A 70-year-old investor with $2.5 million in blue-chip dividend stocks faces a question many retirees wrestle with: is playing it safe actually risky? On Reddit’s r/Bogleheads forum, one user questioned whether their early-70s father’s portfolio with just 10% in stocks was too conservative, noting it “seems just almost too conservative, where it’s almost at a tipping point where it’s actually risky.”

The portfolio holds five established dividend payers: Johnson & Johnson, Microsoft, Procter & Gamble, Coca-Cola, and Verizon. These are profitable companies with strong margins and decades of dividend payments. But at 70 with a substantial nest egg, the question is whether this approach matches the investor’s actual time horizon and income needs.

| Key Factor | Details |

|---|---|

| Age | 70 years old |

| Portfolio Value | $2.5 million |

| Holdings | 5 blue-chip dividend stocks |

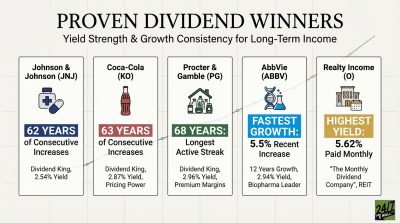

| Current Yields | JNJ 2.31%, MSFT 0.74%, PG 2.85%, KO 2.86%, VZ 6.92% |

| Weighted Average Yield | ~3.1% |

| Estimated Annual Income | ~$77,500 |

The Income Reality: Dividends Alone Won’t Cut It

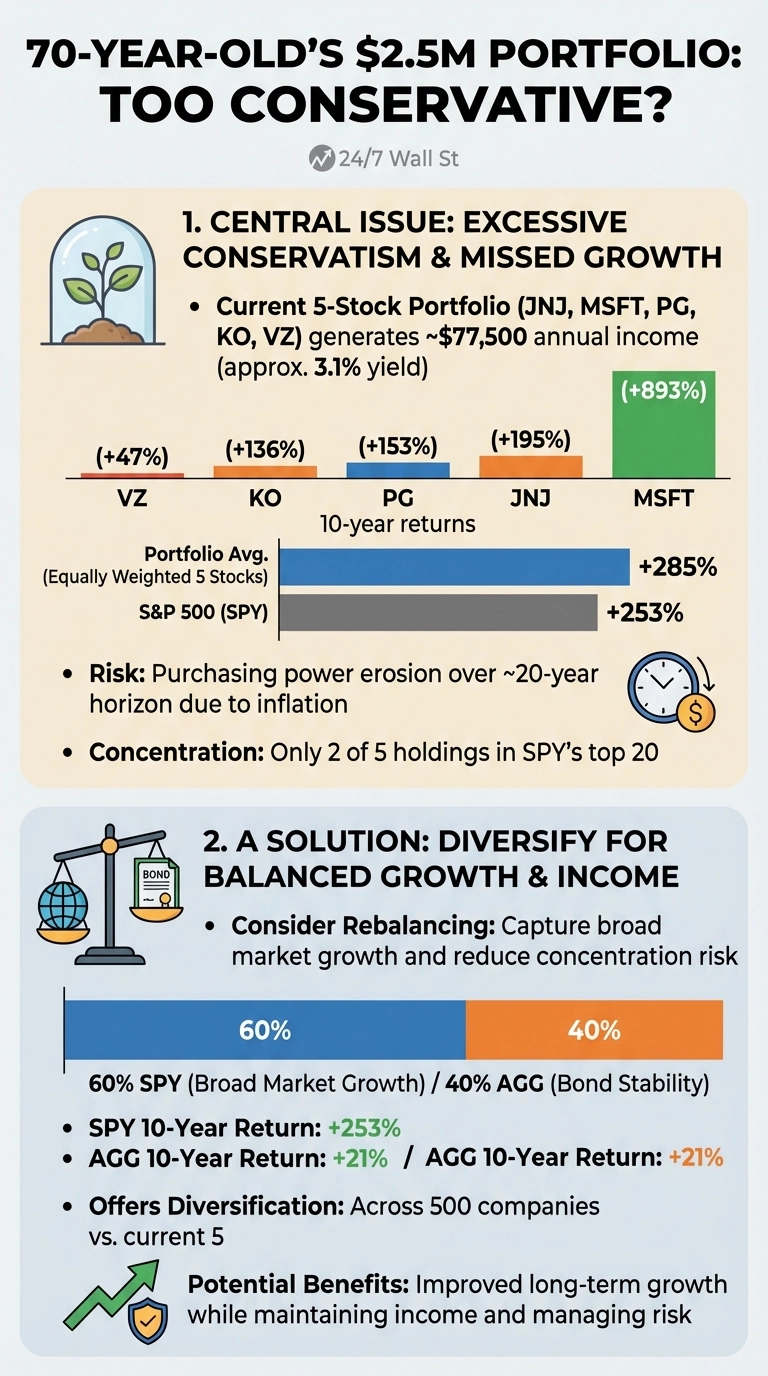

Based on current market prices and dividend yields, this portfolio generates approximately $77,500 annually at a 3.1% weighted average yield. Johnson & Johnson yields 2.31%, Microsoft 0.74%, Procter & Gamble 2.85%, Coca-Cola 2.86%, and Verizon 6.92%. That falls short of the $100,000 a 4% withdrawal rate would provide and misses the growth component that’s driven wealth creation over the past decade.

The 10-year performance data reveals the tension. While defensive holdings like JNJ (+195%), PG (+153%), KO (+136%), and VZ (+47%) delivered respectable returns, Microsoft surged 893%. The S&P 500 gained 253%. A portfolio equally weighted across these five stocks would have grown roughly 285% over 10 years, outpacing the broad market thanks primarily to Microsoft.

At 70, this investor likely has a 20-year time horizon, possibly longer. The traditional “age in bonds” rule would suggest 70% bonds and 30% stocks. This portfolio is 100% equities, which sounds aggressive until you realize four of the five holdings have betas below 0.40 (JNJ 0.33, PG 0.39, KO 0.39, VZ 0.33), meaning they’re significantly less volatile than the market. Only Microsoft, with a beta of 1.07, brings meaningful growth exposure.

The Real Risk: Inflation and Longevity

