DigitalOcean (NYSE:DOCN | DOCN Price Prediction) reported Q4 2025 earnings before the open on Feb. 24, beating EPS estimates and raising its multi-year growth outlook. The stock was trading around $59 in premarket, off roughly 5% from its prior close, as investors digested the guidance details even as headline numbers impressed.

AI Traction Drives a Clean Beat

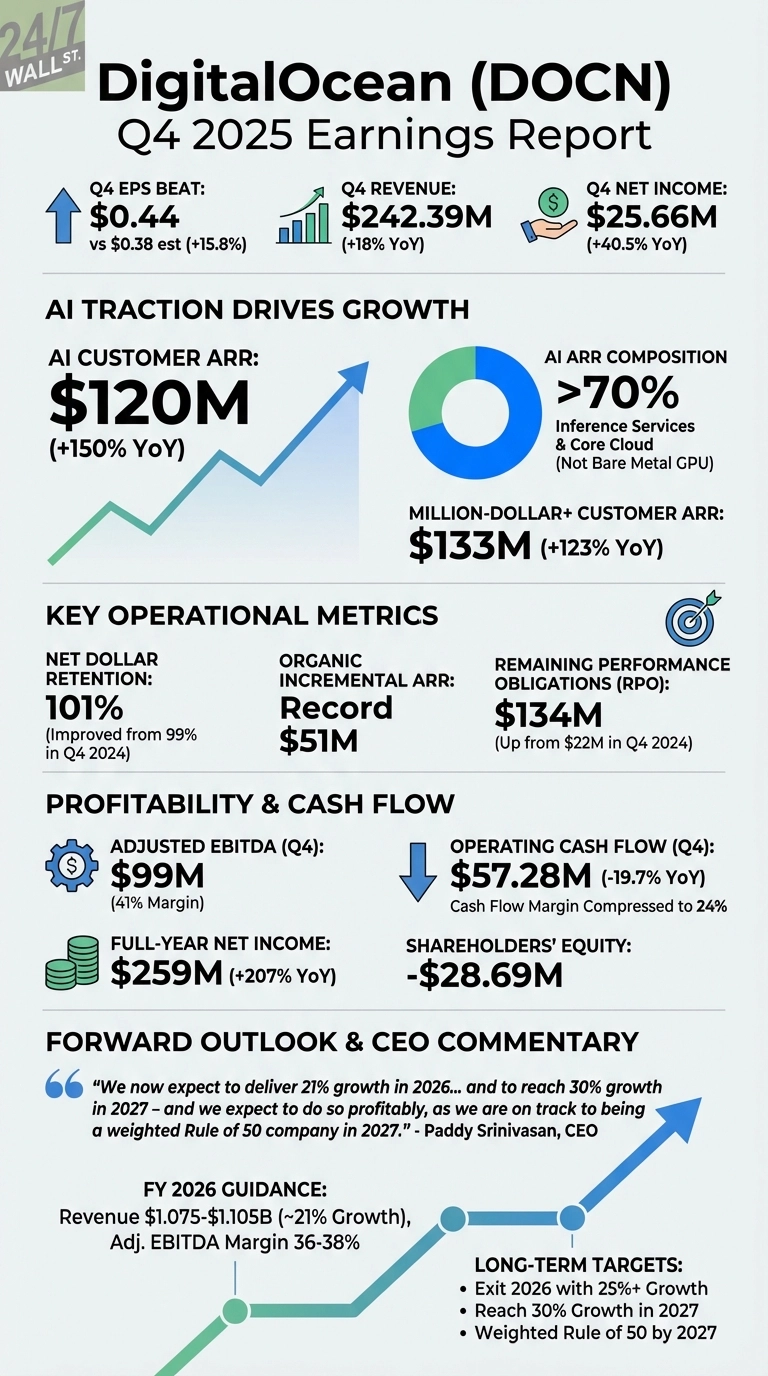

The quarter showed real momentum. Revenue grew 18% year over year to $242.39 million, and non-GAAP EPS came in at 44 cents against a 38 cents consensus estimate, a 15.8% beat. The key driver is AI. AI customer ARR hit $120 million, up 150% year over year, and more than 70% of that AI ARR came from inference services and core cloud products rather than bare metal GPU. That distinction positions DigitalOcean closer to a platform play than a commodity GPU rental business, a more defensible revenue mix.

Million-dollar-plus customer ARR reached $133 million, up 123% year-over-year (YOY), and net dollar retention improved to 101% from 99% in Q4 2024. The company added a record $51 million in organic incremental ARR and reached $1 billion in annualized monthly run-rate revenue in December 2025.

Cash Flow Compression Deserves a Look

Q4 operating cash flow fell 19.7% YOY to $57.28 million, with cash flow margin compressing from 35% to 24%. That’s a meaningful step down even as revenue grew. The company also carries negative shareholders’ equity of -$28.69 million, largely a function of its aggressive share buyback program. Capital efficiency is the number to watch heading into 2026.

EPS Beat Headlines a Strong Year

- Non-GAAP EPS: 44 cents (vs. 38 cents expected); up from prior year

- Revenue: $242.39M; +18% YOY

- Adjusted EBITDA: $99M; 41% margin

- Net Income (Q4): $25.66M; +40.5% YOY

- Full-Year Net Income: $259M; +207% YOY

- RPO: $134M, up from $22M in Q4 2024

The RPO jump is the quiet standout. Growing from $22M to $134M in a year signals customers are committing to longer-term contracts, giving the revenue trajectory more visibility.

CEO Strikes a Confident Tone on Growth Path

CEO Paddy Srinivasan was direct about the company’s direction. “We now expect to deliver 21% growth in 2026, to exit 2026 at 25%+ growth and to reach 30% growth in 2027 – and we expect to do so profitably, as we are on track to being a weighted Rule of 50 company in 2027,” he said. That’s an accelerating growth curve with a profitability commitment attached.

Can the Growth Acceleration Hold?

Full-year 2026 guidance calls for revenue of $1.075 to $1.105 billion, roughly 21% growth, with adjusted EBITDA margins of 36% to 38%. Watch whether AI customer ARR continues compounding at this pace and whether cash flow margin recovers, the real test of whether the growth story is as clean as the headline numbers suggest.