Micron (NASDAQ:MU | MU Price Prediction) was once seen as a volatile tech stock that made memory chips, a mundane piece of hardware required by computers that was sometimes in demand, sometimes not. The infamous memory cycle made this stock trade cheaply, since investors were always debating whether or not memory chips were in demand enough to push up prices. Then, you need to take into account the foreign competition. South Korean companies like SK Hynix and Samsung make great chips too. The argument was, why would anyone buy from an expensive American company? Surely Micron was on its way out, right?

Very few actually saw what was coming, and those who did are laughing their way to the bank. MU stock is up 330% over the past year. The AI rally came out of nowhere, and the memory shortage came even faster. It took only two or so weeks for the RAM shortage to become the talk of the town in tech circles.

What happened in the past year

Before we look into the valuation, it’s a good idea to brush up on what caused MU stock to surge so much so fast.

Micron sells both DRAM (which is system memory) and NAND flash (storage, like SSDs). It also sells the premium AI flavor of DRAM, which is HBM, or high bandwidth memory.

TrendForce’s recent report is explicit that both DRAM and NAND are being pulled by AI and data center demand, and that this pull is strong enough to tilt the whole market into a seller’s market.

HBM is the star. Micron markets its HBM3E as delivering more than 1.2 TB per second of bandwidth per placement, with very high pin speeds, specifically aimed at AI accelerators and data centers.

Why I believe this rally will last a little longer

AI memory is not optional once you are building modern training and inference boxes. HBM exists because GPUs are compute-rich and memory-starved, so when AI deployments accelerate, HBM demand can lurch upward faster than the rest of the memory complex. Thus, we may be looking at demand that is stickier than what the market expects today.

A year ago, the key question for Micron’s valuation was basically, can it even get into the HBM club at scale, or will Hynix and Samsung soak up the profits and leave Micron with the leftovers? Now is “how much will Micron take?” And the fact that this is an American company has turned into an advantage, as most of the AI buildout is still U.S.-centric.

I believe MU stock could rally more, especially as market experts still think demand is red hot. Orders are still surpassing suppliers’ capacity, and memory makers are reallocating production lines to DRAM, which is tightening NAND even more.

When a researcher is projecting 90 to 95 percent QoQ DRAM contract price jumps and still warning the forecast could move higher, the burden of proof shifts to the bears.

I will admit… There’s more risk than reward

No one genuinely expects MU stock to rally forever, and as with every memory demand spike, there will be a drawdown, and it could get ugly. Everyone hopes to sell ahead of the fall, and after a 330% gain, you’re no longer in pump territory and closer to the dump.

