Global WFE Market Share and Competitive Positioning

Chinese semiconductor equipment vendors continue to gain share within the global WFE market, although the absolute level remains modest. Global leaders such as Applied Materials (AMAT), Lam Research (LRCX), KLA (KLAC), ASML (ASML), Tokyo Electron (TOELY), and Screen still dominate the market, particularly in leading-edge logic and memory.

Chinese vendors, including NAURA, AMEC, ACM Research (ACMR), Hwatsing, Piotech, and Kingsemi, collectively accounted for just 6.5% of the global WFE market of $41.4 billion in 2025. While small, it grew from 5.6% in 2024 and just 1.2% in 2021.

While the absolute share remains limited, the direction of incremental share within China is shifting toward domestic suppliers. This shift is not large enough to change global rankings, but it is increasingly relevant for companies that historically relied on China as a primary growth driver.

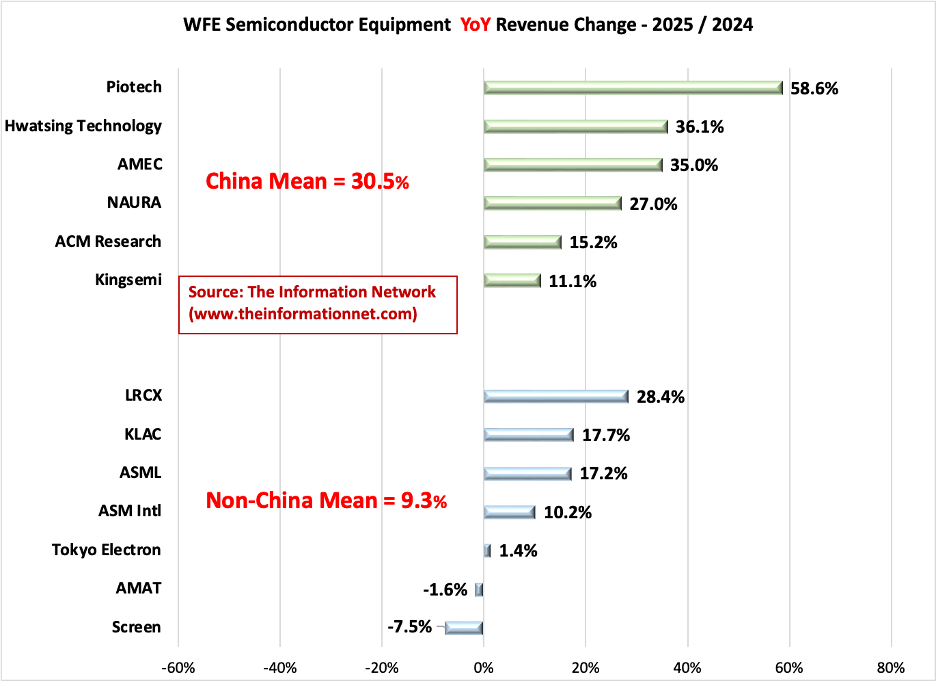

According to Chart 1, and noted in my report entitled “Global Semiconductor Equipment: Markets, Market Shares, Market Forecasts,” which can be previewed on my website at The Information Network, Lam Research exhibited the greatest year-on-year revenue growth in 2025 at 28.4%, ahead of global market leader ASML, growing 17.2%. ASML increased its lead over perennial market leader Applied Materials due to lackluster YoY performance of -1.6%.

The mean 2025/2024 revenue growth of these top non-Chinese companies was just 9.3% compared to 30.5% for Chinese companies. Below is a brief profile of the Chinese companies listed in Chart 1.

Piotech is a China-based semiconductor equipment company focused on thin film deposition, particularly PECVD and ALD systems used in advanced packaging, compound semiconductors, and memory. Its tools are increasingly being adopted in domestic fabs where foreign suppliers have historically dominated these process steps.

Hwatsing Technology manufactures chemical mechanical polishing (CMP) equipment and consumables used for wafer planarization. CMP is a critical step in both logic and memory production, and Hwatsing has gained traction supplying domestic Chinese fabs.

AMEC (Advanced Micro-Fabrication Equipment Inc.) is one of China’s leading etch equipment suppliers, with plasma etch tools used in both logic and memory applications. The company has steadily improved its capability at more advanced nodes, positioning it as a key domestic alternative to global suppliers.

