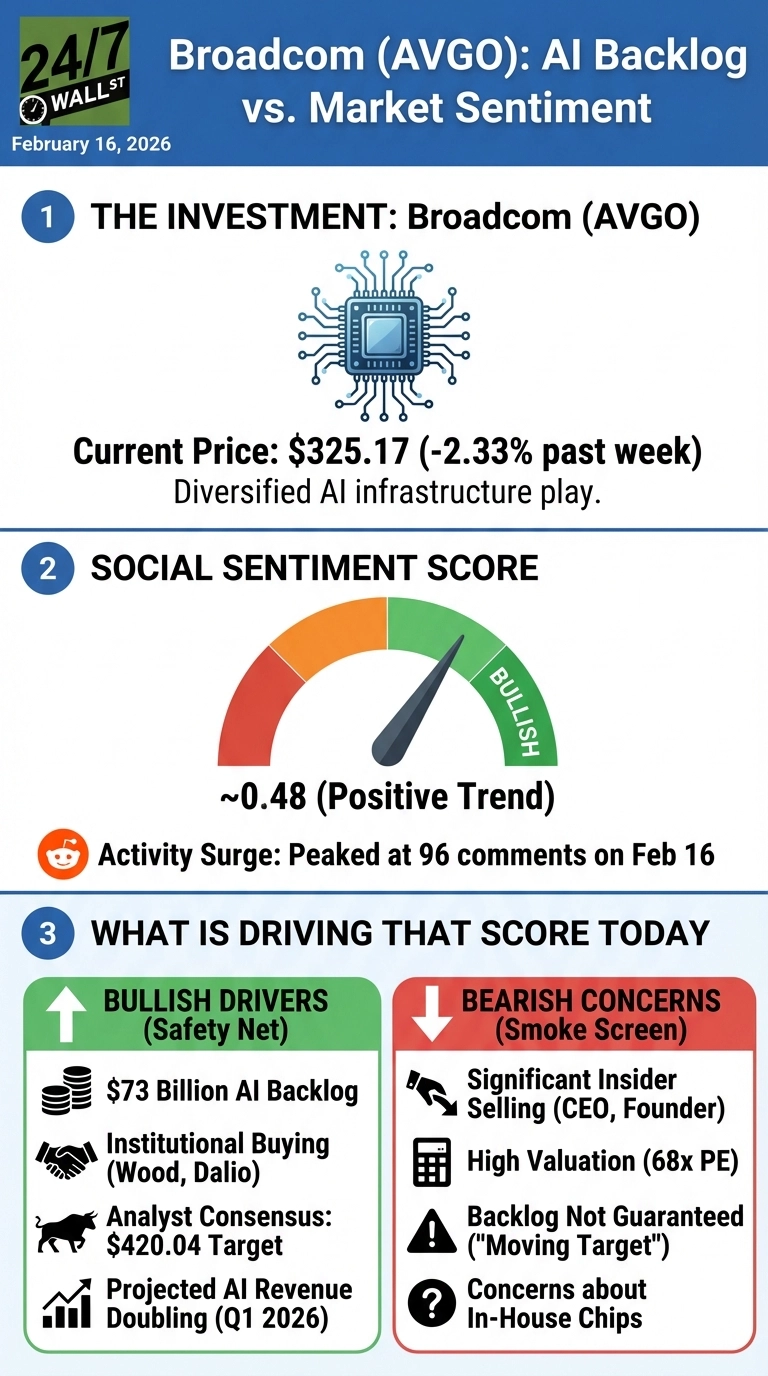

If you’re closely watching shares of Broadcom (NASDAQ:AVGO | AVGO Price Prediction) it was hard to escape watching as the stock fell over 2% over the past week, trading at $325.17, down 6.05% year-to-date. On the other hand, Reddit activity surged mid-February, with mentions peaking at 96 comments on February 16.

AVGO’s Massive Decline…a buying opportunity?

by InvestorDiscussions in wallstreetbets

Broadcom tumbles 11% despite blockbuster earnings

by MarketWatcher in stocks

This r/wallstreetbets post discussed whether the selloff represented a potential entry point given the AI backlog and guidance. Meanwhile, another r/stocks discussion noted: “Despite beating on revenue and earnings, the stock dropped 11% on concerns about valuation and guidance interpretation.” Retail investors are focused on Broadcom’s $73 billion AI backlog and projected 54.5% EPS growth for fiscal 2026.

The AI Backlog: Wall Street’s Safety Net

In a boost to the stock, Cathie Wood’s ARK Invest purchased $10.7 million worth of AVGO shares following the decline, while Ray Dalio’s Bridgewater Associates added 320,349 shares. This suggests Wall Street analysts remain bullish, with 38 of 43 top analysts rating the stock “Strong Buy” or “Buy,” and a consensus 12-month price target of $420.04, representing a 29% upside.

CEO Hock Tan disclosed $73 billion in AI-related backlog, including custom XPU accelerators, switches, and optical components. “We have never seen bookings of the nature that what we have seen over the past three months,” Tan said on the Q4 2025 earnings call. The backlog includes orders from five hyperscale customers building custom AI chips, plus demand for Broadcom’s 102 terabit per second Tomahawk 6 switch.

Three factors support the bullish case:

- Revenue visibility: Broadcom expects AI revenue of $8.2 billion in Q1 2026, representing a year-over-year doubling

- Customer diversification: Five hyperscale customers are building custom XPUs with Broadcom, including Google and Anthropic

- Margin resilience: Operating margin dollars expected to grow through scale leverage

Concerns Linger Despite Analyst Enthusiasm

Of course, insider selling raises questions: CEO Hock Tan sold 130,000 shares on December 18, while Director Henry Samueli sold 391,339 shares on December 8. Tan warned investors not to treat the $73 billion as guaranteed revenue. “Do not take that $73 billion as that’s the revenue we ship over the next eighteen months,” he cautioned, noting the backlog is “a moving target”. DA Davidson issued a “Neutral” rating, citing valuation concerns and risks if hyperscalers build more chips in-house.

NVIDIA Comparison and Next Steps

Broadcom trades at 68x trailing earnings, while NVIDIA (NASDAQ:NVDA) commands 45x with higher profit margins of 53% versus Broadcom’s 36%. Yet Broadcom’s $1.54 trillion market cap positions it as a diversified AI infrastructure play beyond GPUs.

Analysts project free cash flow growing from $26.9 billion in 2025 to $107 billion by 2029. Investors should monitor Q1 2026 earnings for confirmation that AI revenue doubles as guided and watch for changes in hyperscaler CapEx plans.