAU, the iShares Gold Trust, offers the same physical gold exposure with a 0.25% expense ratio versus GLD’s 0.40%. Over five years, IAU has delivered a 10.48% annualized return compared to GLD’s 10.30%, purely due to lower fees. On a $50,000 investment held for five years, you’d save $375 in fees with IAU. The trade-off is liquidity. GLD’s $141 billion in assets dwarfs IAU’s $32 billion, making GLD better for large or frequent trades. But for buy-and-hold investors, IAU’s cost advantage is material.

The most important macro factor driving GLD for the next 12 months is whether central bank buying sustains above 50 tonnes monthly.