NAURA Technology Group offers one of the broadest portfolios among Chinese equipment companies, including etch, PVD, CVD, and thermal processing tools. Its diversification across multiple process steps has made it a major beneficiary of China’s push toward semiconductor self-sufficiency.

ACM Research develops wafer cleaning, electrochemical plating (ECP), and related process technologies used to improve yield in semiconductor manufacturing. Its tools are particularly important at advanced nodes, where contamination control becomes increasingly critical.

Kingsemi manufactures track systems used in photolithography, including coat and develop tools that operate alongside lithography equipment. These systems are essential for front-end wafer processing and represent one of the areas where Chinese vendors have made measurable progress.

According to my report noted above, Naura and AMEC were among my Top 10 list of equipment companies in 2025 based on revenue.

Chart 1: WFE Semiconductor Equipment Revenue Growth – 2025 vs. 2024 (China vs. Non-China Vendors)

China Remains a Large Market—but the Mix Is Changing

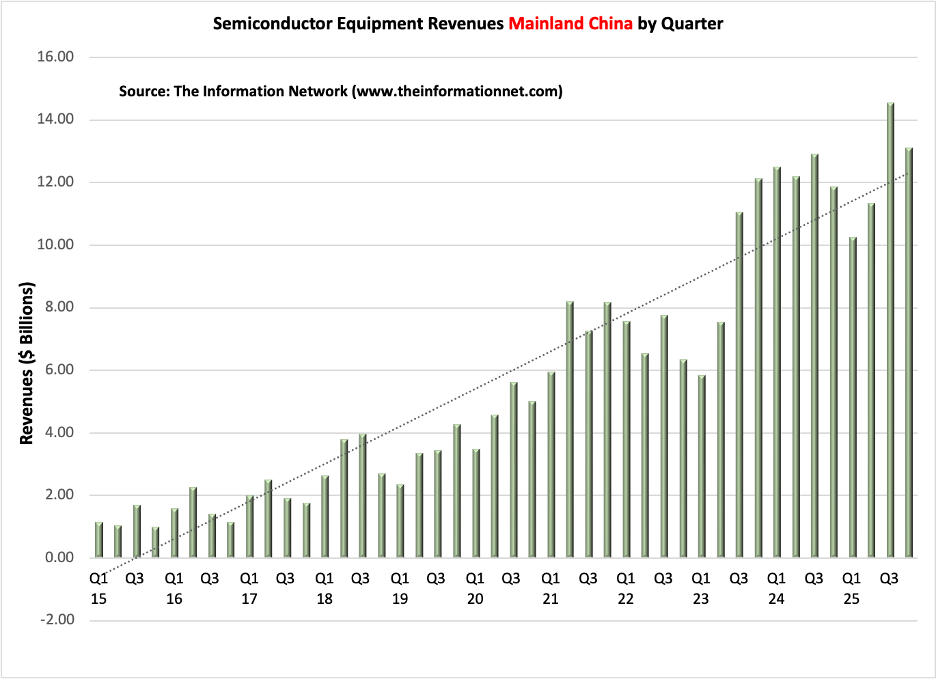

Chart 2 shows revenues of equipment into China between Q1 2015 and Q4 2025, from both imports and domestic production. The trendline (green dotted line) shows consistently positive growth beginning in 2015, but hoarding of equipment by the Chinese for fear of further U.S. sanctions.

Chart 2: Semiconductor Equipment Sales to China (China vs. Non-China Vendors)

