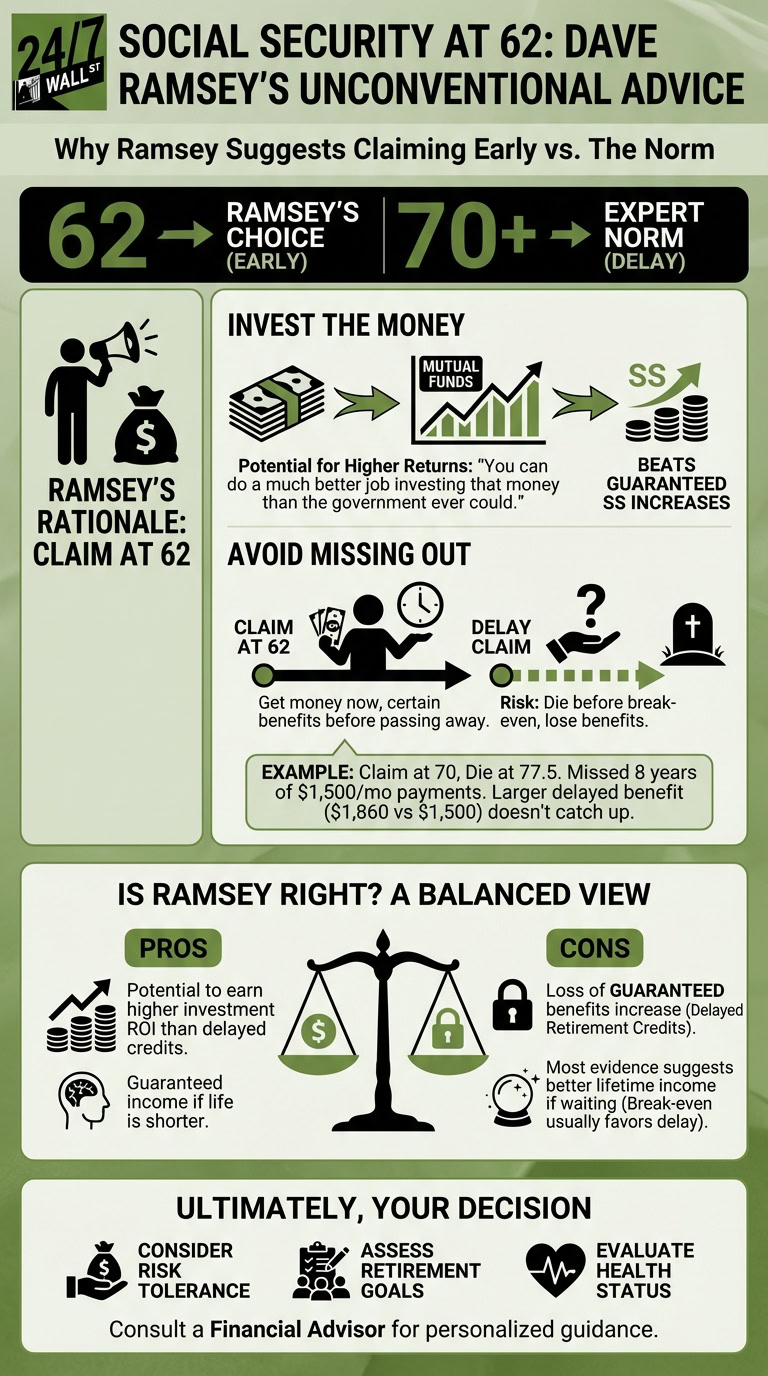

Is 62 the right age to claim Social Security? Dave Ramsey thinks so. In fact, the finance guru has made clear to callers on a podcast that he felt 62 was the right age to claim and there are also posts up on the Ramsey Solutions blog that detail the claiming age Ramsey thinks is best.

Ramsey’s advice to claim Social Security retirement at the earliest age you are allowed to start your checks is a deviation from the norm. Most experts recommend that you start your benefits as late as you can. So, why does Ramsey take a different stance?

There are a few reasons for his suggestion that he’s shared.

1. Ramsey believes you can invest the money and earn better returns

On one podcast where a caller asked when to claim Social Security, Ramsey suggested that the caller start benefits at 62 — but for an unusual reason. Ramsey advised that the caller start his benefits as soon as he could to invest the money. The theory is that if you put your money into mutual funds that give you exposure to equities, you can earn more money than if you just left your benefit alone to grow.

Of course, your benefit does increase if you delay claiming it. For each month you delay beyond age 62, your benefit gets a little bit bigger, either because you’re not getting hit with early filing penalties that apply for claims before your full retirement age, or because you are earning delayed retirement credits that become available for each extra month of delay beyond your FRA.

The Social Security benefits increases you get are guaranteed, but Ramsey believes you can beat them, stating on the Ramsey Solutions blog, ‘You can do a much better job investing that money than the government ever could.”

Ramsey also believes you shouldn’t take the risk of missing out on benefits

Ramsey also thinks it is important to claim early because you don’t know how long you are going to live. After all, your benefits stop when you pass away. If you delay your claim and you die before you start your checks, then you won’t end up getting any of the money out of the Social Security system that you put into it.

Even if you don’t die before getting any checks, Ramsey warns that there’s a risk you’ll pass away before your larger extra benefits make up for the income you missed.

He gives the example of someone who claimed at 70 and died at 77 1/2 years old. If the late claimer had a standard benefit of $1,050, delaying until 7o would have boosted the payment to $1,860 while claiming it at 62 would have shrunk it to $1,500 if the claimer’s full retirement age was 67. While the delayed filer would have gotten more money each month, it wouldn’t have been enough to make up for eight years of $1,500 payments that weren’t collected.

Is Ramsey right?

Ramsey is right that not everyone breaks even for a delayed benefits claim. And, in theory, it might be possible to earn higher returns from investing your Social Security checks than your ROI would be from a delayed claim.

However, there are risks to investing, while the boost in benefits from delaying their start is guaranteed. Plus, while you could die before you break even if you delay, most evidence suggests that the odds are you won’t, and you’ll end up with more lifetime income if you wait until 70.

Ultimately, you need to consider your own risk tolerance, your retirement goals, and your health status when you decide whether listening to Ramsey makes good sense for you or whether a later claim could be a better choice. A financial advisor can help you to make this decision, and it’s worth consulting with one since your claiming age will affect your finances for years to come.