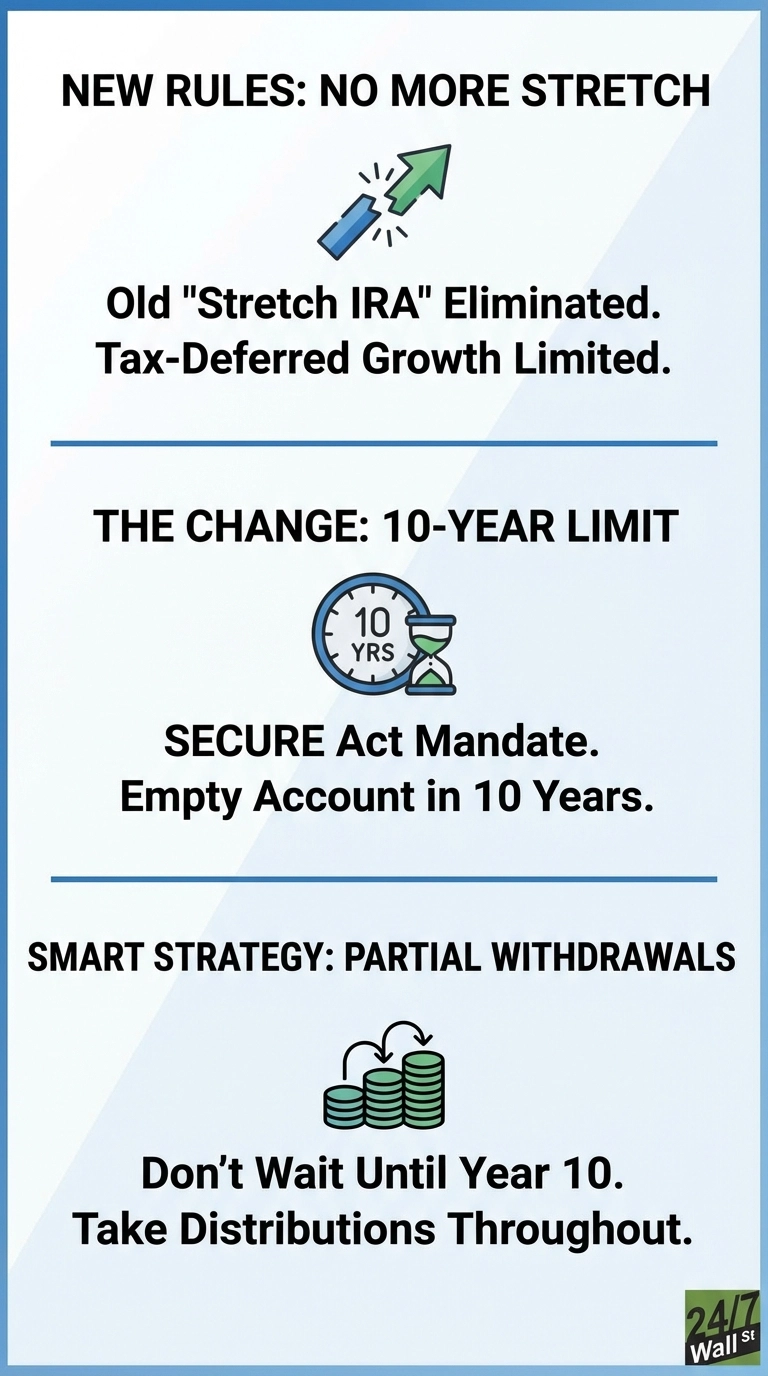

If you’re expecting to inherit an IRA from a parent or other relative, the distribution rules have fundamentally changed in ways that could significantly increase your tax burden. The SECURE Act of 2019 eliminated the “stretch IRA” for most non-spouse beneficiaries, replacing it with a 10-year distribution requirement that many heirs remain unaware of.

How the Old Stretch IRA Rules Worked

Before January 1, 2020, beneficiaries enjoyed remarkable flexibility with inherited IRAs. The stretch IRA strategy allowed heirs to take small annual distributions based on their life expectancy, keeping most funds growing tax-deferred for decades. This meant a middle-aged beneficiary could preserve the tax-advantaged status of an inheritance well into retirement.

The New 10-Year Distribution Requirement

The SECURE Act changed everything for most beneficiaries. Non-spouse heirs must now empty the entire inherited IRA within 10 years of the original owner’s death. There’s no requirement to take distributions annually during those 10 years, but the account must be depleted by December 31 of the tenth year following the owner’s death.

The compressed timeline creates a significant tax problem. Consider a 45-year-old beneficiary inheriting a $500,000 IRA during peak earning years. Under the old rules, they could have stretched distributions across three decades, taking smaller amounts in lower tax brackets. Now forced to withdraw everything within 10 years, those same dollars get stacked on top of their highest-earning years, potentially pushing substantial portions into the 32% or 35% federal brackets instead of the 22% or 24% brackets they might have used with a stretch strategy.

The tax impact varies dramatically based on distribution strategy. A beneficiary who spreads withdrawals evenly across 10 years typically faces a moderate tax increase compared to the old stretch approach. But those who wait until year 10 and take a lump sum face the steepest tax consequences, as the entire inheritance gets taxed at their highest marginal rate in a single year.

Who’s Exempt From the 10-Year Rule

Certain “eligible designated beneficiaries” can still use life expectancy distributions. These include surviving spouses, minor children of the account owner (until they reach age 21), disabled or chronically ill individuals, and beneficiaries not more than 10 years younger than the deceased owner. Once a minor child reaches age 21, they must empty the remaining balance within 10 years.

The Costly Mistake Many Beneficiaries Make

The most common error is assuming inherited IRAs work like they used to. Adult children in their peak earning years who inherit retirement accounts often wait until year 10 to take any distributions, then face a massive tax hit when forced to withdraw the entire balance at once.

A better strategy involves taking partial distributions throughout the 10-year period to manage tax brackets more effectively. Some beneficiaries may benefit from taking larger distributions in lower-income years or coordinating withdrawals with other tax planning strategies.

This content is for educational purposes and should not be considered personalized financial advice. Consult with a tax professional regarding your specific situation.