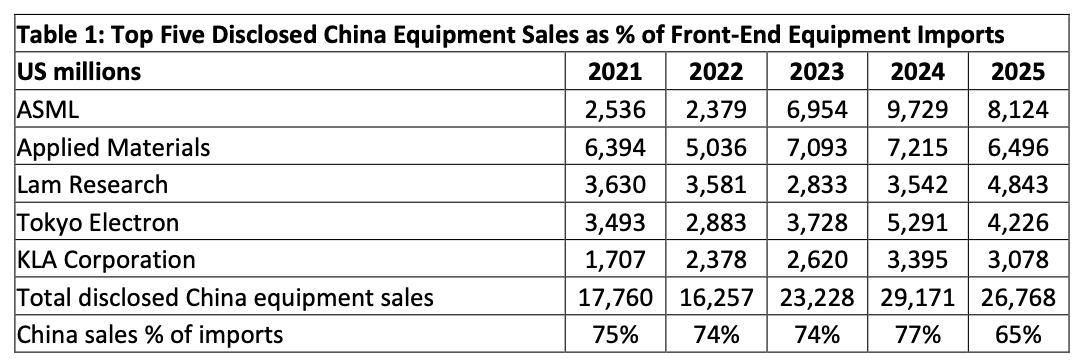

Table 1 shows China Sales by Equipment company to China in CY 2021 to 2025 for comparison. Revenues from China sales increased from $17,760 million in 2021, to $26,768 million in 2025 peaking at $29,171 million in 2024.

According to Table 1, disclosed China equipment sales for the top five global suppliers remained significant in 2025, but the data shows a shift in how that demand is being captured. In 2021, 75% of equipment sales in China were from imports. As a result of strong sanctions, China as a nation began programs to promote the expansion of internal domestic equipment company sales. In 2025, just 65% of equipment sold in China was imported. China demand has not disappeared, but that a smaller portion of that demand is being fulfilled by foreign suppliers.

Chinese equipment suppliers largely serve the domestic market and have made inroads in segments such as RTP, oxidation/diffusion, sputtering, CMP, and cleaning, with etch and deposition representing higher-growth opportunities. These companies are not yet competitive across all leading-edge segments, but they are increasingly able to satisfy demand at mature and mid-critical nodes.

Chinese equipment suppliers largely serve the domestic market and have made inroads in segments such as RTP, oxidation/diffusion, sputtering, CMP, and cleaning, with etch and deposition representing higher-growth opportunities. These companies are not yet competitive across all leading-edge segments, but they are increasingly able to satisfy demand at mature and mid-critical nodes.

ASML, DUV Lithography, and the Multiplier Effect

In 2025, ASML generated 29.4% of revenues ($8,124 million) from China out of total revenues of $27,589 million. An important consideration for the other companies in 2024 is that DUV lithography sales, even though in 2023, semiconductor equipment was imported for the processing of mature and mid-critical nodes to China, as vendors complied with export control regulations.

It must be remembered that ASML’s flagship EUV (extreme ultraviolet) lithography system, priced exceeding $250 million, has been sanctioned for sales to China since the Trump administration.

But immersion DUV systems have been largely exempt from U.S. Sanctions, except for a few of ASML’s high-end systems. And the growth of DUV sales results in growth of other processing types of equipment.

Why? Because DUV lithography on its own only works up to the 39nm technology node. At nodes smaller than 39nm, multi-patterning processes need to be used, and these processes use deposition and etch equipment from AMAT, LRCX, and TEL. Limiting DUV sales to China for mature and mid-critical nodes will significantly impact sales of etch and deposition equipment in 2026 and beyond.

KLAC is the biggest beneficiary of DUV systems in China (and, of course, other regions) because the smaller the technology node, the greater the need for KLAC’s inspection/metrology equipment demanded to maintain high manufacturing yields. I discussed this issue in detail in my May 15, 2024 Seeking Alpha article entitled KLA: Benefiting From The Need For High Yields In Sub-5nm Chip Production.

At the 28nm node, no EUV systems are required anyway, and 10 DUV immersion systems are required for the 50,000 wafers per month (wpm). At 7nm, normally 15 DUV systems and 5 EUV systems are demanded, depending on chip type and company. However, since Chinese fabs such as SMIC are not permitted to use EUV by U.S. sanctions, then they will be substituted by DUV, and 20 DUV systems will be used.

In both cases, multiple patterning is done to delineate that pattern, whether it is 28nm or 7nm. This multiple patterning process is more or less a trick to reach even the 28nm dimensions. The multiple patterning is typically a combination of deposition, etch, and lithography steps.

For a fab making 50,000 wpm at 28nm, in addition to the 10 DUV immersion systems, multiple patterning will demand 125 etchers and 200 CVD systems. At 7nm, in addition to the 20 DUV immersion systems, multiple patterning will demand 350 etchers and 175 CVD systems. Clearly, non-lithography equipment suppliers benefit from the sale of DUV systems.

