Erie Indemnity (NASDAQ:ERIE | ERIE Price Prediction) operates as the management company for Erie Insurance Exchange, one of the nation’s largest property and casualty insurers. The company just raised its dividend 7.1% despite the stock falling nearly 30% in 2025. Can Erie Indemnity afford to keep paying shareholders? I think so, and here’s why:

| Metric | Value |

|---|---|

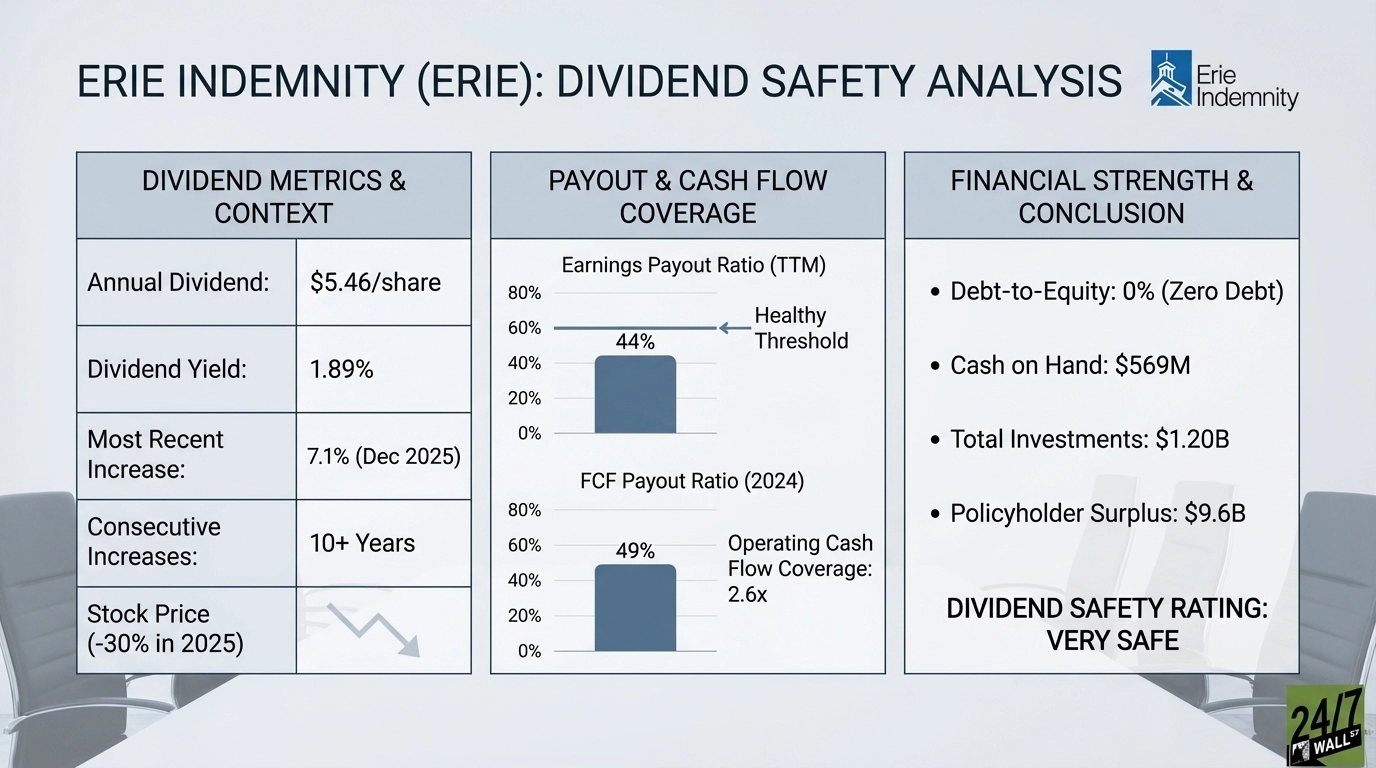

| Annual Dividend | $5.46 per share |

| Dividend Yield | 1.89% |

| Consecutive Years of Increases | 10+ years |

| Most Recent Increase | 7.1% (December 2025) |

| 5-Year Dividend CAGR | 7.1% |

The dividend stands at $1.4625 per quarter, payable January 21, 2026.

The Payout Ratios Look Comfortable

Erie Indemnity paid $5.46 per share in dividends over the trailing twelve months against earnings of $12.39 per share. That’s a 44% earnings payout ratio, well below the 60% threshold I consider healthy. In Q3, the company paid $63.6 million in dividends against net income of $183 million, a 35% payout ratio.

| Metric | TTM Value | Assessment |

|---|---|---|

| Earnings Payout Ratio | 44% | Healthy |

| FCF Payout Ratio (2024) | 49% | Healthy |

| Operating Cash Flow Coverage | 2.6x (2024) | Strong |

The free cash flow picture is equally solid. In 2024, Erie generated $611.3 million in operating cash flow and spent $124.8 million on capex, leaving $486.4 million in free cash flow. Against $237.5 million in dividends paid, that’s a 49% FCF payout ratio. Operating cash flow covered dividends 2.6 times.

The cash flow payout ratio improved from 80% in 2020 to 39% in 2024. The business generates more cash relative to its dividend obligation.

Zero Debt and a Fortress Balance Sheet

Erie Indemnity carries no debt. The company has $569 million in cash and $1.20 billion in total investments against $2.31 billion in shareholder equity. With no interest expense, every dollar of operating cash flow is available for dividends, reinvestment, or building reserves.

| Metric | Value | Assessment |

|---|---|---|

| Debt-to-Equity | 0% | Exceptional |

| Cash on Hand | $569M | Strong Buffer |

| Total Investments | $1.20B | Ample Liquidity |

| Policyholder Surplus | $9.6B | Very Strong |

The Erie Insurance Exchange maintains $9.6 billion in policyholder surplus, up $300 million in 2025.

Management Remains Committed Despite Challenges

In December 2025, the Board announced it would “maintain the management fee rate charged to Erie Insurance Exchange at 25% for 2026” and approved a “7.1% increase in the regular quarterly cash dividend.” The board stated “this decision reflects an ongoing commitment to shareholder returns and consideration of the financial standing of both entities.”

That 25% management fee is Erie Indemnity’s primary revenue source. The board’s decision to maintain it for 2026 provides revenue stability.

The Exchange faced headwinds with its combined ratio hitting 100.6% in Q3, though that improved from 113.7% a year earlier. Management implemented rate increases and launched ErieSecure Auto in Ohio in August 2025 with expansion to Pennsylvania, West Virginia, and Virginia in December.

This Dividend Is Very Safe

Dividend Safety Rating: Very Safe

Erie Indemnity pays out 44% of earnings and 49% of free cash flow, carries zero debt, and sits on over half a billion in cash. The 7.1% dividend increase in December demonstrates management’s confidence despite a difficult year for the stock.

The dividend looks rock solid, though watch for deterioration in the combined ratio or challenges to the 25% management fee.