Reddit Live: Complete Coverage Of RDDT’s Q4 Earnings

Quick Read

-

Reddit (RDDT) stock dropped 40% in one month despite eight consecutive earnings beats and strong profitability.

-

Reddit delivered $584.9M revenue in Q3 with 68% growth. Advertising revenue jumped 74% year-over-year.

-

Q4 guidance targets $660M revenue reflecting 54% growth. Consensus expects $0.93 EPS down from Q3’s $1.26.

Live Updates

$1B Buyback

The surprise $1 billion share repurchase authorization was a pivotal addition to the quarter.

With $2.5B in cash and marketable securities, Reddit now has:

-

Capital return optionality

-

Downside valuation support

-

A signal that management views the recent ~40% drawdown as overdone

This is a meaningful psychological shift for the stock and a key reason shares are up ~9%.

User Growth

User growth re-accelerated meaningfully:

-

Global DAUq reached 121.4M (+19% YoY)

-

International DAUq rose 28% YoY, far outpacing the U.S.

Machine translation and localization are clearly working, and international growth is becoming a structural contributor rather than a future promise. This matters because international users are now monetizing faster than prior cohorts.

Advertising Engine Still Firing

Advertising continues to be the clear growth driver:

-

Ad revenue grew 75% YoY to $690M

-

Advertising represented ~95% of total revenue

-

ARPU expanded 42% globally, with U.S. ARPU up 53%

This confirms Reddit’s ad stack is not only scaling with users but improving in efficiency — a critical validation after skepticism that growth would slow as comps got tougher.

Management Commentary

CEO Steve Huffman framed the quarter as a transition point for the platform:

“We’re entering the next era of Reddit—defined by sharper execution, global expansion, and product innovation that puts real people and conversations at the center.”

The tone was confident and forward-leaning, emphasizing execution, international scale, and turning Reddit’s authenticity into durable utility for users and advertisers.

Guidance Update

Q1 2026 Outlook

-

Revenue: $595M–$605M

-

Adjusted EBITDA: $210M–$220M

While Q1 guidance implies normal seasonal deceleration from Q4, margins remain robust, and management reiterated confidence in sustained growth through 2026. Importantly, nothing in the outlook suggests a slowdown in either demand or monetization efficiency.

Topline Results vs. Expectations

| Metric | Actual | Street Expectation | Result |

|---|---|---|---|

| Revenue | $726M | ~$660M | 🟢 Beat |

| EPS (GAAP, Diluted) | $1.24 | ~$0.93 | 🟢 Beat |

| Adj. EBITDA | $327M | ~$280M (guide midpoint) | 🟢 Beat |

Reddit delivered a decisive beat across revenue, earnings, and profitability, extending its streak of strong execution. Revenue accelerated to 70% year-over-year growth, while margins remained elite at scale, the combination the market has been demanding after the stock’s recent pullback.

Reddit Up Big After Earnings

Reddit’s shares are rallying ~9% after hours as investors digest a decisive beat-and-raise-style quarter, capped by a surprise $1B share repurchase authorization.

-

Revenue came in at $726M vs. ~$660M expected, a clear acceleration to 70% YoY growth.

-

GAAP EPS of $1.24 crushed the ~$0.93 consensus.

-

Adjusted EBITDA margin hit 45%, reinforcing that Reddit’s profitability is scaling, not peaking.

Key Takeaways From Last Quarter

- Achieved 640K Bitcoin holdings and strong profitability with $163M net income (28% margin), hitting 40% adjusted EBITDA margin—a goal set at IPO. Growing to 116M daily users with 20% YoY growth through machine translation in 30 languages and improved product features.

- Advertising revenue surged 74% YoY to $549M with 75%+ advertiser growth. Improving ad performance through AI-driven models showing 20%+ conversion improvements, while expanding into lower-funnel products like Dynamic Product Ads and automated bidding.

- Launched Reddit Answers integrated into search (75M weekly searchers) and Reddit Pro tools for publishers. Focusing on app growth and international expansion in France, Brazil, India, while maintaining strong product margins despite inventory management challenges.

