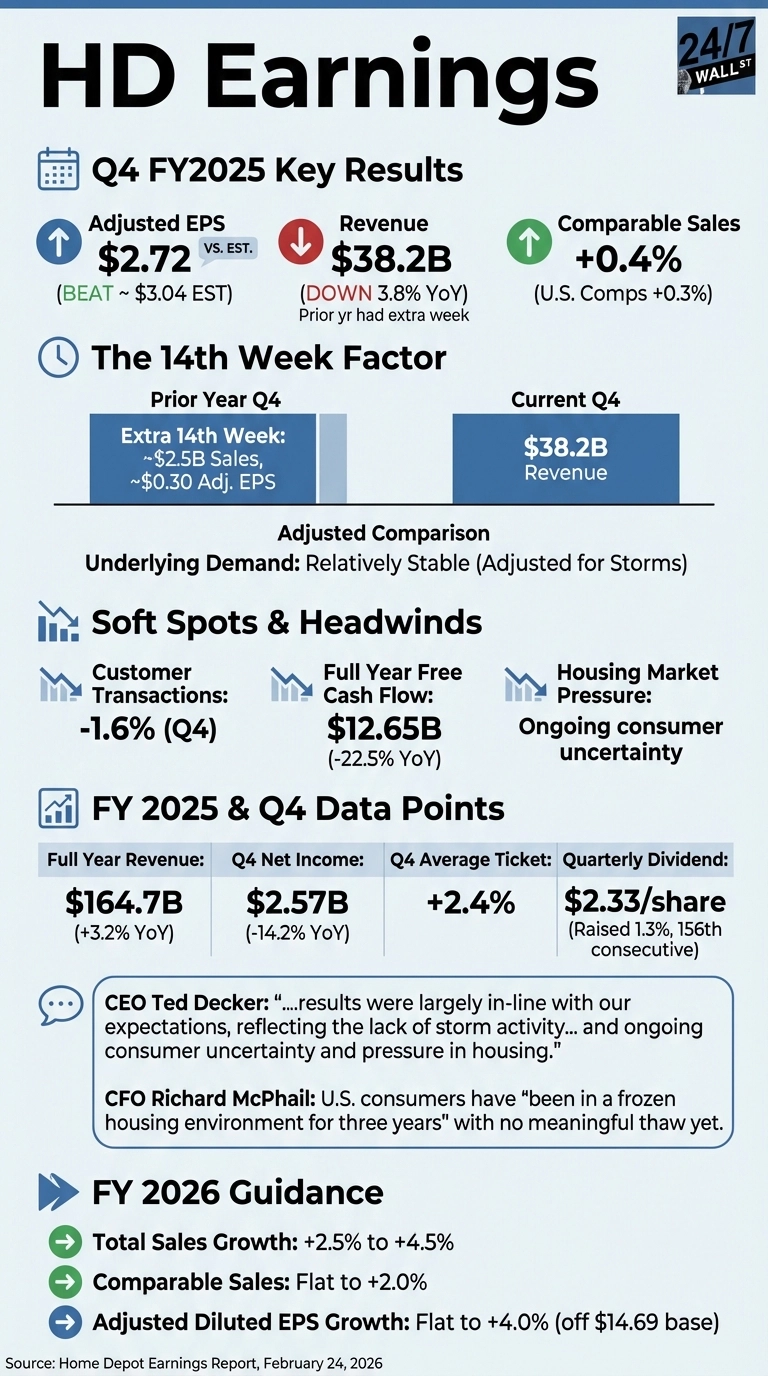

Home Depot (NYSE: HD | HD Price Prediction) reported Q4 fiscal 2025 results before the open on Feb. 24, topping Wall Street’s earnings and revenue expectations for the first time in a year. Adjusted EPS came in at $2.72, ahead of the $2.54 LSEG consensus estimate, and revenue of $38.2 billion edged past the street forecast. Shares climbed roughly 3.5% in premarket trading on the news.

The 14th Week Explains Most of the Decline

The headline revenue drop looks worse than it is. Sales fell 3.8% year over year to $38.2 billion, but the prior-year quarter included an extra 14th week that added approximately $2.5 billion in sales and 30 cents in adjusted EPS. Strip that out and the comparison is far more flattering. Comparable sales grew 0.4%, with U.S. comps up 0.3%. Average ticket rose 2.4%, meaning the customers who did come in spent more. That detail suggests the core customer relationship is holding even as foot traffic remains soft.

For the full fiscal year, revenue grew 3.2% to $164.7 billion, driven in part by the SRS Distribution acquisition, which now has over 1,250 locations operational. Full-year adjusted EPS landed at $14.69.

Traffic and Free Cash Flow Are the Soft Spots

Customer transactions fell 1.6% in Q4 and 1.0% for the full year, a persistent signal that housing market pressure is keeping shoppers away from bigger project spending. Free cash flow for the year dropped 22.5% to $12.65 billion, partly reflecting the capital demands of integrating SRS. The company also completed fiscal 2025 without any share repurchases, prioritizing debt management after the acquisition. Transaction volume remains a key metric for assessing whether a broader recovery is underway.

EPS Beat Anchors the Quarter

Key Figures

- Adjusted EPS: $2.72 vs. ~$2.54 expected

- Revenue: $38.2B vs. ~$38.12B expected; down 3.8% YoY (extra week in prior year)

- Comparable Sales: +0.4% (U.S. comps +0.3%)

- Average Ticket: +2.4%

- Customer Transactions: -1.6%

- Net Income: $2.57B; down 14.2% YoY

- Full-Year Free Cash Flow: $12.65B

- Quarterly Dividend: $2.33/share (raised 1.3%; 156th consecutive quarterly payment)

The EPS beat was the headline, but average ticket growth is the quiet driver worth watching. It points to a customer base that is still spending on projects, just doing so selectively.

CFO Flags a Frozen Housing Market

CEO Ted Decker said “our results were largely in-line with our expectations, reflecting the lack of storm activity in the third quarter and ongoing consumer uncertainty and pressure in housing” and added that “adjusting for storms, underlying demand was relatively stable throughout the year.” CFO Richard McPhail was more direct, telling CNBC that U.S. consumers have “been in a frozen housing environment for three years” with no meaningful thaw yet. He acknowledged rising consumer uncertainty and declining confidence as signals the company is watching closely. Management sounded steady, not bullish, reflecting the cautious macro backdrop.

Guidance Points to a Modest Recovery

Home Depot guided fiscal 2026 for total sales growth of 2.5% to 4.5%, comparable sales growth of flat to 2.0%, and adjusted EPS growth of flat to 4.0% off the $14.69 base. With spring selling season approaching, whether housing turnover shows signs of life in the coming quarters will be a key indicator for the home improvement sector.