Regional banks continued their steady dividend payouts this week, with Dime Community Bancshares (NASDAQ: DCOM) paying 25 cents per share on Jan. 23, maintaining the quarterly rate it’s held since early 2023. The payment reflects a 2.79% dividend yield based on the current stock price of $36.23, but the real story lies in whether these regional institutions can sustain their shareholder distributions amid a challenging interest rate environment.

Dividend Aristocrats and Steady Payers

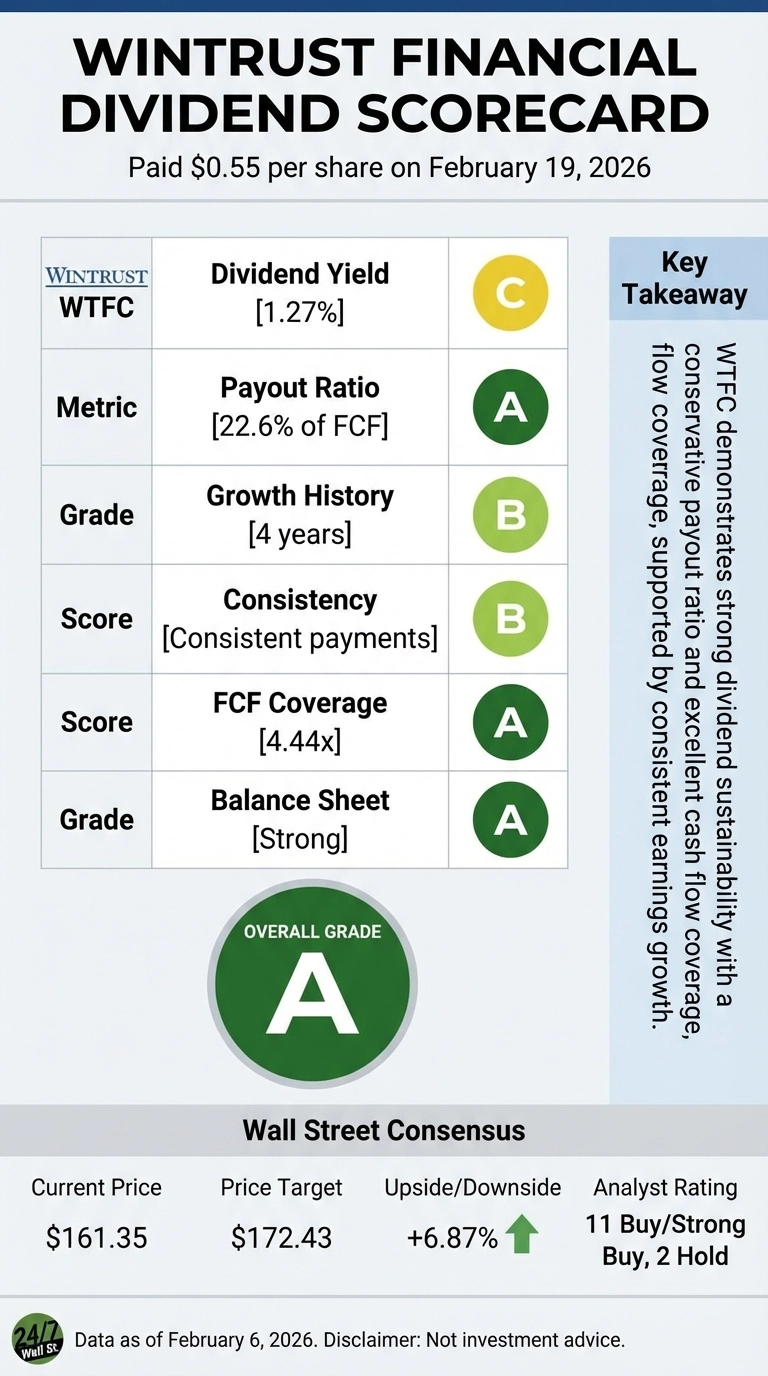

Among the regional banks that just paid investors, Wintrust Financial (WTFC) delivered 55 cents per share on Feb. 19, 2026, representing a 10% increase from the previous quarter’s $0.50. This marks the company’s fourth consecutive year of dividend growth, with the annualized payout climbing from $1.60 in 2023 to a projected $2.20 in 2026. At the current price of $161.35, the yield sits at 1.27%, modest but backed by strong fundamentals.

WTFC’s dividend sustainability looks solid. The company generated $721.6 million in operating cash flow during 2024, comfortably covering the $143.3 million in dividend payments by a factor of 4.4 times. With a return on equity of 12.1% and net income of $823.8 million in 2025, up 18.5% year-over-year, management has demonstrated both the capacity and willingness to reward shareholders.

UMB Financial (NASDAQ: UMBF) | UMBF Price Prediction will pay 43 cents per share on April 1, up from 40 cents in the prior two quarters. The Kansas City-based bank has increased its dividend for five consecutive years, with the 2025 annual total reaching $1.63 compared to $1.58 in 2024. At $134.32 per share, the stock yields 1.24%, with a remarkably conservative payout ratio of just 17.5% based on trailing earnings of $9.30 per share.

Growth Streaks Under Pressure

Bank OZK (NASDAQ: OZK) paid 46 cents per share in mid-January 2026, extending a pattern of quarterly increases that has delivered approximately 2.3% growth each quarter throughout 2025. The annual dividend reached $1.74 in 2025, up from $1.58 in 2024. At $51.40, the stock offers a 3.48% yield, the highest among the regional banks examined here.

However, this bank’s dividend faces headwinds. The bank’s interest expense surged from $688.7 million in 2023 to $1.08 billion in 2025, a 56% increase that has compressed margins. The interest coverage ratio—operating income divided by interest expense — deteriorated from 1.26 times in 2023 to just 0.87 times in 2025. This means operating income no longer fully covers interest costs, a concerning signal for dividend sustainability. While operating cash flow of $834.5 million still covers the $195.6 million dividend by 4.3 times, the underlying profitability trend warrants scrutiny.

United Community Banks (NYSE: UCB) paid 25 cents per share on Jan. 5, representing a 4% increase from the prior year’s quarterly rate of 24 cents. The Georgia-based bank has grown its dividend for more than a decade, with the annual payout climbing from $0.22 in 2015 to $0.98 in 2025. At $36.52, this regional yields 2.73%, backed by a 9.28% return on equity and 14.8% year-over-year earnings growth.

The Sustainability Question

For regional banks, dividend sustainability hinges on managing the dual pressures of elevated interest expenses and maintaining loan quality. DCOM’s operating cash flow of $99.1 million in 2024 covered its $45.3 million dividend by 2.05 times, providing adequate cushion. The company rebounded strongly from a $20.4 million loss in Q4 2024 to generate $110.7 million in net income for full-year 2025, suggesting operational improvement.

UMBF stands out with its conservative 17.5% payout ratio, leaving substantial room for dividend growth or economic downturns. The bank’s net income surged 59.2% to $702.4 million in 2025, driven by strong revenue growth and improving margins. This provides a comfortable buffer for the $1.63 annual dividend.

The regional bank dividend landscape reveals a sector managing through interest rate normalization with varying degrees of success. While established players like WTFC and UMBF demonstrate robust coverage ratios and growing earnings, others face margin compression that could constrain future increases. For income investors, the 2.5% to 3.5% yields offered by these regionals provide meaningful cash flow, but selectivity matters—especially as interest coverage ratios signal which banks have the financial flexibility to maintain distributions through the next credit cycle.