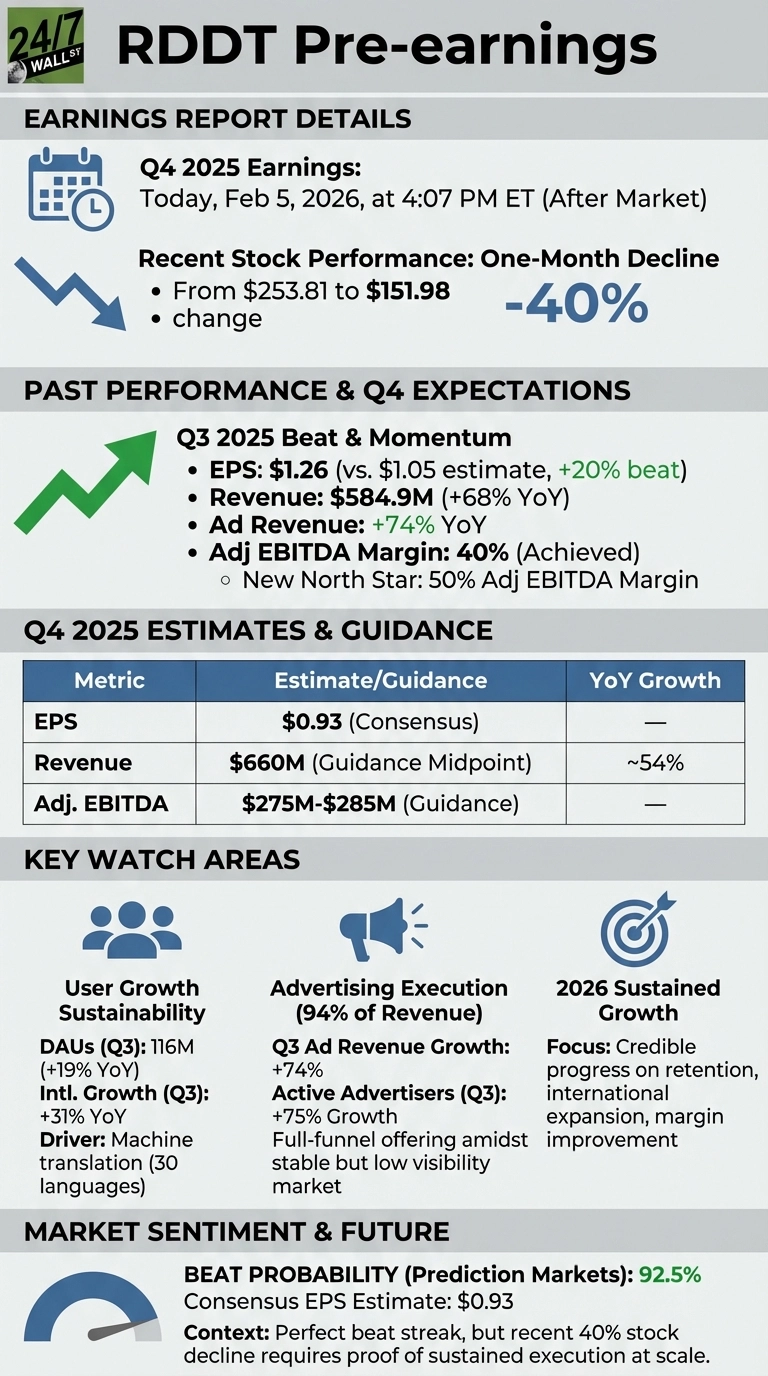

Reddit (NYSE: RDDT | RDDT Price Prediction) reports fourth-quarter 2025 earnings today after the bell at 4:07 PM ET. After a sharp decline from $253.81 one month ago to $151.98, investors are watching whether management can deliver another beat and sustain momentum that drove eight consecutive earnings surprises.

Proving the Growth Story Still Works

Reddit enters this quarter with credibility to protect. The company crushed Q3 expectations, posting $1.26 EPS against a $1.05 estimate, a 20% beat. Revenue hit $584.9 million, up 68% year-over-year, with advertising revenue climbing 74%. Reddit reached its pre-IPO profitability target of 40% adjusted EBITDA margin and immediately raised the bar, setting a new 50% margin North Star.

The question is whether Q4 can validate that trajectory. Management guided to $655 to $665 million in revenue and $275 to $285 million in adjusted EBITDA. Consensus expects $0.93 EPS, down from Q3’s $1.26 but still reflecting strong profitability. Management’s guidance implies roughly 54% year-over-year growth at the midpoint.

| Metric | Q4 2025 Estimate | YoY Growth |

|---|---|---|

| EPS | $0.93 | — |

| Revenue (Guidance Midpoint) | $660M | ~54% |

What I’m Watching

I’ll focus on three things: user growth sustainability, international momentum, and advertising execution. Daily active users hit 116 million in Q3, up 19% year-over-year, with international users growing 31%. CEO Steve Huffman emphasized that machine translation across 30 languages was the largest organic growth driver. Any deceleration would raise concerns.

Advertising remains the core business at 94% of revenue. Management noted “broadly stable” market conditions with “low visibility” heading into Q4, citing tariff concerns among some customers. Watch whether Reddit’s full-funnel ad offering held up and whether pricing power continued. Q3 saw 75% growth in active advertisers and strong performance across both brand and direct response ads.

Guidance will matter more than the print. With shares down 40% in one month despite the company’s track record, investors need reassurance that 2026 can sustain this growth rate as comps get harder.

A Reset Opportunity

Prediction markets are pricing in a 92.5% probability that Reddit beats the $0.93 consensus. That confidence reflects Reddit’s perfect beat streak, but the stock’s recent volatility suggests the market wants proof that execution can continue at scale. If management shows credible progress on retention, international expansion, and margin improvement, sentiment could shift quickly at this valuation.

Joel South covers large-cap stocks, dividend investing, and major market trends, with a focus on earnings analysis, valuation, and turning complex data into actionable insights for investors.

He brings more than 15 years of experience as an investor and financial journalist, including 12 years at The Motley Fool, where he served as an investment analyst, Bureau Chief, and later led the Fool.com investing news desk. He has also co-hosted an investing podcast and appeared across TV and radio discussing market trends.

© 24/7 Wall St.