Qualcomm Live: Complete Coverage Of QCOM’s Q1 Earnings

Quick Read

-

Qualcomm (QCOM) shares fell 14.7% over four weeks. Analysts cut targets to $160 on reduced Apple modem share and Samsung’s internal transition.

-

Qualcomm’s automotive and IoT segments delivered 27% combined growth in fiscal 2025 to offset declining handset demand.

Live Updates

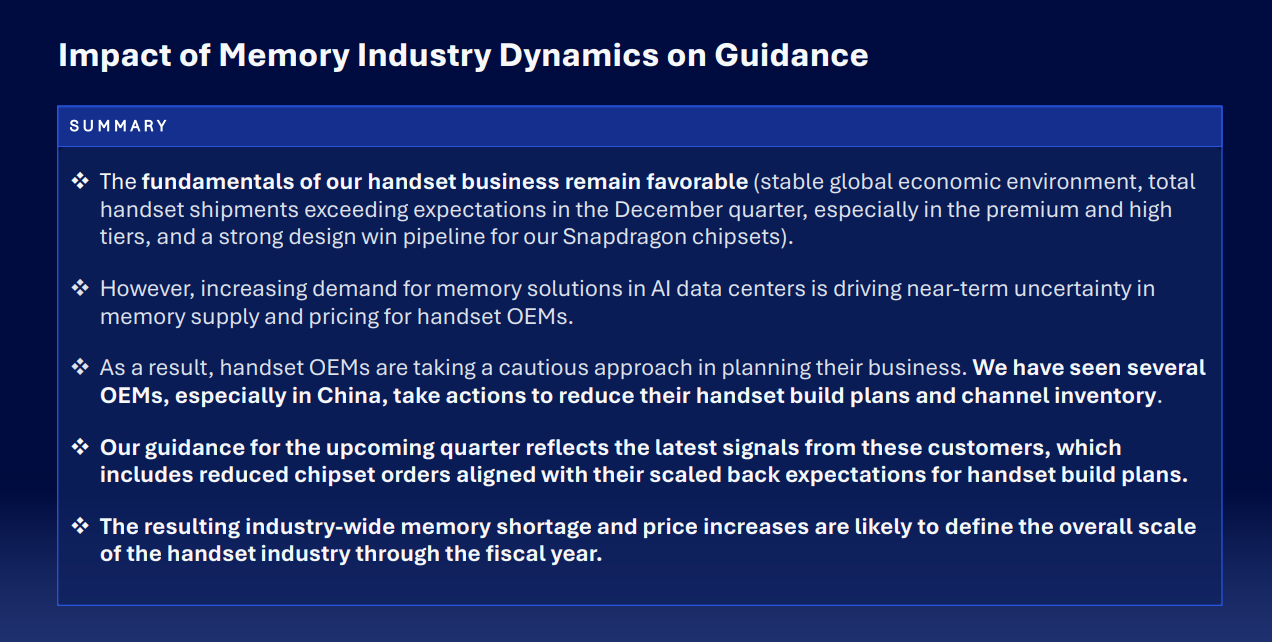

More on Memory Shortage

The Phrase That Spooked Investors

Memory Supply Constraints.

This is not exclusive to Qualcomm, memory shortage is a large bottle neck, just look at Sandisk earnings.

Management explicitly blamed industry-wide memory shortages tied to AI data centers, which are now:

- Raising memory prices for handset OEMs

- Forcing OEMs (especially in China) to cut build plans and channel inventory

- Leading Qualcomm to guide lower chipset orders next quarter

This is a new macro overhang for QCOM’s core handset business and directly undercuts last quarter’s confidence tone.

The Real Problem: Q2 Guidance

Qualcomm’s Q2 FY26 guidance is what broke the stock:

| Metric | Q2 FY26 Guidance |

|---|---|

| Revenue | $10.2B – $11.0B |

| Non-GAAP EPS | $2.45 – $2.65 |

| QCT Revenue | $8.8B – $9.4B |

| QCT EBT Margin | 26% – 28% (down from 31%) |

That EPS guide implies a 25% sequential decline from Q1’s $3.50, far worse than investors were modeling.

Earnings Are In and Stock Down

Immediately after releasing earnings, Qualcomm stock is down 5.29%.

