Live Earnings: Will Palantir Beat Q4 Estimates?

Quick Read

-

Palantir (PLTR) reports Q4 earnings today with consensus expecting $1.34B revenue and 62% YoY growth.

-

Palantir’s U.S. commercial segment grew 121% YoY in Q3 as enterprise conversions accelerated.

-

Q3 bookings reached $2.8B in total contract value including multiple deals exceeding $10M.

Live Updates

Here's Palantir's Q&A

If you want to watch Palantir’s Q&A you can below; it starts in just a few minutes at 5 p.m. ET:

Analyst Expectations Breakdown: Wall Street Was Bracing for a Beat

Wall Street entered Q4 expecting Palantir to deliver $1.34 billion in revenue and $0.23 EPS — but the consensus masked significant divergence among analysts. The 24-analyst coverage universe leaned cautious: 17 Hold ratings versus just 4 Buy ratings, with an average price target of $190 sitting below the company’s recent highs reached in November.

| Metric | Q4 2025 Estimate | Q3 2025 Actual | Implied Growth |

|---|---|---|---|

| Revenue | $1.34B | $1.18B | +13.5% |

| EPS | $0.23 | $0.21 | +9.5% |

The $0.23 EPS estimate represented a sharp deceleration from Q3’s 24% beat, suggesting analysts were tempering expectations after three consecutive quarters of outperformance. Palantir’s track record — five beats in the past eight quarters — gave bulls confidence, but the Hold-heavy rating distribution reflected valuation concerns at 358x trailing earnings.

Holding to 8% Gains

Palantir is holding to 8% gains before the company’s conference call. We’ll embed that one more time below. We don’t expect any significant movement from what Palantir talks about, but it’s always a very interesting listen.

In other after-hours move AI stocks Teradyne and Rambus are moving in opposite directions. Teradyne blew out earnings and is up about 20% while Rambus is down 20%.

Questions That Are Important for Palantir's Q4 Q&A Call

We pasted an embed of Palantir’s Q&A call above. It’s starting in about 35 minutes. Here are some questions we think will be in focus:

Top 5 Questions Analysts Are Likely to Ask

- U.S. Commercial Sustainability: Can the 115% growth guidance be sustained beyond 2026, or will the market saturate?

- International Acceleration: What specific initiatives will compress deal cycles in overseas markets where AIP adoption lags?

- Margin Trajectory: With 43% net margins in Q4, how much operating leverage remains as revenue scales?

- Government Growth Durability: Can 66% YoY government growth continue amid potential budget constraints?

- Customer Concentration Risk: How diversified is the $4.26 billion contract backlog across industries?

Key Buzzwords to Listen For

Watch for mentions of “bootcamps” (AIP deployment velocity), “land-and-expand” (customer expansion rates), and “Rule of 40” (profitability plus growth). Any discussion of regulatory headwinds or AI governance could signal caution despite strong results.

Palantir Now Routinely Beating Earnings Estimates

Management’s Track Record: Five Beats in Last Eight Quarters

After four consecutive misses between Q4 2021 and Q3 2022, Palantir’s management has rebuilt credibility with five beats in the past eight quarters and zero misses. Recent highlights include Q3 2025’s 23.5% beat ($0.21 vs $0.17 estimate) and Q4 2024’s 23.7% beat ($0.14 vs $0.11 estimate).

The pattern shows management setting conservative estimates and consistently exceeding them by 11% to 24% when they beat. Three quarters landed exactly in-line with estimates, suggesting disciplined guidance.

Today’s Q4 beat of $0.25 versus $0.23 estimate (8.7% above consensus) continues this pattern. More striking: full-year 2026 revenue guidance of $7.18-7.20 billion versus $6.22 billion consensus represents 15% upside, with management projecting 115% U.S. commercial growth.

The aggressive raise signals management confidence has reached new highs after years rebuilding investor trust.

Palantir's Q4 Earnings Get an "A" in Our Earnings Scorecard

Overall Grade: A

Palantir delivered a comprehensive beat-and-raise quarter that exceeded even elevated expectations. Revenue guidance for 2026 implies 64% growth at midpoint — far beyond the 43% Wall Street consensus we mentioned earlier. The company’s execution across all key metrics demonstrates accelerating momentum rather than deceleration.

