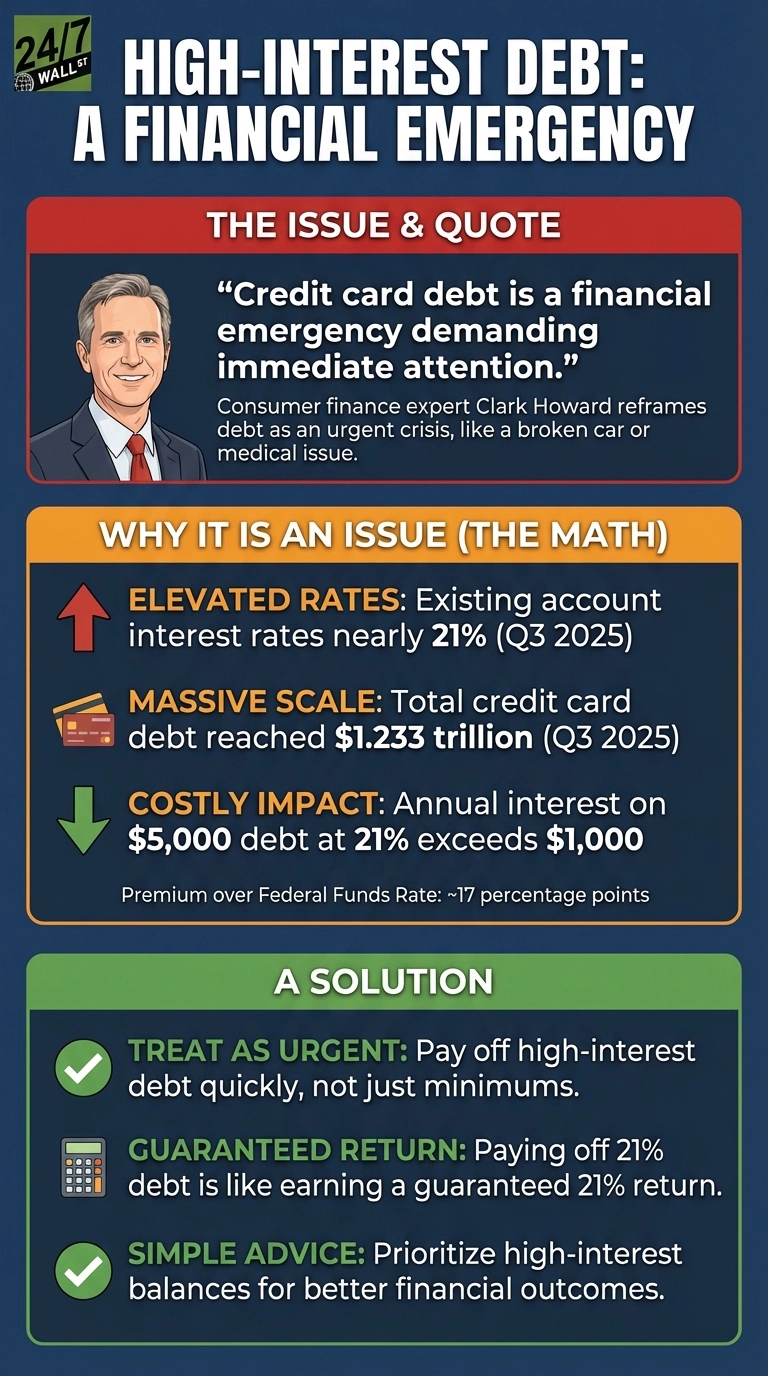

Consumer finance expert Clark Howard has long maintained a straightforward position on credit card debt: it’s a financial emergency demanding immediate attention. His reasoning centers on a mathematical reality many Americans overlook—high-interest debt compounds faster than most people can realistically pay it down.

The Quote and Why It Resonates

Howard, host of The Clark Howard Podcast and founder of Clark.com, classifies credit card debt as an emergency requiring urgent action. The message reframes debt from a common financial burden into something requiring the same urgency as a broken-down car or medical crisis. It’s simple, direct, and cuts through the rationalization that keeps many people making minimum payments indefinitely.

Where the Math Supports Howard’s Warning

The current credit card environment validates Howard’s alarm. Interest rates on existing accounts have climbed to nearly 21%, transforming what might once have been manageable debt into a genuine financial trap. These elevated rates create a compounding problem where interest charges accumulate faster than many households can realistically pay them down.

The scale of the problem has grown substantially. Total credit card debt reached $1.233 trillion as of Q3 2025, reflecting how millions of American households are caught in this high-rate environment. This isn’t just a number—it represents real financial stress affecting retirement planning, emergency preparedness, and long-term wealth building.

The math reveals why this qualifies as an emergency. Consider a typical household carrying $5,000 in credit card debt at today’s rates—they’ll pay over $1,000 annually just in interest charges before touching the principal. This money disappears into interest payments rather than building wealth or funding retirement, creating a financial drain that compounds year after year.

The premium consumers pay for revolving debt has reached extreme levels. Credit cards now charge roughly 17 percentage points above the Federal Funds Rate, meaning households face a massive markup on borrowed money compared to other forms of credit.

Howard’s emergency framing makes particular sense when compared to typical investment returns. Even investors seeking market returns lose ground if they’re simultaneously carrying debt at 21%. The math is unforgiving: paying off high-interest debt delivers a guaranteed 21% “return” through avoided interest charges.

What the Advice Leaves Out

Howard’s guidance is directionally correct but requires context about timing and household circumstances. The emergency designation assumes someone has basic liquidity—enough cash to cover immediate needs. A person with zero savings and $3,000 in credit card debt faces a different calculation than someone with $10,000 saved and the same debt load.

The advice also doesn’t account for debt at substantially lower rates. Someone with a 0% promotional APR still has six months remaining should focus on building emergency savings first, then tackle the balance before the promotional period expires.

How to Think About This Advice

Most retirees and pre-retirees should treat Howard’s warning seriously. With consumer sentiment at 52.9 as of December 2025—well below the neutral threshold—financial stress is widespread, and high-interest debt accelerates that pressure.

The key question: Are you paying more in credit card interest than you’re earning on savings? If yes, Howard’s emergency framing applies. If you’re carrying balances at today’s average rates while earning 4.24% on Treasury bonds, you’re losing 16 percentage points annually. That’s not sustainable for anyone approaching or living in retirement.

Well-known advice often simplifies complex situations, but in this case, the simplification serves most people well. High-interest debt is expensive, and treating it as urgent typically leads to better outcomes than gradual payoff plans.