Export Controls and Their Impact

As for the impact of U.S. sanctions on China, in October 2023, the U.S. government published updated export control regulations, according to ASML. The regulations consist of both an update from the October communication of the previous year and the implementation of U.S. regulations within the trilateral agreement involving the Dutch, Japanese, and U.S. governments.

On October 17, 2023, the US Department of Commerce’s Bureau of Industry and Security (BIS) declared that lithography machines with a maximum “dedicated chuck overlay (DCO)” value between 1.5nm and 2.4nm are prohibited from being shipped from the U.S. to China. The DCO value serves as an indicator of imaging performance, with smaller values indicating higher accuracy.

Under these new rules, the BIS has imposed a ban on shipments of ASML’s NXT:1980Di and NXT:1970Ci machines, which have maximum DCO values of 1.6nm and 2nm, respectively, from the U.S. to China. As of now, there is no indication that the Dutch government will follow suit.

ASML expects that these sanctions will impact its sales to China by -10 to -15%. And that would mean lower sales from AMAT, LRCX, and TEL.

The U.S. has continued to tighten export restrictions, most recently this past week, ordering semiconductor equipment companies to halt certain shipments to China’s second-largest foundry, Hua Hong Semiconductor.

Market Performance Reflects Diverging Fundamentals

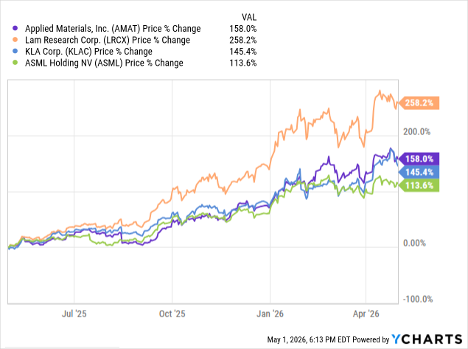

According to Chart 3, semiconductor equipment stocks have diverged significantly, with Lam Research outperforming its peers over the past year.

Lam Research has gained 258.2%, compared to 158.0% for Applied Materials, 145.4% for KLA, and 113.6% for ASML.

Ironically, share growth does not correlate with revenue performance or market leadership of the four companies. Share price for LRCX does correlate with YoY revenue growth for the company as illustrated in Chart 1. However, AMAT’s share price performance does not corelate at all with revenue growth in 2025, which was -1.6%. KLA’s share growth was 145.4%, yet the company dominates the metrology/inspection market, and is products are critical to maintaining high yields, particularly at the sub-5nm node. ASML leads the global equiment market, and its leadership is growing. It has a 100% share of the EUV lithography market and a 90% share of the DUV lithography market. Yet its share price has performed the worst.

Chart 3: Semiconductor Equipment Stock Performance

Conclusion

Chinese semiconductor equipment vendors remain a small portion of the global market at approximately 6.5% share, but their continued growth within China is beginning to affect the distribution of demand across suppliers. While global leaders continue to dominate in advanced technology nodes less than 5nm, domestic vendors are increasingly able to meet requirements at mature and mid-critical nodes, particularly in process steps such as etch, deposition, cleaning, and thermal processing. Remember that U.S. sanctions against China limited production of logic chips below 14nm and memory chips below 18nm. These sanctions have currently moved away from node-specific to node-agnostic, meaning that some specialized types of equipment, such as tools for advanced packaging or DUV lithography systems, are restricted regardless o node capability.

The issue for global semiconductor equipment companies is not the loss of global leadership, but the gradual reduction of their share within China. As shown in Table 1 above, the percentage of China equipment imports captured by the top five suppliers declined from 77% in 2024 to 65% in 2025. In a period where overall WFE growth is slowing, even incremental share loss in China can impact revenue growth, particularly for companies with high exposure to that market.

U.S. sanctions against China have been in existence for more than 6 years under two different administrations. They have been designed to prevent the development of sophisticated chips that can be used by the Chinese military, particularly at 5nm and lower nodes, which are being manufactured by Taiwan Semiconductor (TSMC) (TSM) and Samsung Electronics (SSNLF). As shown above in Chart 2, demand for semiconductor equipment in China continues, despite the legal node of export regulations. Yet the Chinese have made significant strides of reaching the 7nm and lower nodes even without the ability to import EUV lithography equipment from ASML.