When mortgage rates swing and regional banks wobble, the monthly income checks keep arriving. That’s the promise behind Invesco KBW High Dividend Yield Financial ETF (NASDAQ:KBWD), an ETF delivering a 12.9% yield by concentrating in mortgage REITs and business development companies. For retirees chasing high monthly income, that yield is magnetic. But the cost runs deeper than most realize.

Built for Income, Not Growth

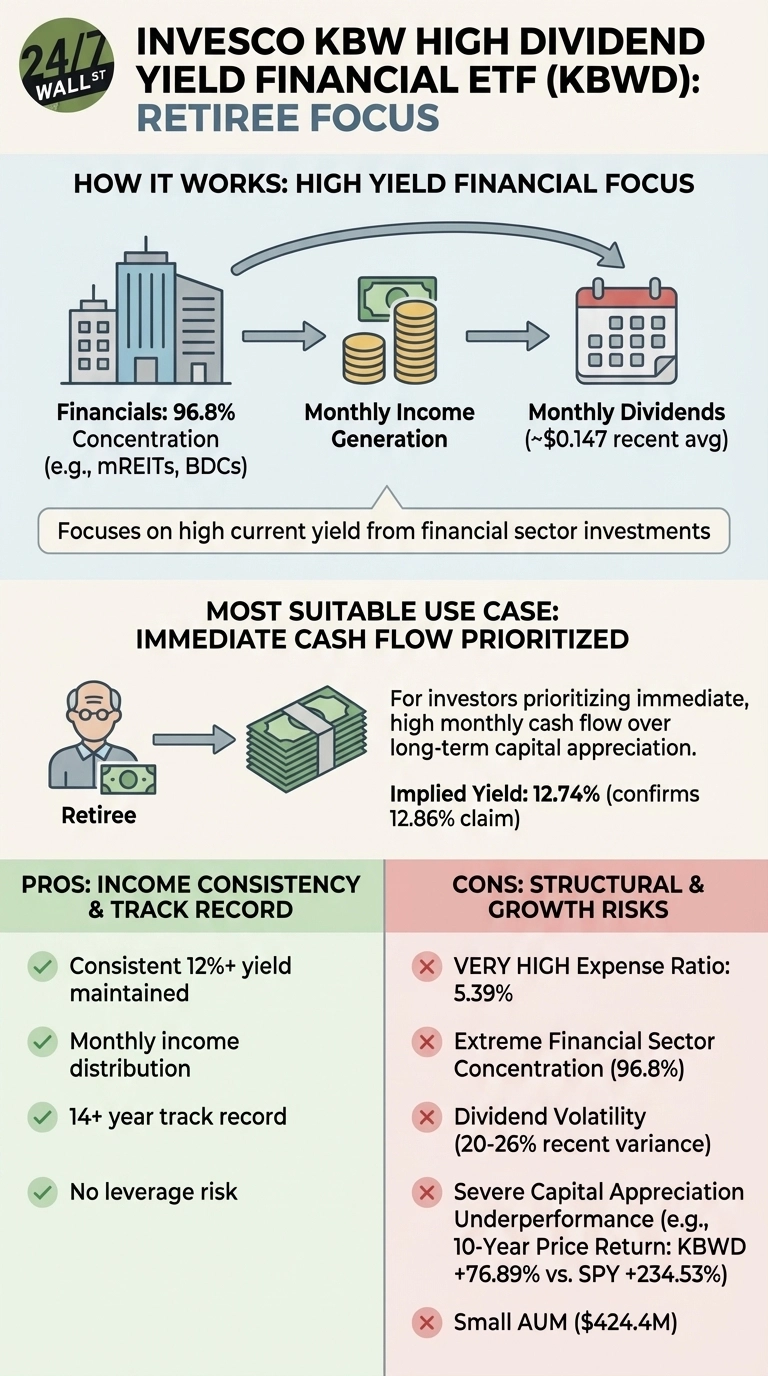

KBWD generates immediate cash flow from financial sector dividend payers. The fund tracks the KBW Nasdaq Financial Sector Dividend Yield Index, with 96.8% of assets in financials and top holdings like Invesco Mortgage Capital, Orchid Island Capital, and AGNC Investment. The portfolio tilts heavily toward mortgage REITs that earn spreads on residential mortgage-backed securities.

These companies borrow short-term funds at low rates, invest in longer-term mortgage securities, and distribute the interest spread as dividends. Monthly payments averaging $0.147 per share provide steady income. KBWD has maintained distributions for over 14 years.

The Price of 12%

The yield comes with structural costs that compound over time. KBWD charges a 5.39% expense ratio, consuming nearly half the gross yield before investors see a penny. Over ten years, that fee alone extracts more value than most equity ETFs generate in returns. The fund also carries a negative cash position and 60% annual turnover.

More concerning is what happens to principal. While KBWD delivered 76.89% total return over ten years, the S&P 500 gained 235%. Even accounting for KBWD’s higher dividends, total returns lag significantly. One Reddit investor who bought 39 shares in 2021 at $19.06 watched the price fall to $13.85 today despite reinvesting all dividends. As they noted, “Even when the market hit several all time highs it never got above $16-$17/share.”

Dividend volatility adds another risk layer. Monthly payments have fluctuated between $0.14 and $0.17 over the past two years, a 21% range. AGNC Investment, the fund’s fourth-largest position, cut its dividend 76% from 2008 peaks. Two Harbors Investment, the third-largest holding, operates at a negative 35.6% profit margin while maintaining a 15.7% dividend yield.

Who Should Avoid KBWD

Retirees who cannot afford principal erosion should look elsewhere. High fees, sector concentration, and interest rate sensitivity create substantial downside risk during economic stress. Anyone in early retirement with 20-plus year horizons will likely see better total returns from diversified dividend strategies.

Tax-sensitive investors face another problem. Because KBWD holds REITs and BDCs, distributions are taxed as ordinary income at your marginal rate, not the favorable qualified dividend rate. In a taxable account, that 12.9% yield becomes roughly 9% after federal taxes for someone in the 28% bracket.

Consider SCHD Instead

For retirees seeking sustainable income with growth potential, Schwab U.S. Dividend Equity ETF (NYSEARCA:SCHD | SCHD Price Prediction) offers a compelling alternative. While the 3.8% yield looks modest compared to KBWD’s 12.9%, the expense ratio is just 0.06% and the fund delivered 200% total returns over ten years versus KBWD’s roughly 200% including dividends.

SCHD diversifies across energy, consumer staples, healthcare, and industrials rather than concentrating in mortgage REITs. The quality-focused approach screens for dividend growth and financial strength, not just current yield. For retirees who need income that grows with inflation and principal that appreciates over time, SCHD’s lower yield paired with capital gains often produces superior total returns.

KBWD delivers exceptional current income for investors who prioritize monthly cash flow over total returns, but the high expense ratio and concentration risk make it unsuitable as a core retirement holding.