At the headline level, Qualcomm did what it was supposed to do:

- Revenue: $12.25B (record, +5% YoY)

- Non-GAAP EPS: $3.50 (top end of guidance, +3% YoY)

- QCT Automotive: $1.1B (+15% YoY, second straight quarter >$1B)

This was not a miss quarter. The stock is down because the forward outlook reset expectations sharply lower.

3 Takeaways from Qualcomm's Last Quarter Earnings

- Record results beat across the board: Revenue of $11.3 billion and EPS of $3.00 both exceeded high end of guidance, with record QCT revenues of $9.8 billion. Full-year FY25 revenue hit $44.1 billion (up 13% YoY) with record QCT operating margins of 30%. Non-Apple QCT revenues grew 18% YoY, surpassing prior estimates, driven by premium Android adoption of Snapdragon 8 Elite Gen 5.

- AI smart glasses breakout hit: XR segment significantly exceeding expectations on explosive Meta Ray-Ban demand, with 30 designs in production/development across partners including Samsung’s new Galaxy XR. Smart glasses emerging as personal AI devices at inflection point. Automotive crossed $1 billion quarterly milestone (up 36% YoY) with launch of Snapdragon Ride Pilot L2+ system in BMW, validated in 60+ countries.

- Data center entry accelerated: Unveiled AI200/AI250 inference-optimized chips with HUMAIN as first customer targeting 200MW deployment starting 2026. Pulled forward data center revenue materiality from FY28 to FY27, representing potential multibillion-dollar opportunity. Maintains 75% Samsung baseline share assumption for Galaxy S26; guiding record Q1 with low-teens sequential handset growth on continued premium Android strength.

Qualcomm (NASDAQ: QCOM | QCOM Price Prediction) reports first-quarter fiscal 2026 results today after the market close at 4:00 PM ET. After shares dropped 14.7% over the past four weeks to $151.53, investors are watching whether the chipmaker can sustain momentum despite mounting headwinds in its core handset business.

Pressure Building on Multiple Fronts

Cantor Fitzgerald cut its price target to $160 from $185 on February 4, citing conservative guidance driven by Apple’s reduced modem share, Samsung’s internal modem transition, and a declining Chinese handset market. Mizuho followed with a $160 target, projecting a 4% year-over-year decrease in global handset estimates for 2026.

Handsets remain Qualcomm’s largest revenue driver. Last quarter, the company reported QCT segment revenue of $9.82 billion, the bulk from smartphone chips. Management highlighted 18% growth in non-Apple QCT revenues during the fiscal fourth quarter, but that diversification faces headwinds as major customers shift strategies.

Consensus Expectations

| Metric | Q1 FY2026 Estimate |

|---|---|

| Non-GAAP EPS | $3.39 |

| Revenue | $12.21 billion |

What I’m Watching Beyond the Print

Qualcomm has beaten earnings estimates for eight consecutive quarters, with surprises ranging from 1% to 14%. Prediction markets price an 88% probability the company beats the $3.39 EPS consensus, reflecting confidence despite recent downgrades.

I’ll focus on three areas. First, management’s tone on handset demand through the March quarter and beyond. The company guided first-quarter revenue between $11.8 billion and $12.6 billion in November. Whether they maintain or adjust that range will signal how quickly headwinds are materializing.

Second, automotive and IoT growth rates matter more now. Last quarter, Automotive revenue hit $1.05 billion, up 17% year-over-year, while IoT grew 7% to $1.81 billion. Combined, these segments delivered 27% growth for full fiscal 2025. Sustaining that momentum would offset handset weakness.

Third, I’m watching for commentary on the Ventana Micro Systems acquisition and how it strengthens Qualcomm’s custom CPU roadmap after key Nuvia founder exits.

Execution Needs to Match the Story

After delivering $44.28 billion in fiscal 2025 revenue and returning $3.4 billion to shareholders through dividends and buybacks, Qualcomm’s financial foundation remains solid. But with shares trading down 12% year-to-date and well below the analyst average price target of $187.69, this quarter needs to prove the diversification strategy can offset smartphone market pressure. Management’s guidance and tone will matter more than the headline numbers.

Joel South covers large-cap stocks, dividend investing, and major market trends, with a focus on earnings analysis, valuation, and turning complex data into actionable insights for investors.

He brings more than 15 years of experience as an investor and financial journalist, including 12 years at The Motley Fool, where he served as an investment analyst, Bureau Chief, and later led the Fool.com investing news desk. He has also co-hosted an investing podcast and appeared across TV and radio discussing market trends.

© 24/7 Wall St.