The biggest threat isn’t market volatility. It’s purchasing power erosion. At 3% annual inflation, $2.5 million loses half its purchasing power in 24 years. Dividend growth helps, but historical dividend growth rates for these companies have varied significantly over the past decade.

Verizon presents a particular concern. Despite its attractive 6.92% yield, the company’s 10-year return of just 47% significantly lags peers. High yield often signals market skepticism about dividend sustainability.

Observations on Similar Portfolios

Some investors in similar situations have chosen to rebalance portfolios to capture both income and growth. A 60/40 split between a broad market index like SPY and a bond fund like AGG provides diversification across 500 companies while maintaining significant equity exposure. Over 10 years, SPY returned 253% versus AGG’s 21%, demonstrating the growth opportunity cost of excessive caution.

Other investors maintaining individual stock approaches have reduced positions in underperforming high-yield stocks in favor of broader technology exposure to improve growth profiles. Microsoft demonstrates that dividend growth and capital appreciation can coexist, delivering 893% total returns over the past decade while maintaining consistent dividend payments.

Considerations for Similar Portfolios

Investors in similar situations often examine their actual income needs. When dividend income plus Social Security covers expenses comfortably, there may be flexibility to optimize for growth. Portfolio concentration in just five stocks raises questions about adequate diversification, particularly with entire sectors like energy, financials, and most of technology absent. Verizon’s lagging performance warrants particular scrutiny given its outsized contribution to the portfolio’s income generation.

Being conservative at 70 makes sense, but bonds returning 21% over 10 years while stocks returned 253% represents real opportunity cost. With potentially two decades ahead, portfolios concentrated in just five defensive stocks may not align with a 20-year time horizon. The question isn’t whether these are quality companies; it’s whether this specific allocation truly serves the investor’s long-term needs.

This analysis is for informational purposes only and not personalized financial advice. Consult a qualified financial advisor for guidance specific to your situation.