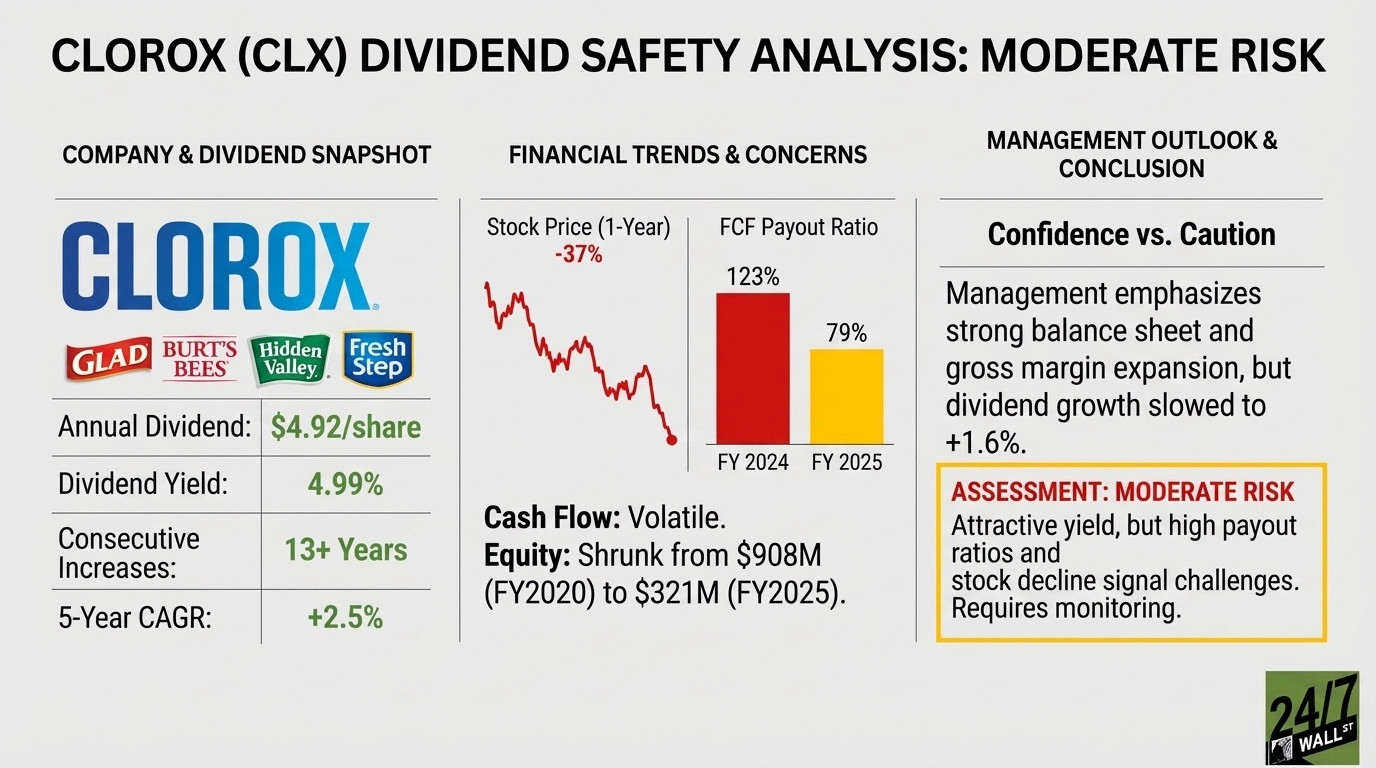

Clorox (NYSE:CLX | CLX Price Prediction) operates household brands including Clorox bleach, Glad trash bags, Burt’s Bees, Hidden Valley, and Fresh Step cat litter. The company pays an annual dividend of $4.92 per share, yielding just under 5%. That yield looks attractive, but it’s elevated because the stock has collapsed 37% over the past year. Can Clorox sustain this dividend, or is that yield a warning sign?

| Metric | Value |

|---|---|

| Annual Dividend | $4.92 per share |

| Dividend Yield | 4.99% |

| Consecutive Years of Increases | 13+ years |

| Most Recent Increase | +1.6% (April 2025) |

| 5-Year Dividend CAGR | +2.5% |

The Cash Flow Picture Is Concerning

Clorox paid $602 million in dividends during fiscal 2025 (ended June 30, 2025) against free cash flow of $761 million. That produces a FCF payout ratio of 79%, elevated but manageable. The problem is the trend. In fiscal 2024, the company paid out 123% of free cash flow as dividends—exceeding what the business generated.

| Metric | FY 2025 | FY 2024 | Assessment |

|---|---|---|---|

| Free Cash Flow | $761M | $483M | Improved but volatile |

| Dividends Paid | $602M | $595M | Stable |

| FCF Payout Ratio | 79% | 123% | Elevated |

Operating cash flow has been erratic, swinging from $1.5 billion in fiscal 2020 down to $695 million in fiscal 2024, then back to $981 million in fiscal 2025. This volatility makes it difficult to assess normalized dividend coverage. The most recent quarter (Q1 fiscal 2026) showed dividends of $151 million against operating cash flow of just $93 million.

Debt Is Manageable but Equity Has Shrunk

Clorox carries $2.88 billion in total debt against $167 million in cash, producing net debt of $2.71 billion. With EBITDA of $1.23 billion, the net debt-to-EBITDA ratio sits at 2.4x—manageable for a consumer staples company.

The balance sheet concern is shareholder equity, which has declined from $908 million in fiscal 2020 to just $321 million in fiscal 2025. This reflects years of paying out more in dividends and buybacks than the company earned. The company spent $332 million on share repurchases in fiscal 2025 despite the elevated dividend payout ratio.

Management Sounds Confident Despite Headwinds

On the Q3 fiscal 2025 earnings call, CEO Linda Rendle acknowledged severe near-term challenges but emphasized operational strength. She noted “we delivered our 10th consecutive quarter of gross margin expansion, which enables us to keep reinvesting in our brands.” CFO Luc Bellet added the company expects tariff headwinds of about $100 million annually but views this as “manageable” through sourcing changes and targeted pricing.

Rendle highlighted the balance sheet position: “We certainly have a strong balance sheet, good cash flow.” That language suggests management views the dividend as secure, though they’ve slowed dividend growth to just 1.6% in 2025 compared to historical increases of 5% to 7% annually.

This Dividend Needs Watching

Dividend Safety Rating: Moderate Risk

Clorox has maintained 13 consecutive years of dividend increases and the fiscal 2025 payout ratio of 79% is technically sustainable. Management expresses confidence in the balance sheet and cash generation. However, the fiscal 2024 payout ratio of 123% and recent cash flow volatility are concerning. The stock’s 37% decline signals the market sees fundamental challenges.

The yield is attractive, but it comes with elevated risk that income investors should acknowledge.