Americans often come across advice regarding Social Security, but many ignore the critical advice that puts them at a disadvantage during retirement. While many Americans look forward to turning 62 so they can sign up for Social Security, there are other factors one mustn’t ignore.

The decision to claim Social Security isn’t an easy one, and a lot of seniors are tempted to file for the benefits at the earliest. You’ve paid into the system, and now you’re more than ready to start receiving the money. However, your filing age can play a huge role in the amount of money you receive each month.

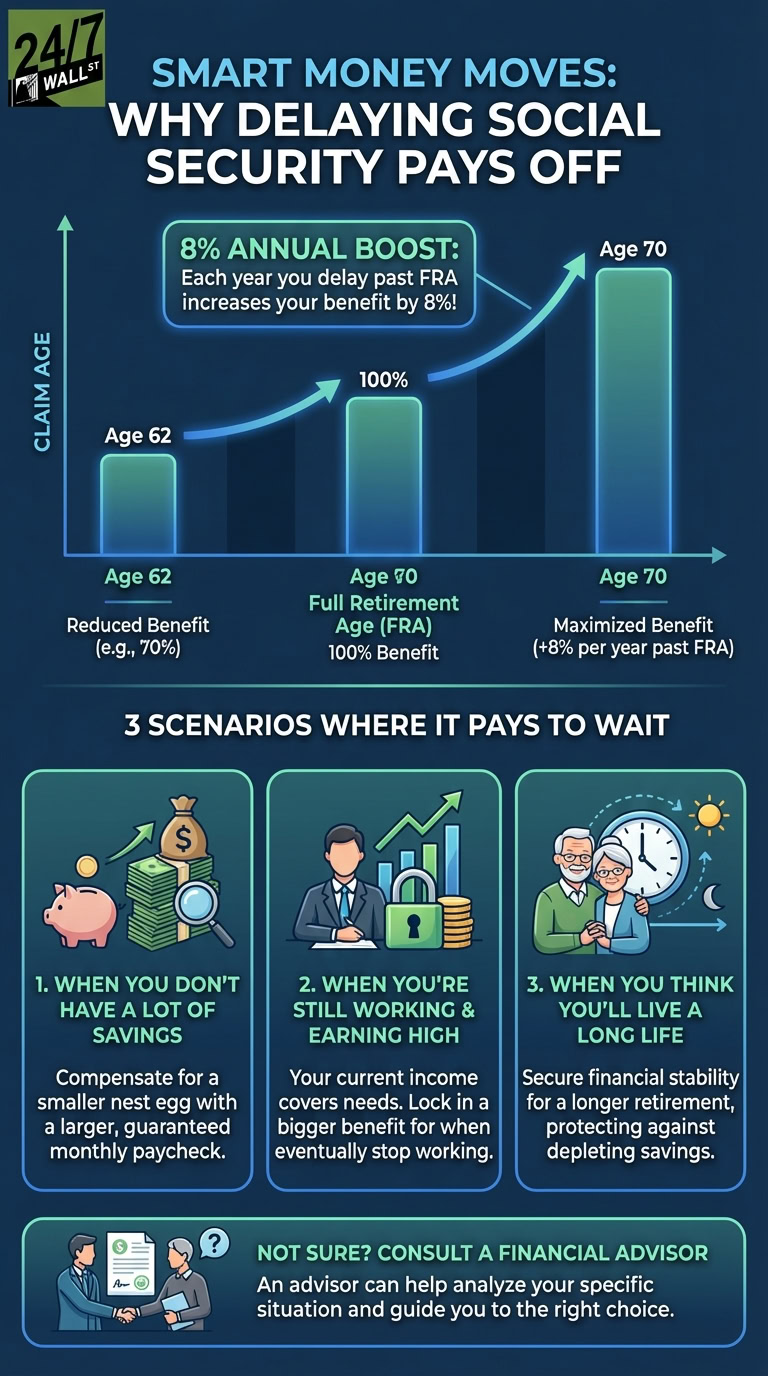

The recommended strategy of delaying Social Security benefits until the age of 70 to maximize payouts is worth considering. Although the monthly benefits are calculated based on the personal earnings history, the filing age will make a difference to the amount of money you receive monthly. If you rush through this decision, it could end up costing you $100,000 over a lifetime.

Delaying Social Security benefits can be a win-win

In a period of rising inflation, growing healthcare costs, and increasing cost of living, making the most of your Social Security income has become crucial. A single decision could cost you tens of thousands of dollars in your lifetime.

Some Americans claim early due to income needs and uncertainty over the future of Social Security funding. There are also worries around the stability of the benefits if they delay claiming. Many are even unaware of the long-term benefits. While the math is simple, it is worth understanding thoroughly.

Reducing a guaranteed source of income is a move you shouldn’t take lightly. If you do not have enough retirement savings or expect your spouse to outlive you, filing for Social Security early will mean taking a huge risk. It could leave your spouse with a smaller benefit. If your savings are modest and you’re counting on Social Security for the retirement years, you need to be careful when making this decision.

When you claim early, you reduce the benefits by about 30%, and the lower amount will remain locked in for your lifetime. If your full retirement benefit is $2,000 monthly and if you claim it at 62, it’ll drop to $1,400. This means you’re settling for $600 less every month, which amounts to $7,200 a year, and in a 20-year period, that could add up to more than $144,000 lost in benefits.

It is not a small amount, and the gap can make a big difference if you live longer or have a higher cost of living. When you claim at 62, your benefit could be about 30% lower than if you claim at the full retirement age. But if you claim benefits at 70, the benefits will be about 30% higher than the full retirement age.

Making the right call at the right age

Making this one social security filing mistake can be a huge financial setback. Properly timing the claims can make a huge difference to your retirement income, and if you can delay until the age of 70, it can end up being a sound financial decision. Claiming early might feel convenient, but it will reduce the retirement funds.

However, for some people, claiming Social Security early could be the only option. It makes sense if there’s no other choice and no other source of income. If you’ve lost a job or are unable to work due to health reasons, it makes sense to start the smaller monthly payments at 62. Getting more of these payments means you’re receiving a larger lifetime payday.

That said, if you have a significant amount of savings, you can consider filing for Social Security early. A large investment that generates $100,000 in retirement income could give you financial security, and you may be willing to take less money from Social Security each month.

While claiming early can provide immediate income, the monthly reduction will be permanent. If you claim at 62, you could receive $1,400 each month as compared to $2,480 each month at 70. Ultimately, consider your personal circumstances and decide if you really need to file early. If you can wait until 70, your reward will be larger checks.