Payoneer (NASDAQ: PAYO) and PayPal (NASDAQ: PYPL | PYPL Price Prediction) just reported Q3 2025 earnings, revealing two payment processors taking wildly different paths into the stablecoin era. Payoneer bets on B2B cross-border infrastructure for digital businesses. PayPal leverages its massive consumer base to push crypto integration at scale. Both stocks are down sharply over the past year.

Payoneer Grows Revenue but Bleeds Earnings Quality

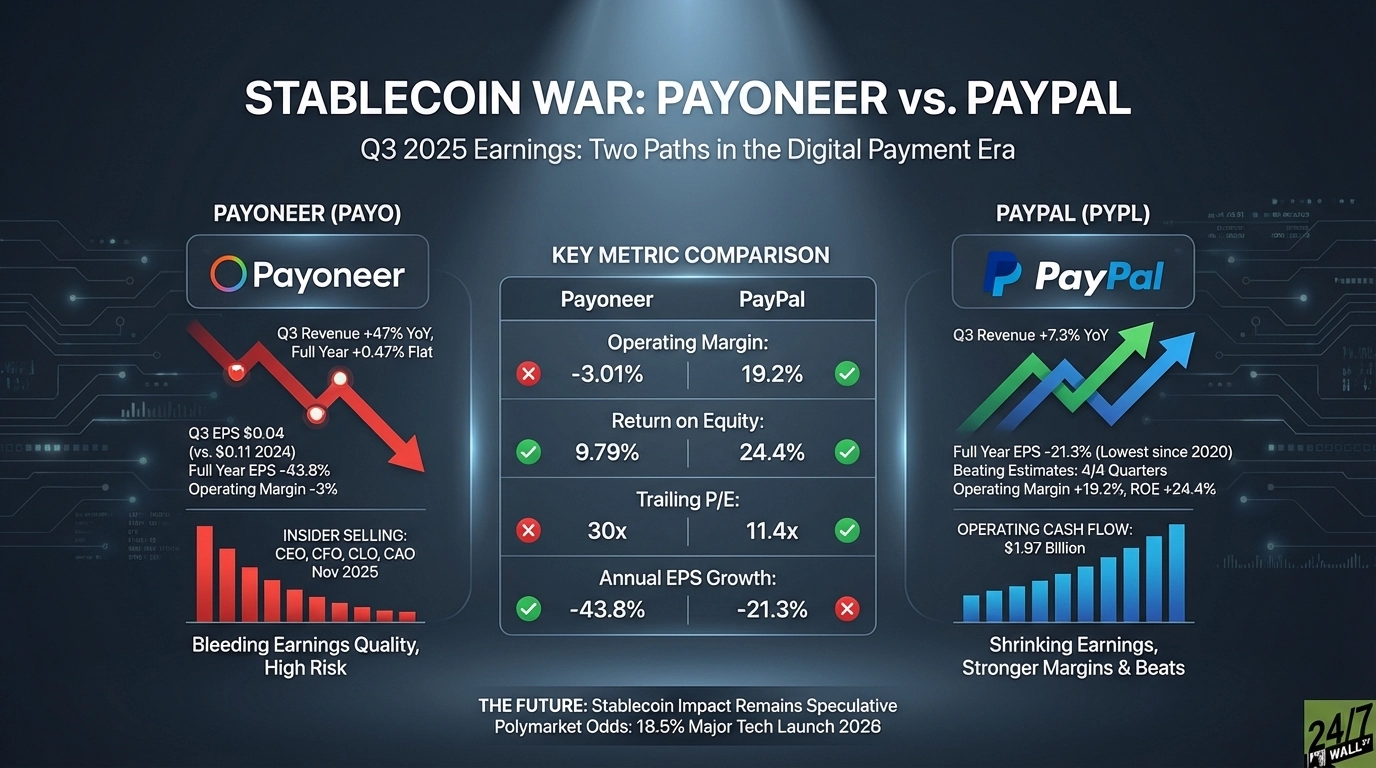

Payoneer posted Q3 revenue of $270.9 million, up 47% year-over-year. That sounds strong until you see the full-year picture. Annual revenue growth for 2025 was just 0.47%, essentially flat. Quarterly earnings per share collapsed from $0.11 in Q3 2024 to $0.04 in Q3 2025. Full-year EPS fell 43.8% from $0.33 in 2024 to $0.19 in 2025. The company missed analyst estimates in three of four quarters this year, with Q3 delivering a 33% negative surprise.

Operating margin sits at negative 3%, meaning Payoneer loses money on core operations despite reporting net income. That gap suggests one-time gains or non-operating income propping up the bottom line. Return on assets is 1.08%, indicating poor capital efficiency. The stock trades at a 30x trailing P/E despite stalled revenue growth, an expensive multiple for a business under this much pressure.

Insiders aren’t buying the dip. CEO John Caplan sold 103,688 shares in November at prices between $5.45 and $5.70. CFO Beatrice Ordonez, Chief Legal Officer Tsafi Goldman, and Chief Accounting Officer Itai Perry all sold shares on the same days. No insider purchases appeared during the stock’s 48% annual decline.

PayPal Shrinks Earnings but Beats Every Quarter

PayPal reported Q3 revenue of $8.42 billion, up 7.3% year-over-year. Full-year EPS fell 21.3% from $4.98 in 2024 to $3.92 in 2025, the lowest since 2020. But unlike Payoneer, PayPal beat analyst estimates in all four quarters of 2025, with Q3 delivering a 14% positive surprise at $1.30 per share versus the $1.14 estimate.

Operating margin is 19.2%, and return on equity is 24.4%, both significantly healthier than Payoneer’s metrics. The stock trades at an 11.4x trailing P/E and a 9.8x forward P/E, suggesting the market expects slower growth ahead. The PEG ratio of 0.58 indicates the stock may be undervalued relative to its growth trajectory. PayPal generated $1.97 billion in operating cash flow last quarter compared to Payoneer’s $54.2 million.

| Metric | Payoneer | PayPal |

| Operating Margin | -3.01% | 19.2% |

| Return on Equity | 9.79% | 24.4% |

| Trailing P/E | 30x | 11.4x |

| Annual EPS Growth | -43.8% | -21.3% |

The Stablecoin War Remains Speculative

Neither company provided detailed stablecoin product updates in their Q3 reports. Polymarket prediction markets assign just 18.5% odds to a major tech platform launching a USD stablecoin in 2026. Revolut gets 49% odds, a coin flip. The U.S. passed stablecoin regulation in 2025, creating a legal framework, but Bank of America’s announced stablecoin never launched despite CEO commitment.

Why I Would Wait on Both

Payoneer’s earnings deterioration is real, not a valuation reset. Three consecutive negative surprises and a 43.8% EPS decline justify the 48% stock drop. Management cannot sustain 2024’s execution quality, and small business customers appear strained. PayPal is operationally stronger but shrinking earnings at a slower rate. The forward P/E of 9.8x prices in continued deceleration. Payoneer reports Q4 earnings February 25, 2026. I will watch whether revenue growth can return and whether management discusses concrete stablecoin timelines. Until then, neither stock offers a compelling entry point. If you believe stablecoins will reshape B2B payments within 18 months, Payoneer is the higher-risk, higher-reward bet. If you want profitability and scale while waiting for crypto adoption, PayPal is the safer hold.