| Category | Grade | Notes |

|---|---|---|

| Revenue Performance | A+ | $1.407B vs $1.34B estimate (5% beat); Q4 guidance raised $77M above midpoint |

| Earnings Beat/Miss | A | $0.25 EPS vs $0.23 estimate (9% beat); continues Q3’s 24% surprise streak |

| Guidance Quality | A+ | 2026 revenue $7.19B vs $6.22B consensus (16% above); 115% U.S. commercial growth projected |

| Margin Trends | A- | Maintained 33% operating margin from Q3 despite 63% revenue growth |

| Cash Flow | A | Free cash flow exceeded $539M in Q3; Q4 likely sustained strong generation |

| Management Confidence | A | Aggressive 2026 guidance signals conviction in AIP-driven demand durability |

Palantir Webcast Starts at 5 p.m. ET - Watch Below

Palantir’s earnings webcast starts at 5 p.m. ET, we’re embedding it below:

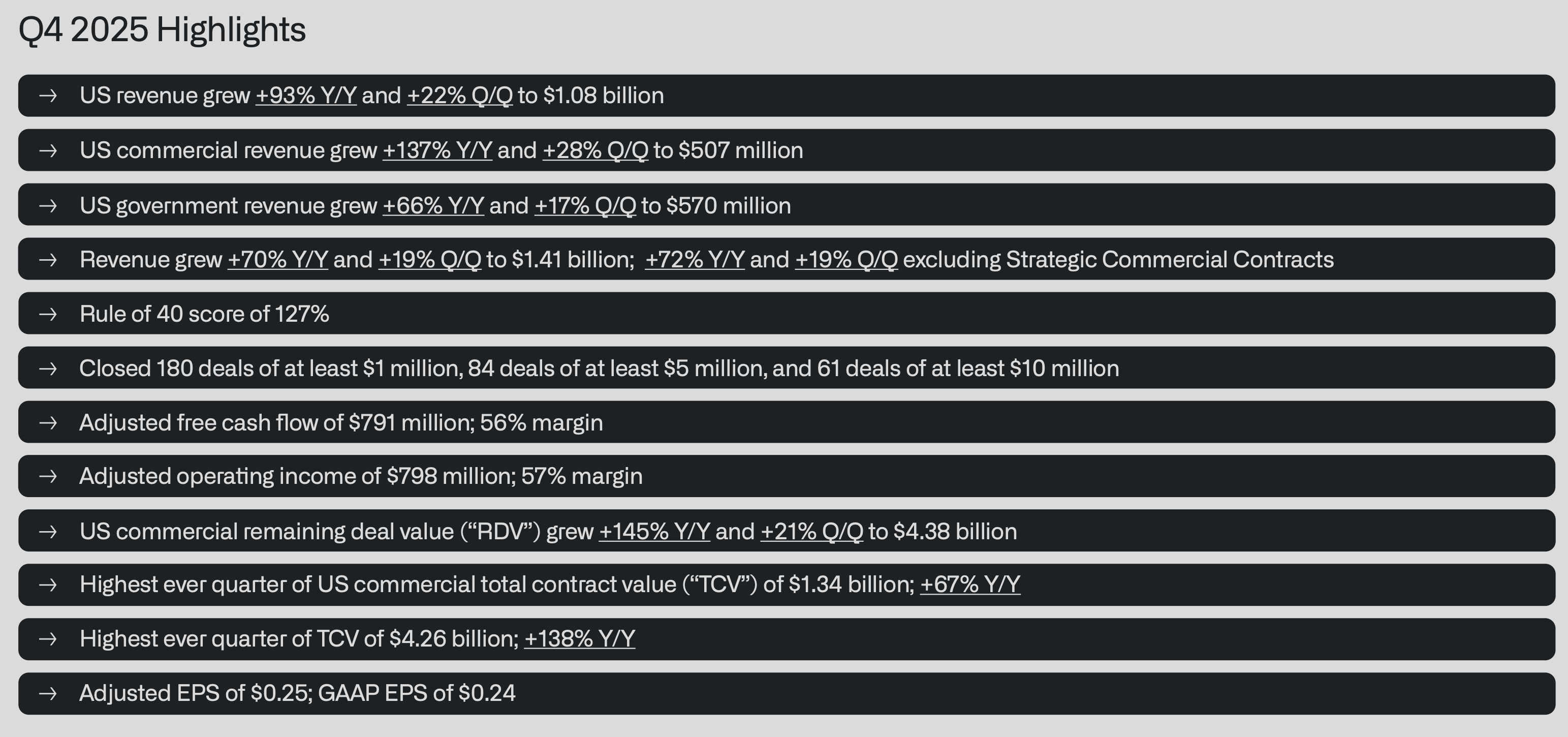

Q4 Highlights from Palantir's Investor Relations Presentation

Shares Are Now up Nearly 8%

5 minutes after earnings hit and shares continue trading up, now up 7.6%.

Palantir had sky high expectations and blew them away.