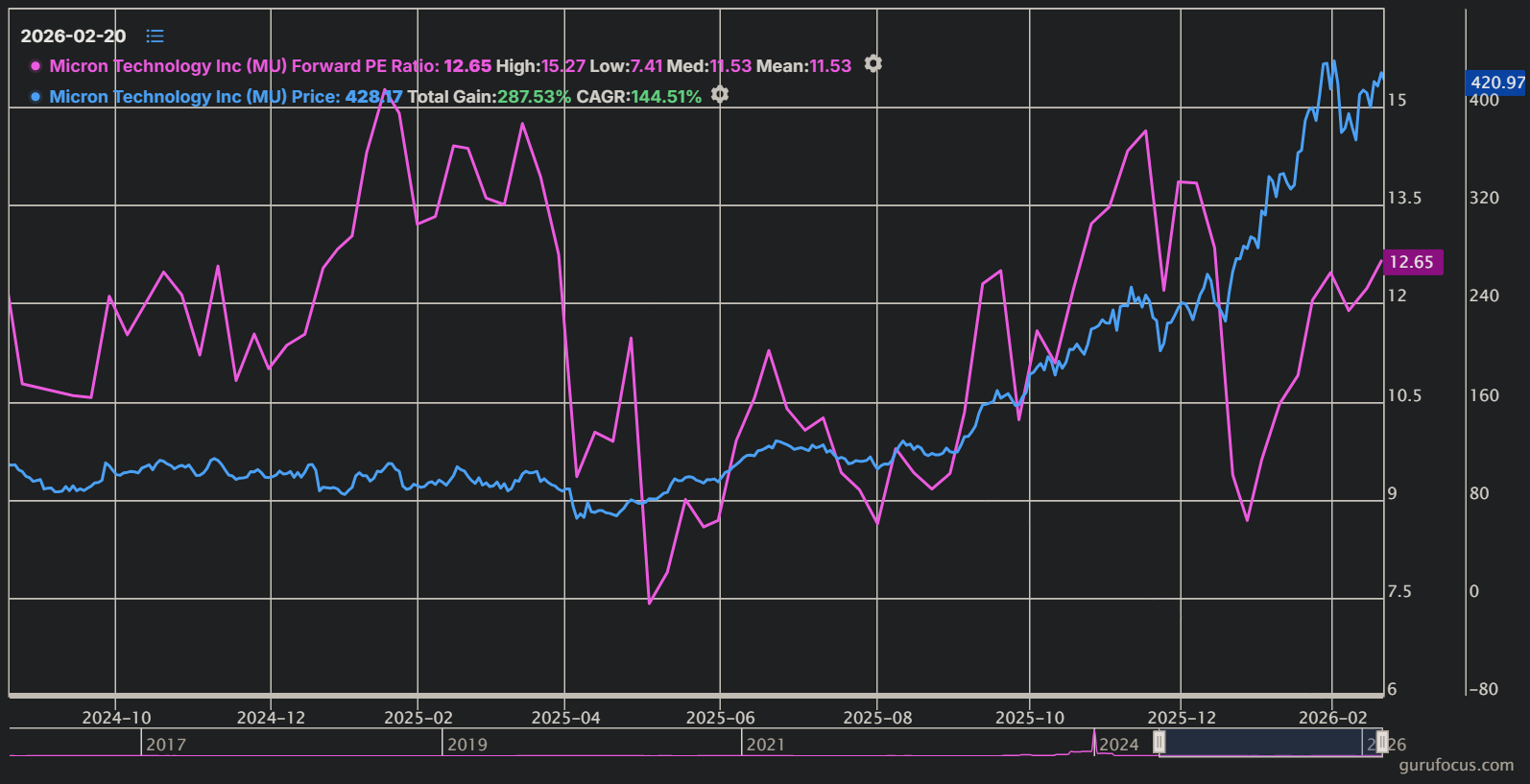

But before you run away in fear, here’s the silver lining. MU stock trades at just 12 times forward earnings. Yes, you heard that right.

This is the estimated price in the coming months if the market holds the historical earnings premium (minus non-recurring items).

That’s just 15 times earnings, and MU stock is trading at over 37 times that today. But even if you extrapolate the stock with the lower historical median number and take the earnings estimates at fair value, you get the scenario above.

It’s certainly possible if hyperscalers keep pouring money into the AI buildout. The market has been expecting a slowdown for the past three years, so a fourth year won’t be a surprise.

Where I see MU stock going

This is a stock that is extremely cheap for the growth you are getting. 12 times forward earnings for this fiscal year and just 9 times forward earnings for next fiscal year’s earnings. Don’t take those estimates as gospel, but even the lowest estimate suggests a quadrupling of earnings.

Where it does get interesting is that the market is digesting that growth in real time. The forward PE has hovered sideways as the price increased increasingly, so that quadrupling of earnings is already baked in.

Thus, I believe a more realistic target is a 60% upside from here. In past cycles, MU stock topped out at 20 times forward earnings before the pendulum swung the other way. What we’re dealing with now is an unpredictable cycle driven by AI, so deciding whether or not the stock will reach that mark this time or turn back before it even hits 13 times forward earnings is up to you.