Q1 Guidance

Here are more details on Palantir’s guidance:

- Q1 revenue of $1.532B To $1.536B vs $1.32B estimates

- Full Year 2026 $7.182B to $7.198B vs $6.22B estimates

We said earlier Palantir would need to significantly outpace the 43% sales growth Wall Street expected and they’ve done it.

Palantir Earnings Are Out

Here’s what Palantir reported in Q4 2025:

- Revenue: $1.407 billion

- EPS (Normalized): $0.25

As a reminder, here’s what Wall Street was expecting:

- Revenue: $1.34 billion

- EPS (Normalized): $0.23

Full-year estimates are significantly beyond US expectations. Guidance for commercial growth is +115% in 2026.

In short, it’s a strong beat and raise. Shares are initially up 6%.

We Expect Palantir Earnings to Hit Newswires at 4:05 p.m. ET

Palantir earnings are expected to hit newswires at 4:05 p.m. ET.

The moment they hit, we will be providing news and analysis. All you have to do is leave this page open, and new updates will appear automatically.

In the mean time, if you’re looking for a great resource for following AI, check out our AI Investor Podcast. The host of the podcast (Eric Bleeker) first called Palantir back in 2024.

We’ll be discussing Palantir’s earnings on the next episode, so subscribe now!

Palantir Shares Are Down 12% in the Past Month

Palantir shares are down about 12% in the past month and 30% from their all-time highs reached in early November.

The company is under pressure as software valuations come under more scrutiny. Palantir has one of the clearest ‘narratives’ of more sales growth as AI accelerates, but it’s not immune to the broad sell-off across the sector.

Even with the sell-off, Palantir will have little margin for error tonight. Wall Street currently expects 43% sales growth in 2026, but the ‘whisper number’ is likely higher.

International AIP Adoption Is the Wildcard for 2026 Growth

One under-discussed swing factor is international commercial growth. Management acknowledged U.S. demand is dramatically outpacing international markets, where deal cycles remain longer and AI adoption is less standardized. Investors will listen closely for any signs that AIP traction is beginning to compress overseas sales cycles or whether growth remains heavily U.S.-concentrated into 2026.

Palantir Technologies (NASDAQ: PLTR | PLTR Price Prediction) reports fourth-quarter 2025 earnings today after the bell. Consensus expectations imply the company is still in a high-velocity growth phase coming off a Q3 print that management framed as a step-function quarter in U.S. execution, bookings, and profitability.

What to Expect

- Revenue: $1.34 billion

- EPS (Normalized): $0.23

Full-year forecasts:

- FY 2025 Revenue: $4.40 billion

- FY 2025 EPS: $0.73

Against the prior-year comp shown on the estimates page, Q4 revenue is implied up 62% YoY (from $827.52M a year ago) and EPS is implied up from $0.14. For context on execution, the company has also posted positive EPS surprises in each of the last four reported quarters listed.

Key Areas to Watch

U.S. commercial expansion cadence

Investors will watch whether U.S. commercial continues to scale at triple-digit rates, after management cited 121% YoY U.S. commercial growth and highlighted accelerating conversions into larger enterprise agreements.

Bookings quality and “large deal” repeatability

Management emphasized a record $2.8B total contract value quarter with a high count of $1M+, $5M+, and $10M+ deals. The setup into Q4 is whether that “big deal” profile remains robust or normalizes.

AIP product leverage and deployment productivity

The call leaned heavily on AI FDE and “Hivemind” capabilities as drivers of faster delivery and higher internal productivity. Investors will want evidence this translates to faster time-to-value and broader rollouts across customers.

Government momentum and platform consolidation signals

On Q3, leadership pointed to strong U.S. government growth and cited an Army directive to consolidate on Vantage. Q4 focus is whether these signals turn into sustained revenue acceleration and follow-on programs.

Margins, cash flow, and investment intensity

Management highlighted 51% adjusted operating margin and $508M cash from operations in Q3 while also flagging continued product and technical hiring investment. Investors will watch for any margin give-back versus continued outperformance.

Eric Bleeker has been investing for more than 20 years. He began his career working at Microsoft before joining Motley Fool, one of the largest publishers of financial research. In his 15 years at Motley Fool Eric served as the General Manager for Fool.com and led coverage in the Technology & Telecom sector. In addition, he was a featured columnist and has hosted dozens of investing seminars attended by more than a million total investors. Eric has more than 1,000 financial bylines to his name and has been featured in The Wall Street Journal, CNBC, Fox Business, and many other leading publications. He is currently focused on artificial intelligence investing and is a CFA Charterholoder.

© 24/7 Wall St.